More on Mortgage Affordability

In a recent post, I reviewed mortgage affordability. I argued that the front-loaded cash outlays of conventional mortgages are a relatively arbitrary choice. The reason mortgages are especially unaffordable now, given the amortization products that are common, is because of high rents and the supply shortage.

The Traditional Home Buyer Deal

Figure 1 here is my simple model of the 20th century “American Dream” deal. The 30 year mortgage has front-loaded cash outflows, in real terms, but in a market with stable rents and functional supply, home prices are low enough to make it manageable. With 4% income growth, 2% rent growth, and 7% mortgage rates, the initial mortgage payment would be similar to the rent payment on our hypothetical home, but since the mortgage payment is fixed, it becomes more affordable over time. Homeowners also have additional maintenance expenses. But, it ends up being a good deal over time, with personal control as a bonus, for the typical homeowner.

In all of these figures, the y-axis is the percentage of the resident’s income, and they are based on a home whose rent at move-in takes 30% of the tenant’s income.

Figure 2 is basically how the deal has evolved. Our broken housing supply means that while incomes still can grow at 4%, and general inflation might still be 2%, rents are typically growing at more like 3%. Since the future rental value on the house will be higher, the home’s price is higher. And, the front-loaded cash outflows of conventional mortgages now are even more front-loaded. (Now the mortgage payment is fixed while rent would increase by 3% annually. Rents used to increase by 2% annually. Now the fixed mortgage payment has to be higher to reflect the higher value of those future rents.)

Expected rent inflation increases the market value of homes and creates more front-loaded cash outflows for new home buyers.

The Financial Basics of Owning vs. Renting

Just to break this down conceptually a little more, Figure 3 is similar to Figure 1, but in a hypothetical market with no inflation instead of 2% inflation. So, everything is similar to Figure 1, but the topline numbers are all 2% lower (2% income growth, 0% rent growth, and 5% mortgage rates). You can see that inflation is part of the reason fixed rate mortgages are front-loaded. Again, this simply goes back to the fact that the mortgage payment is fixed while rents increase when there is inflation. In Figure 3, where there is no inflation, the trends in mortgage payments and rent payments are parallel.

The total cost (mortgage payment plus maintenance) is higher than the rent, until the mortgage is paid off, and then it is much lower. There are no capital gains in this hypothetical. Some of the difference between owner and renter cost is just the owner paying for accumulated equity in the property until they own it free and clear, after which the costs above maintenance costs are entirely the opportunity cost of invested capital rather than cash outlays.

To belabor the point, I have added a mortgage payment line for a mortgage that is interest only. In that hypothetical case, someone else’s capital is funding the home indefinitely in either case (rented or owned), and the owner’s total cost (maintenance plus mortgage payment) is similar to the renter’s cost in perpetuity.

In the real world, things change. Rents change. Valuations change. So the renter and the owner have different risks. But, at any given point in time, this is a reasonable estimation of the expected costs over time. Really, neither necessarily has systematically more or less risk. The risks are different. The renter’s rent could go up unexpectedly. The owner’s value could decline unexpectedly. That’s in the no-inflation, no amortization, no capital gains world.

“Higher mortgage rates hurt housing affordability.”

“Mortgage affordability” of the typical home can be thought of as a product of two certainties - (1) the amortization schedule and (2) current rental value - and several unknowns - (3) future inflation, (4) future real income trends, and (5) future housing supply. Keeping this in mind, I want to review what it means for “higher mortgage rates to hurt housing affordability”.

I think the thinking on this is universally misguided. Fundamentally that’s because Fed policy seems to get filtered down to “The Fed manages money supply by controlling interest rates.” which, in any meaningful sense just isn’t true. It certainly isn’t true of mortgage rates. And, as I frequently discuss here, there is little evidence that mortgage rates have much effect on home prices, anyway. In a market with perfectly elastic supply, home prices should simply reflect the cost of materials.

Let’s start with the baseline 20th century “American Dream” scenario in Figure 1 (4% income growth, 2% inflation and rent growth, 7% mortgage rates, Price/Income 4x). The things we know, stipulated in these hypotheticals, are that rent starts at 30% of income and it’s a fixed 30 year mortgage loan.

In the baseline scenario, mortgage payments start at 32% of income and end up at 10%.

The way interest rates are routinely characterized in housing discourse is that mortgage rates just move up or down in a way that is unrelated to other factors that determine housing supply and demand, or they are controlled by the Fed, and so, higher rates make homes less affordable and lower rates make them more affordable. In spite of the clear historical record that mortgage payments do not revert to some stable mean, they are routinely treated as if they do. When rates rise, many observers express expectations that prices must fall.

