The Cheat Code for Understanding Housing

An update on rents and prices

One fundamental point that readers can take away from my work, which will give them a leg up on financial traders, economists, etc. is that inflated rents cause prices to inflate more. In other words, high price/rent ratios are almost entirely due to high rents.

As far as I know, academic and policy papers largely are written in ignorance of this. Much of the existing economic literature on recent housing volatility is based on the inappropriate presumption that price/rent ratios should be stable, and that when they change it is due to unsustainable changes in prices. It’s a big reason why the supply crisis gets misdiagnosed as an overly cyclical market.

Anyway, long-time readers know this. I revisit it quite a bit. It’s basically the point of the first of my series of 4 Mercatus papers.

More recently, one way I have framed housing valuations is basically as a combination of two multiples, both of which are relatively stable over time. The valuation multiple on structures, which tend to sell for about 12x annual rent. (Or, maybe it is more accurate to say that they rent annually for 1/12 the cost to build them.) And the valuation multiple on land (which includes many elements like location, endowment value, local amenities, quality of neighbors, etc.), which tends to be about 36x annual rent.

I thought it might be worthwhile to take a look at current valuations to see how this continues to be the case.

Aggregate US Price/Rent

Figure 1 is an example of the common error. It’s a shame I don’t have much reputational capital or a larger megaphone, because there’s just so much stress, fear, and mistaken policy responses out there from this. On the bright side, using this information will probably provide opportunities for trading alpha well into the future, because it will be our little secret.

This is a chart of a rent index and a price index. And, what this looks like to intelligent people who don’t know about the price/rent issue is a market that was 39% cyclically overvalued, which briefly corrected to normal, and now is cyclically overvalued by 53%.

The right way to read Figure 1 is that a multiple should be applied to the excess part of the rising rent. A properly multiplied rent index would rise roughly together with the price index in the 2000s. Then, the mortgage crackdown put a permanent 20% shock in the price index from 2007 to 2012. From that point on, the properly multiplied rent index would continue to rise at a level roughly 20% higher than the price index.

Figure 2 expresses this process as a ratio - price/rent. In the 1970s, most real estate value was in the structures, so the aggregate price/rent ratio wasn’t much higher than 12x. There are some cyclical fluctuations. But, the cyclically neutral price/rent ratio was probably around 20x by the 2000s and would be in the mid-20s by now.

Now, you have to be a little bit careful with the counterfactual here. Rents would be a lot lower if we hadn’t had the credit shock. If residential construction had continued strong after 2005 instead of crashing, the neutral price/rent would have levelled off or possibly started to decline a bit.

By temporarily pushing price/rent down by pushing down prices, we permanently pushed price/rent up by creating rising rents.

Sorry. I didn’t intend to make this post a cipher. If that’s confusing to you, the only thing you need to know is that rising rents cause price/rent ratios to rise.

Price/Rent Among Cities

In 2022, I wrote 7 posts showing that any apparent correlations between price/rent and mortgage rates are spurious and that over time, rising prices, any way to cut it, are climbing up the price/rent escalator as rents rise. (1, 1A, 2, 3, 4, 5, 6).

How do prices and rents look today? The story is the same as it was in 2022.

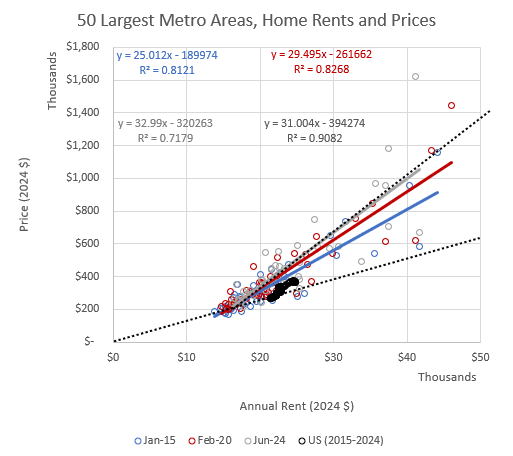

In Figure 3, annual rents are on the x-axis and prices are on the y-axis. There are two black dashed lines. The lower one reflects the 12x price multiple that would apply if all value was from structures. The higher, steeper dashed line reflects a roughly 36x multiple for excess rent reflection non-structure sources of value.

These are expressed in 2024 dollars, but instead of adjusting it for inflation, I have adjusted it for average income, since the rents and prices are Zillow estimates, which change compositionally as population grows and new homes are built.

Figure 3 shows the Zillow median rents and prices for 50 metropolitan areas. At any time before the mid-1990s, the median values for all American metro areas would have been down at the base of this group - around $20,000 annual rent or less and generally well below a median price of $400,000.

That is because when there is not a supply shortage, land doesn’t become overvalued, and Americans pay a relatively predictable portion of our incomes for shelter in that context. Shelter - structures - tend to have a valuation multiple of about 12x annual rents (give or take some differences due to property tax rates, etc.).

So, the variance between cities is new. Where there is variance, it is due to inflated land values because of supply obstructions. And, so, where there is variance, the median home value rises in proportion to the higher valuation multiple associated with land.

