Valuations, Density, Rents, and Incomes

I have happened upon something really interesting which I think corroborates my point about high price/rent ratios and may resolve some other mysteries.

In the previous post, I wrote about how home values are surprisingly stable as a function of rents. When rents are inflated by local supply barriers or are due to amenities not related to the actual structure, they fetch higher price/rent multiples. The entire increase in the aggregate price/rent ratio of American housing over time is due to higher rents from urban scarcity.

This creates a difficult situation for pundits, economists, and analysts. They generally view high price/rent ratios axiomatically as a sign of unsustainable buyer demand, so so they are systematically misguided, constantly convinced that a supply problem is a buyer demand problem.

Anyway, as I was working through that post, I discovered some odd price trends in ZIP codes with high rents. Since the end of 2020, prices have been sharply declining in ZIP codes with high rents.

And, it turns out, that is a spurious correlation. Prices have been sharply declining in ZIP codes that are densely populated, and dense ZIP codes tend to have high rents.

I have previously looked at the interaction between density and the Erdmann Housing Tracker components. As I mentioned in the previous post, density is an inferior good. Poorer residents tend to live in the densest parts of the densest cities. But, they pay more for it. This is likely related to the value of public amenities like mass transportation.

Most of the time, the value of density is relatively stable, and so it doesn’t matter much if I control for it in the tracker. But then Covid came. Rents and prices in dense neighborhoods have been cratering. They still are, as far as I can tell.

When I looked at the issue with the Erdmann Housing Tracker in mind, it didn’t matter that much outside of New York City. The tracker uses ZIP code incomes and metropolitan areas as the independent variables. Most American cities don’t have urban amenities that are developed enough to create the value that attracts poorer residents to dense cores. The only places where the sudden shock to the value of dense urban real estate mattered much for the tracker were New York City, and to a lesser extent a few cities like San Francisco and Chicago. So, I stopped poking around the data too soon before I discovered the full extent of the recent changes.

Seeing the odd results in the previous post led me to take a fresh look at the data. And, in the meantime, property values in dense ZIP codes have continued to plummet.

The Collapse of Dense Home Prices

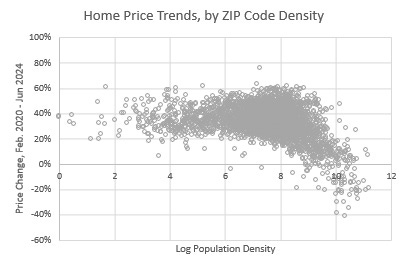

Figure 1 shows the (continuously compounded) change in home prices since December February 2020, by ZIP code density. Prices in most of the country have moved up about 40% (give or take 20%), unrelated to density. But above a density of about 4,000 homes per square mile, home price trends have had a strong negative correlation with additional density.

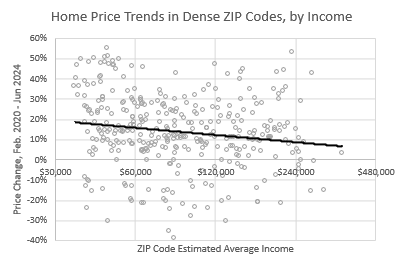

The relationship between price changes and local incomes is somewhat weak. It’s hard to see it in the plot in Figure 2. But, the trendline in Figure 2 shows that the exodus is somewhat correlated with incomes. Figure 2 shows the change in prices in the densest ZIP codes with more than 8,000 homes per square mile. There appears to have been a decline in demand for density among the residents with the highest incomes. Demand for density has gotten inferiorer, as it were.

The Effect of Supply Scarcity and Amenity Value on Price/Rent Ratios

This brings us to the previous post. When I isolated only ZIP codes where rents were equal to about 30% of average national income, the price/rent ratio has remained within a few tenths of a point of 19x since 2015. The aggregate national price/rent ratio has increased over time because excess rent inflation is accumulating over time. But, holding rent stable, price/rent ratios are also stable.

One way to put it is that the scarcity value is rising all over the country, so rents and price/rent ratios are rising all over the country. But, substituting down to a home with less amenity value would counteract the change in rent and price/rent ratios.

