Home Price Trends Point to a Worsening Lack of Supply: Part 3

Generous mortgage markets made housing cheaper.

In Part 1, I explained how severe urban supply constraints in some locations mean that even moderate increases in per capita demand for housing lead to distressed migration. If housing is relatively fixed and housing/capita rises, then population must fall. And it does in the failing cities like New York, Los Angeles, San Francisco, and Boston.

In Part 2, I explained how post-2008 housing markets in most American cities underwent the strange following series of trends:

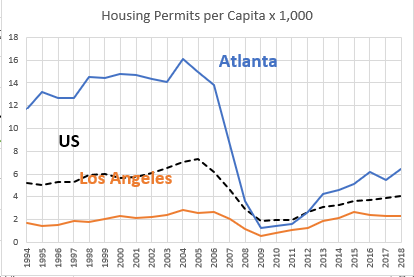

Moderate construction activity, prices, and rents until 2006 (Actually, rents in many normal markets were becoming more affordable. As I have written about extensively, the 2000s housing market has been highly driven by fundamentals. For 25 years, rents have been an increasingly important factor driving prices. So, where prices were moderate before 2008, rents were generally becoming more affordable. Figure A below compares rent inflation (blue) in Atlanta to core CPI inflation (red) and Atlanta housing production (green, right). The last time Atlanta built sustainably, briefly, was from 2001 to 2005. Then, initially rents increased when construction started to collapse before the crisis. Then rents declined again briefly during the depths of the foreclosure crisis. Then, the long period of stagnant construction and rising costs set in.)

Collapsing construction and prices

Rising rents and prices

Mortgage access, money, and speculation were blamed for all of the problems that were created by the lack of adequate housing in the expensive cities. In paper 3 of this series of papers, I was able to quantify an estimate of the effect of credit access. The existing literature ignores, doesn’t try to quantify, or treats inadequate supply as an aggravating control variable playing second fiddle to credit markets during the boom. If you give supply its due, as you can using my analytical framework, it clearly takes center stage. But, credit was a factor. I think my estimates of its affects are higher than some of the existing literature that has focused on its importance in the boom. In fact, my analysis would say that loose credit was inflating home prices in Atlanta more than in LA. You have to fully control for the effect of supply on home prices in LA, which with a decade’s hindsight, clearly doesn’t require loose credit markets to push low tier prices up. And, remember that families that require generous mortgage access were exiting LA by the hundreds of thousands at the time. So in paper 3 I argue that loose lending did push up prices, but mostly in places where prices were still relatively moderate.

But, also, I am attributing rising costs in cities like Atlanta after 2008 to the tightening of mortgage access.

How can both loose lending and tight lending cause prices to rise? Figure 10 from the paper is a starting point.

Think of 2 extremes - a perfectly elastic housing market where the price can’t rise higher than the cost of new construction and a perfectly inelastic housing market where the number of homes is fixed. Think Atlanta and Los Angeles in 2002.

Finance is about yields. Income/capital, or, in real estate we tend to talk about the inverse, price/rent. If loose lending raises prices, it does it by reducing yields - by removing financial frictions so that more families can buy homes. An analogy would be the price/earnings ratio on a stock. Stocks with more liquid markets tend to have higher price/earnings ratios.

In the perfectly elastic market, the price is fixed by the cost of construction, so a rising price/rent ratio can’t make the price increase. It can only act by reducing rents. Exactly what was happening in Atlanta in 2005!

In the elastic market, it is rent that is anchored by demand for shelter, so in inelastic markets, mortgage access or rising incomes only push up the price. If anything, more liquidity in the buyer marketplace increases demand for housing per capita of families with higher incomes and access to capital, which leaves less room for families with fewer resources. Exactly what was happening in Los Angeles in 2005!

What happens if mortgage access tightens? It will lower the price everywhere, and especially lower prices where incomes are lower and mortgage access is more binding. (See Figure 12 and 13 from the previous post.) It won’t affect construction much in the inelastic market, because construction was bound up with local politics already. Supply will become inelastic in the formerly elastic market because the existing stock of homes will be fixed in place and the price won’t be high enough to trigger building more. So, construction will recover to the previously paltry levels of the inelastic market and it will collapse in the formerly elastic market. Just like in Atlanta and Los Angeles after 2005 (Figure B)!

As I wrote about in the previous post, since both markets now have inelastic supply, both will have high rent inflation. And they did!

These are really peculiar construction, rent, and price trends. Could they be explained by other commonly reported factors?

Mortgage interest rates, which were low and generally declining until 2022

I have written extensively at the tracker against this thesis. But, for believers, this is really mostly a question about levels. If anything, the correlation between mortgage rates and home prices has been positive for most of the last 25 years. (Higher prices when rates are higher.) So, to attribute a lot of power to mortgage rates, you have to believe that high prices before 2008 were mostly from something other than low rates, which was corrected for between 2007 and 2012, and then, after that, low rates led prices to be excessively high again, raising them back to the high levels of 2005. This will require a creative use of lags, but it retains the benefit of the doubt in most circles.

Readers will recognize this Figure 18 from previous posts. The mortgage rate proponents don’t seem to consider production. I’ve written quite a bit about how obstructed housing supply leads to distressed migration when there are changes in per capita housing demand. You can see in Figure 18 that before 2008, those changes were barely perceptible.

The trend change in per capita housing production after 2008 is epic. How could prices driven in the slightest by stimulated buyer demand from low rates lead to such a shift? It’s frankly ridiculous, and if there was any piece of evidence this stunningly against my thesis, nobody would have read the Erdmann Housing Tracker for more than 5 minutes, and rightly so. It would be like if LA and New York had suddenly started permitting 15 units per 1,000 residents after the turn of the century and I hadn’t noticed it at all.