At any point in time, the least supply constrained cities remain moored near that anchor point. There are very strong natural forces to pull them there. Where those forces are blocked, they move up and to the right.

So, home prices don’t deviate much from year to year, except for where rents are rising. Really all of the variance in prices is just from rents that rise and push home prices up that steep gradient associated with inflated land value.

The little line of black dots is the median price and rent for the US, over time, from 2015 to 2024. You can see that it was near the 12x line in 2015 and has risen up above it since then. That deviation reflects the rise in price/rent in Figure 2 from 2015 to 2024.

The variance between cities is much greater than the variance over time of the median US home, so the shift in the US median numbers in Figure 3 is dwarfed by the differences between cities, but you can see in the regression equations that, over time, a $1 increase in excess rent in the US leads to about a $30 increase in home values. And, at any given point in time, a city with $1 higher annual rents will tend to have about $30 higher home values.

(The US median price tends to run a bit lower than the mean of the individual cities, likely because of data coverage and skewness.)

Price/Rent Among ZIP Codes

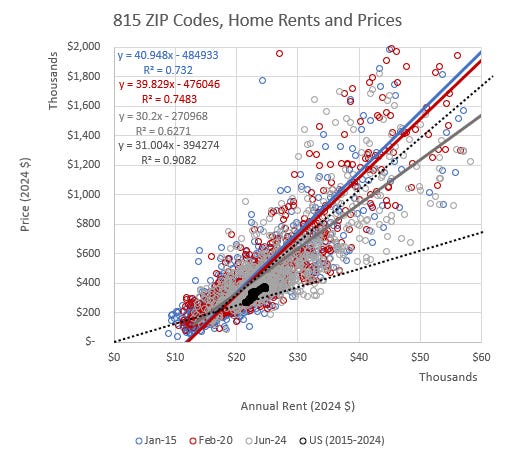

Here, let’s cut a little deeper. Figure 4 looks cross-sectionally at prices and rents in 815 ZIP codes across the US. Here again, the black dots are the US median figures over time.

If the US didn’t have a urban housing supply crisis, the US time series - the black dots - would not move. They would just hover in a single spot around $15,000 annual rent and a $200,000 or so price, year after year after year (just rising in line with incomes).

But, since the supply crisis is pushing rents up excessively, the US dots are moving to the right over time. And since the dots are moving to the right, they are also moving up at a ratio of about 30:1, from the baseline ratio of 12:1.

Even at the ZIP code level, there is no fundamental change in the relationship of actual rents and prices.

Let me put it this way. From Figure 2, the US aggregate Price/Rent ratio was about 16x in 2015, about 18x in 2020, and about 20x or 21x in 2024. Or, from Figure 1, the aggregate US home price/rent ratio was elevated about 40% in 2024 compared to 2015.

But the regression lines in Figure 4 are basically identical in 2015 and 2020 and the regression line is lower in 2024. In other words, the expected price of a house with a given rental value has remained the same or declined at all three points in time. The only reason the aggregate price/rent ratio has increased is because the rents have increased. The dots moved to the right, so they also moved higher.

Figure 5 can help simplify. As you can see in Figure 4, the density of ZIP codes with annual rents above about $40,000 and prices above about $1 million is lower, but because they are further from the mean, they have a large influence on the regression. Idiosyncrasies changing the relative valuations of these very high-tier neighborhoods, especially during the volatile post-Covid period, can be adding more smoke than light here.

So, in Figure 5, I have removed the ZIP codes with 2024 annual rents above $40,000. I also removed the 2020 plot to clear up the chart a little bit. Now the regressions reflect the correlations for the remaining 90% of the ZIP codes that are more reflective of typical systematic trends.

After removing the very high-tier ZIP codes, the regressions look a lot like the pattern in Figure 3 between cities. ZIP codes with annual rents up to about $15,000 are moored to that 12x natural valuation multiple. And from there ZIP codes with $1 higher rents tend to have $30 higher valuations.

After excluding the very high-tier ZIP codes, the regression lines for 2015, 2020 (not shown in Figure 5) and 2024 are all nearly identical.

The national numbers in Figure 2 imply that a home with $20,000 annual rent would have sold for $320,000 in 2015 and about $410,000 in 2024. But, as you can see in either Figure 3 or Figure 5, at both times, the typical home with $20,000 annual rent would have been associated with a price of about $320,000.

Price/rent levels have not been changing. Rents have been rising excessively. So, the aggregate US statistics over time are changing compositionally. The US aggregate time series isn’t measuring like with like. It used to be a measure of home values. Now it is mostly a measure of elevated land values.

And, you can see what has happened in Figure 5. The dots moved quite sharply to the right (and, thus, up) from 2015 to 2024. The cheapest rents (adjusted for income growth!) have generally increased by more than 20% since 2015.