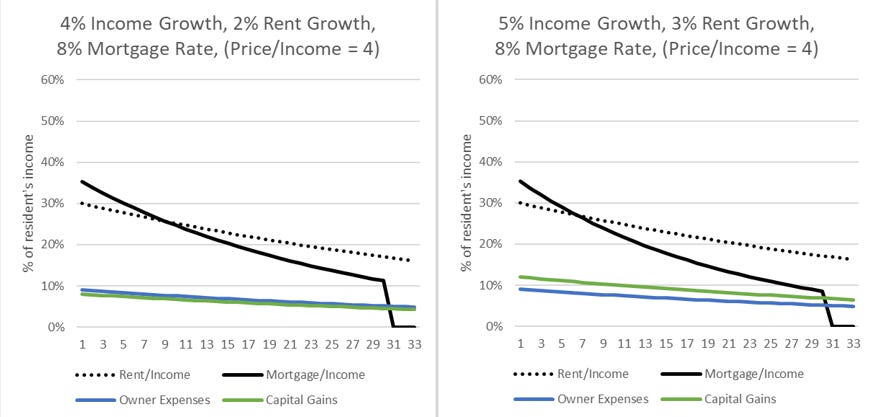

The left panel of Figure 4 characterizes this way of looking at it. An increase to an 8% mortgage rate raises the initial mortgage payment to 35%. Higher rates made homes 10% less affordable, implying that we should expect a 10% price decline.

What I will walk through here is that interest rates are related to the 3 uncertainties that determine mortgage affordability. They don’t change in a vacuum.

First, long-term rates generally coincide with long-term growth expectations. In long-term charts, the relationship is visually clear (and suggests how weird it is that so many associate low rates with nominal economic stimulus. Of course, Scott Sumner is a key resource on this.)

Growth can be real or inflationary. The right panel of Figure 4 assumes that a 1% rise in mortgage rates is related to a 1% rise in expected future inflation. In this case, everything scales up. Incomes will rise 5% annually and rents will rise 3% annually. In real terms, everything is the same as in the baseline, so the only difference in mortgage affordability is that higher inflation makes the 30 year amortization schedule more front-loaded.

Inflationary interest rate increases do make “mortgage affordability” worse. The initial payment increases to 35% of income. But, the financial proposition between owning versus renting isn’t any worse. The payment will decline as incomes inflate, so that by the end of the mortgage, the payment will take less than 9% of the owner’s income. And, each year, inflation creates capital gains amounting to a few additional percentage points of the owner’s income. So, the higher initial payment is a counterweight to future gains.

It is certainly true that inflation makes it harder for buyers to take on affordable mortgages. And, anecdotally, the strains of that are obvious. But, since the 1970s were an extreme example of this problem, there is no need to guess at what happens to home prices as a result. Home prices in the 1970s were not depressed. Interest rates much higher than 8% didn’t cause home prices to decline in order to make mortgage payments affordable.

Financial fundamentals are more dominant, in the aggregate, than the frictions created by mortgage amortization constraints. Home prices don’t decline in order to make mortgages affordable, to any degree that would dominate market trends.

But, in any case, the rise in long-term interest rates has not been related to inflation expectations. The rise has been in real rates, which implies that real growth expectations have improved.

Rental expenditures will rise with incomes, so housing supply must also.

If housing supply is elastic (easy to build), as it was in the mid-20th century, then rising incomes means more homes. Americans tend to spend roughly 10% of our incomes on housing. When American incomes were rising in the 20th century, we built more, larger, better homes to live in. The old existing homes filtered down. Over time, the initial residents of the older homes moved out and the new residents had lower incomes than the previous residents.

If housing supply is inelastic (hard to build), as it has been recently, then when American incomes rise, we must pay higher rents for the existing homes. Where supply is the worst, existing homes filter up. New residents tend to have higher incomes than the previous residents.

In the simple model I am using here, a 1% increase in interest rates would be associated with 5% future income growth. This is reflected in both panels of Figure 6. The effect on housing depends on supply conditions. The left panel reflects an elastic supply. More homes means that the rents of existing homes just rise at the rate of inflation.

This is orthodox economics. The scary real Shiller price index chart people have passed around for years now, and which Robert Shiller still updates monthly, is based on this point. The prices of houses shouldn’t appreciate faster than the general rate of inflation. That much is true enough. Unfortunately, Dr. Shiller has spent most of the past 20 years craning his neck around the elephant in the room to divine the cause of the divergence.

So, the left panel exists in the world that we don’t have, where rents (and prices) would rise at the general rate of inflation. The right panel exists in the world we do have, where housing supply has been broadly blocked, and rent growth is persistently higher than the general rate of inflation.

One way to anecdotally think about the left panel and the right panel is that in the left panel, by the time the family pays off the mortgage, their home will be more fitting for a family with much lower income. In the right panel, when the family has paid off the mortgage, the home will still be a home fitting for their income.

For the left panel, imagine a family who bought a home in the inner suburbs of Atlanta in 1970. For the right panel, imagine a family who bought a home in San Francisco in 1990. (Actually, closed access cities like San Francisco are frequently even worse than this.)

This is expressed through the mechanisms of this simple model through the rental expenses. In the left panel, rent starts at 30% of income, and after 30 years, it is down to 13%. In the right panel, it also starts at 30%, and after 30 years, it’s down to 17%. Thirty years of 1% excess rent inflation accumulates to rent that is 1/3 higher.