A home that would take 30% of the average households income sells today for a price/rent of about 19x. You could say the same thing about a house that would have taken 30% of the average household income in 2015. But, the 2015 house would have been a relatively better house. The house with those characteristics would have had more amenity value. Today, the 30% rent/income and 19x price/rent house has less amenity value and more scarcity value. It would cost more because there aren’t enough of them, so you would need to live in a worse neighborhood to keep the economics the same.

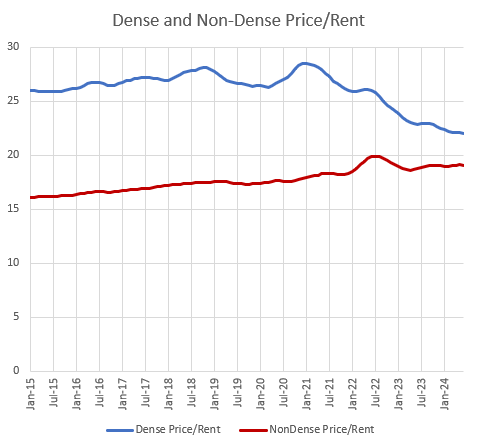

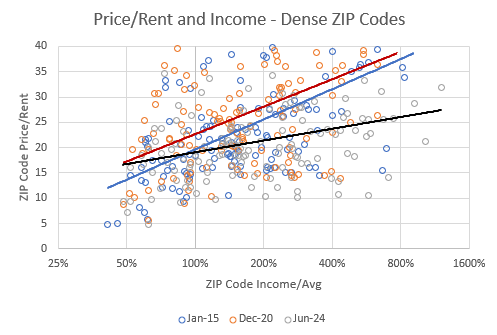

Figure 3 is one way to try to get at this. Here, I have just taken the average price/rent ratios of the 133 densest ZIP codes and the 305 least dense ZIP codes for which I have rent (Zillow), price (Zillow), density (collected by Salim Furth at Mercatus), and income (IRS) data for every month since January 2015.

The least dense ZIP codes have just generally climbed over time as rent inflation has accumulated. The price/rent ratios in the most dense ZIP codes were flat or rising until Covid hit, and then they started falling off a cliff.

I think what we’re seeing here, which is clear when I segregate the ZIP codes by density, is that two countervailing forces have been at play in the aggregate numbers. Scarcity has continued to raise rents, prices, and price/rent ratios in general. But, at the same time, a loss of urban amenity value has caused rents, prices, and price/rent ratios to decline in dense ZIP codes.

In Figure 4, I have taken the average rent/income and price/income ratios of the 133 densest ZIP codes and the 305 least dense ZIP codes. This breaks down the reason for changing price/rent ratios. Was it a change in rents or a change in prices?

The densest ZIP codes are the blue lines. Rent/income (dark blue) on the left axis and Price/rent (light blue) on the right axis. The least dense ZIP codes are the red lines.

Rents have generally taken a rising portion of incomes in non-dense ZIP codes. And, as rents have risen, prices have risen even more. (The light red line is catching up to the dark red line as the each rise.)

Rents in dense ZIP codes were flat or slightly rising before Covid, and so were prices. There are a lot of tricky things going on here, but I would guess that the relatively higher price level in dense ZIP codes relative to non-dense ZIP codes is related to density amenities, and amenities raise the price/rent ratio.

After Covid, urban amenity value declined, and rents declined in dense ZIP codes. When that happened, prices also declined. And they declined more steeply than rents did! We should expect this! This is the thesis of the previous post. Where changing rents are unrelated to the size and quality of the structure, effect on prices is multiplied.

This is also what would happen if a decline in scarcity value led to lower rents.

Figure 5 shows that since Covid arrived in 2020, rents have continued to increase in the least dense ZIP codes, and so prices have continued to increase even more.