Keep in mind that before 2008 when people like Ed Leamer or John Taylor would argue that home prices had been driven higher by low interest rates, they would argue that it led to oversupply, because of those squiggles in real per capita housing consumption that are now imperceptible compared to the epic trend shift to less consumption. Even then, they were wrong about oversupply. But boy howdy, the subsequent decade has not been kind to the “overstimulus” thesis, though this doesn’t seem to have dampened its popularity.

Housing demand due to COVID-19 migration and changes such as more working from home

These rent and price trends were already in place well before Covid struck. The Closed Access cities were already entering negative population trends before Covid struck. And, as far as the receiver cities go, instead of building more homes, their prices and rents increased when newcomers showed up. Something has changed in supply conditions. The total demand for housing that has driven prices higher hasn’t even been moderate. It’s been tepid. Historically low. Covid factors have influenced demand in the short run but there was a larger story to tell before Covid showed up.

Supplier consolidation

The post-Covid period has done us the favor of demonstrating that, given demand, the homebuilders are more than willing to not only produce up to their physical capacity to do so, but even to bid up the price of inputs when they hit capacity. Construction didn’t collapse in Atlanta because of industry consolidation, though certainly a causality in the other direction is plausible.

Changes in the cost of construction due to regulation or market forces

This is probably the most plausible of these four alternative explanations. And, certainly, to an extent, costs have risen. But, higher costs create a different outcome than politically obstructed supply.

These panels from Figure 21 demonstrate what I’m talking about. Obstructed local supply creates a musical chairs process where the most vulnerable families are pushed out. It creates this predictable pattern in local prices/income ratios as intra- and inter-metro migration is required because of a lack of supply, and prices have to rise high enough for families to volunteer under duress to be displaced. Every city is becoming more like LA.

Think about it historically, too. These strong differences in price levels are a recent phenomenon. Before the 2000s, there wasn’t much of a difference in price/rent or price/income ratios between different metro areas or within them. We are richer than previous generations. Relative to our incomes, costs are much lower than they had been in the 1980s or 1970s, etc. Yet, these patterns didn’t exist back then. Higher cost of construction leads to lower real consumption, smaller units, etc., not regional distressed migration.

Also, these steepening price/income relationships happened mostly from 2012 to 2020. When input costs surged after Covid, rising costs did what rising costs do, they increased home prices in all income ranges. As subscribers to the Erdmann Housing Tracker know, on average the slopes of these price/income relationships stabilized after the spring of 2020. Price increases were universal rather than from steepening price/income differences.

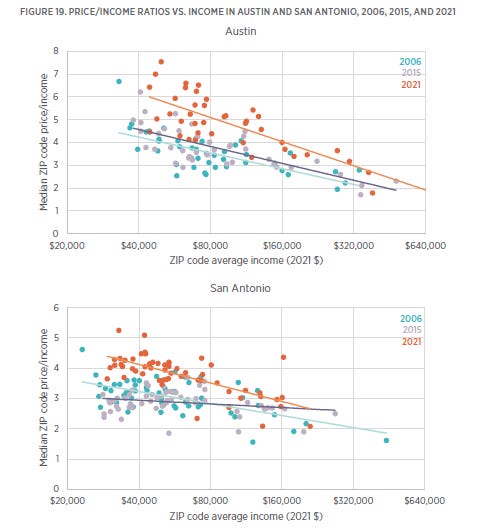

Finally, regarding the interaction between mortgage access and incomes, Austin and San Antonio provide an interesting example. They are two markets that interact quite a bit, being just down the road from each other. Austin has especially high incomes and San Antonio has especially low incomes.

As Figure 19 shows, from 2006 to 2015, the price/income slope was barely affected in Austin. In San Antonio it was sharply flattened. Austin’s price/income line has steepened a bit since 2006, as has San Antonio’s. But San Antonio has had the tell-tale back and forth of a credit constrained market.

Also, rents have risen more, especially at the bottom end, in San Antonio - again, a sign of income-sensitive supply constraints related to mortgage access. Low tier rents had to rise in San Antonio for prices to rise as they did in Austin because limited mortgage access lowered relative price/rent ratios more in San Antonio.

Finally, shown in Figure C, construction in Austin has recovered to levels higher than those of 2005. San Antonio construction rates fell to a fraction of the 2005 level, and have only recently recovered, but still at levels below the pre-2008 peak. Weird, given that high rent inflation, unless, of course, tight mortgage markets bite more there, pushing down price/rent ratios more and making it harder to justify building.

From the paper’s conclusion:

It could be that cities, in general, were overregulating the construction of multiunit and urban infill housing even before 2008, and that loose lending simply put a Band-Aid over that problem by financing an excess amount of entry level, single-family construction. When financing for those homes was pulled back after 2008, the underlying constraints may have been exposed, so that no city has been willing and able to approve enough multiunit and urban infill construction in the absence of that financing.

It is likely that hysteresis from the decade of suppressed construction activity lowered the capacity to build, which has only recently been retested. The recent development of an institutional build-to-rent market in single-family tract home construction suggests that prices have now fully moved into the righthand scenario of figure 11. Continued tight mortgage access means that the new supply will be financed by landlords rather than by owner-occupiers.

An increase in either multiunit or build-to-rent single-family construction may stem further steepening of negative price/income slopes, but it remains to be seen whether that activity will reverse the steepening or the significant increases in rents and rent/income ratios. It is plausible that the costs of landlordship require higher rents and that a market that depends on more rental units will settle at higher rents. Both theory and recent practice suggest that in a market with elastic supply, the primary net effect of generous mortgage access may be lower rents for nonowner tenants.