In the left panel, where future higher incomes mean more homes will be built in the future, the rent and mortgage payments in the future eventually take less income. Initial conditions are the same, though, except for the higher mortgage rates. The income growth will be in the future. So mortgage affordability is worse at inception. At inception, this looks just like the simple hypothetical where higher mortgage rates just increase the mortgage payment, and nothing else changes.

In the right panel, where future higher incomes means higher rents, the current value of the home reflects those future higher rents. So, the price/income ratio is higher. In this scenario, the initial mortgage payment is boosted both by the initial conditions of the higher mortgage rate and by the future conditions of higher rents.

The higher initial mortgage payments triggered by higher mortgage rates are mostly dependent on housing supply conditions. Richer families bidding up the rents of a stagnant housing stock 30 years from now mean that the mortgage payment today has to be higher.

The left and right panels are extremes. However, there are many markets that have been reasonably estimated by the left panel. The first hundred plus years of the famous Case-Shiller real home price chart are. It’s the most common market there is. It is the expectation. It is what Dr. Shiller thinks we should expect.

In some places before 2008 and in most places since then, we look quite a bit like the right panel - in many cases even worse.

The counterintuitive realization, which, to be honest, I didn’t fully intuit until I worked through these hypotheticals, is that when rising mortgage rates appear to be creating the most mortgage affordability stress, it is plausible that the stress is coming from supply constraints. It is plausible that these are the times we should least expect mortgage affordability to return to more comfortable levels.

The high initial mortgage payments are not really so much a function of high rates as they are a function of arbitrary amortization schedules and rent expectations about the future.

Conclusion

In short, it probably makes more sense, most of the time, to view mortgage rates as a function of sentiment and demand rather than a cause of it. High rates are associated with aspirational sentiment. Aspirational families demand aspirational homes in aspirational locations. And, they have to initiate that demand with stressful cash flows because of the mortgage products that are most widely available and because of poor housing supply conditions. (As I mentioned in a recent post, rate buy-downs are one way that builders can reduce the front-loaded cash outlays.)

Homebuilders are currently reporting concerns about high interest rates reducing demand and also difficulties finding labor and lots. I think this combination of concerns make more sense if we view high interest rates as a signal of strong economic sentiment and trends. There is certainly a type of buyer that will be constrained by the ability to fund a purchase under these conditions, and builders consult with those buyers and deal with those constraints every day. The stresses are salient. But, the idiosyncratic stresses exist within a broader set of economic relationships. A bullish market will be associated with high interest rates, even if the idiosyncratic countervailing stresses associated with high rates are visible and easily understood.

And, there is no doubt that if sentiment falters, if the Fed overtightens, if we enter recessionary conditions, all of that will certainly be related to lower mortgage rates, weakness in home construction markets, etc.

Reversing the causality makes it all make sense.

Mortgage affordability can be improved by lowering expected income growth, which will bring interest rates back down, or by encouraging more home building, which will bring future rents down. Surely, we can all agree, in the abstract, that the latter is the better choice. But this is the sort of thing that constrained housing supply does to us. It creates tempting scenarios where making ourselves worse off appears to be a solution.

Here, the temptation is to lower interest rates by lowering incomes. That is what happened in 2008, quite explicitly. It’s still the overwhelmingly popular stance about what was appropriate at the time, expressed in countless ways. Frequently it is expressed as monetary hawkishness. Sometimes it is expressed as anger toward corporations that attract skilled and well-paid workers to a housing constrained city. Sometimes it is expressed as anger toward foreigners or visitors. Housing starved Americans have found countless things to fear which would be obviously good in any scenario where we had enough homes.

In 2008, we were afraid of homes, themselves! We supposedly had a glut of homes in 2008 because Fed stimulus tricked families into thinking they were richer than they thought they were. In fact, we were poorer than we should have been because we were prepaying for the future inflated rents that we have implicitly agreed to enforce for the next 30 years. It sounds dumb to say it out loud, but we really did choose poverty over housing. I’m not being glib here. When you come to realize the housing shortage has been a binding economic constraint for decades now, you can’t help but painfully realize how explicitly policymakers and their critics chose poverty over housing - explicit policy choices to lower incomes until we hurt enough to acquiesce to our pitiful stock of housing.

I will have a post on this broader point soon - ethics in a context of deprivation. In the meantime, I hope you find the above figures useful.

Isn't one explanation for the Schiller "gap" simply ZIRP? It shows up in the price of equities, as well. In that sense, housing is like any other risk asset--it inflates when money is cheap.

The US population of working age adults--homebuyers and growth-makers--has been flat-to-down since ~GFC. We've had unit-growth (supply) in excess of people-growth (demand) for ~15 years, and yet prices have gone up, coincidental with rates coming down. I understand the supply-side arguments--I really do--but the elephant in the room is on the demand side. There is at least some evidence that when people-driven demand growth came to an ebb, cheap money stepped in to fill void (and has been doing so ever since, until just recently).

More here: https://www.therandomwalk.co/i/120973131/consider-the-everything-bubble