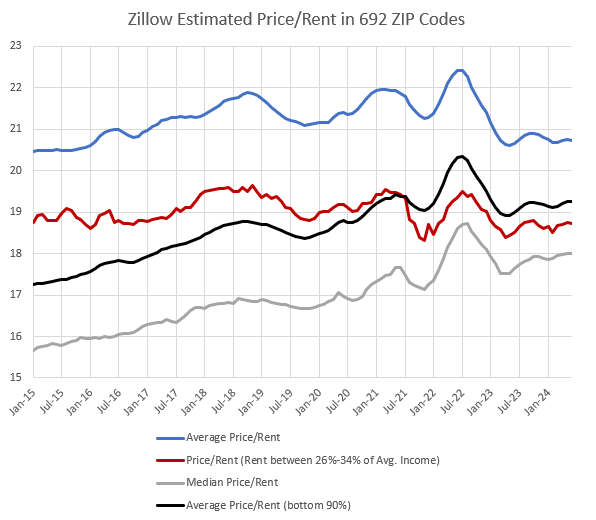

Finally, in Figure 6, using the Zillow rent and price data for 692 ZIP codes that have data every month from January 2015 to June 2024, I compare the aggregate median price/rent, the average price/rent, the average price/rent for the bottom 90%, and the price/rent for ZIP codes where rent takes between 26% and 34% of the average reported income.

The median price/rent and the average price/rent of the bottom 90% of ZIP codes show similar patterns as the aggregate national data in Figure 2. The average price/rent of the bottom 90% starts at about 17x in 2015 and rises to above 20x by 2022. The average price/rent follows a similar pattern except that in the post-Covid period since 2022, it reflects the anomalous pattern from Figure 4 where some prices of very high-tier ZIP codes have declined sharply.

But, the price/rent of a ZIP code where rents cost close to 30% of the average income has remained about 19x, plus or minus a couple tenths of a point, for the entire period.

If you earned the average income and wanted to live in a house that would take 30% of your income for rent, on average, that house would have had a purchase price about 5.7x your annual income. This has been the case for a decade. Your main problem would have been that you would need to keep trading down to worse houses in order to keep the rental value at 30% of your income.

The aggregate price/rent ratio has only gone up because rents have gone up.

The only correction that could possibly fix this is lower rents! Moving those dots back to the left. And the only way to do that is to grind out millions of additional homes, year after year, until we do.

I know that it’s hard to switch gears on this. For 25 years, the newspapers, libraries, and journals have been full of valuation stories. The valuations are too high, and so we have to stop mortgage lending or stop speculation or stop foreign buyers or stop corporate buyers or whatever.

There is no valuation story!

There is NONE.

The narrative doesn’t have to be a binary exclusive story. There could be a demand-side valuation story and a supply story. It’s a complicated world. But it is binary. In any way that matters, it’s all rent. It’s all supply. There is NO valuation story. There HASN’T BEEN a valuation story.

This is your cheat code. While your counterparties are working out their models to try to divine how excessive the valuations are, you can spend all that time doing something useful, analyzing something that actually exists, or learning something relevant. And then, when you finish learning, and decide that you want to make some investments, they will sell some of those investments to you at a discount, because of their estimates of the excess valuations.

There are a lot of analysts and economists who have built a worldview around the valuation story - loose money, loose lending, etc. Generally, they simply will be unable to accept this. That’s understandable. It’s not easy to accept a fact that undermines a hundred other things that you have considered to be axioms. So, I think there will be profitable trades from this cheat code at least as long as I’m kicking around.

Just pray to high heaven that JPow! fends off the valuation proponents that make their way onto the FOMC. I only wish we could keep them out of the FHFA and CFPB, but that ship has sailed.

PS: Here’s a follow-up post where I get to the bottom of why excluding the highest rent ZIP codes makes the results more stable. I find the answer quite interesting.

PPS: This chart is for a comment.

So, after 100 years of zoning regulations and other anti-supply measures, the final equilibrium of the U.S. economy can be summarized as follows:

-Productivity and efficiency gains in all areas of the economy EXCEPT real estate can result in a stabilization of prices and eventually have no impact on inflation.

-Land prices, and the purported value of single family homes, can appreciate perpetually at a range of 5 to 8% annually.

-Exceptions to the land & house price appreciation are tolerated for geographic areas that are experiencing population decline and/or environmental devastation---unless political influence deems that they will be perpetually insured by taxpayers.

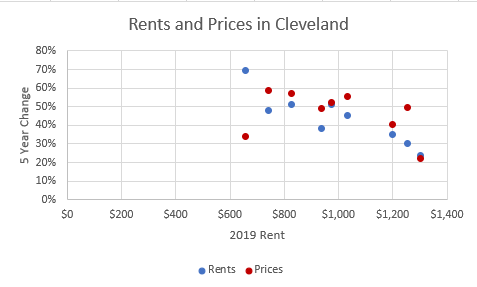

How would you explain the situation in a city like Cleveland?

Cleveland has one of the very lowest Price/ rent ratios, but also has some of the fastest YoY rent growth.

Does this simply represent a lag before home prices shoot up, or is there a different dynamic at play in this market since it is not growing?