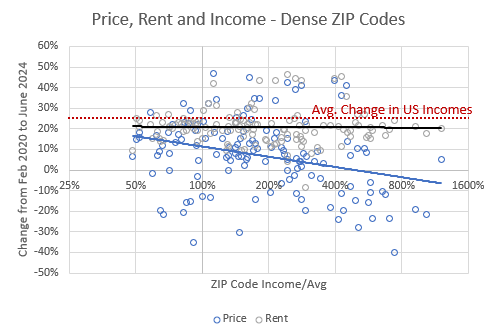

Figure 6 shows that rents in the densest ZIP codes have not risen as fast as the average US income since February 2020. So, prices have risen even more slowly. And, in the richest dense ZIP codes, prices have declined. We will have to watch as time passes to see if this is a temporary divergence, and if it closes through declining rents or recovering prices. (This is partly noise, I think. The number of ZIP codes with rent data is smaller, so the number of data points in Figure 6 is smaller than in Figure 2. And, the decline in prices in Figure 2, with more ZIP codes, isn’t as highly correlated with income.)

Figure 7 shows the effect of these changes on price/rents. In the least dense ZIP codes, price/rents are rising. Keep in mind that this would happen even if nominal rent expenditures level out, as long as rent inflation remains high. If families keep rents under control by downsizing, it will still be the case that more of their rent would be rent on the lot rather than rent on the structure, and so it will fetch a higher premium. This may finally end if home construction can start to rise again.

Figure 8 shows that price/rent had a similar pattern in dense ZIP codes (with much more variance reflecting the wide range of amenities and disamenities dense locations have). Since Covid, price/rent ratios of the richest, densest ZIP codes have fallen sharply.

Some Technical Notes about the Effect on the Erdmann Housing Tracker

This is probably too into the weeds for just about everyone, but here are some parting thoughts.

Seeing it this way, I think this probably is more of a problem in the Erdmann Housing Tracker data than I had accounted for. It doesn’t show up enough in any single city, except for New York City, to make a noticeable difference, but I think the small effect the decline in demand for dense housing has in every city, in a way that is not correlated with incomes, has just generally lowered relative prices across each city, and has probably caused the Supply component of the tracker to flatten out more than supply conditions on their own would have.

And, I have to estimate income changes for the most recent couple of years because the IRS reports ZIP code data with a lag. This has been challenging because of the abrupt changes in incomes related to Covid fiscal responses. In reviewing this data, I have also determined that I have probably been underestimating incomes a bit, which causes the Cyclical Component of the tracker to be overstated. Once I adjust the income estimates, the Cyclical Component will be a few percentage points lower, and will be below a neutral valuation.

New York City does have extensive enough density amenities that there is a negative correlation between density and incomes, which causes the opposite effect there. The declining demand for density has caused prices to decline in neighborhoods that tend to have lower incomes. This is a bit confusing. Prices in the richest dense ZIP codes in New York City have declined the most, just like they have in other places. But, as Figures 5 & 6 showed, rents and prices have declined more in all dense ZIP codes than they have in less dense ZIP codes. And New York City has a lot of dense ZIP codes with low incomes and a lot of rich, less dense ZIP codes.

The effect this has on the regression I use for the tracker is to make the New York City Cyclical component look higher and the Supply component look lower. So, it is true that housing in New York City has gotten cheaper in poorer neighborhoods, but it’s not cheaper because of added supply. It’s cheaper because of lower demand for density amenities.

But, I think both the flat Supply component and the low Cyclical component (after I adjust income estimates) both simply reflect a true loss of amenity value in the American urban housing stock that is related to Covid. Households are less willing to pay to live in cities. I’m not quite sure how to account for this in the tracker data. For now, I will probably just make note of it.

There has been a bit of a mystery in the tracker data since the arrival of Covid. Rent inflation, measured by the BLS and by Zillow, has continued to be elevated. But, the Supply component of the Erdmann Housing Tracker has flattened out, suggesting an end to excess rent inflation. The effect of the decline in the value of density might explain this. My Supply component has likely been understating the continuation of rent inflation.

Very wonky, but you made it understandable, thank you.

One of the biggest and critical density amenity value is access to (better) employment opportunities. It could be that this is declining in both rich and not rich, for different reasons. In the rich dense zips, remote work has reduced the density value. In the poor dense zips, service job opportunities have declined with less office occupancy (as a significant portion of the services is to office workers). Food for thought.

I enjoyed your journey through the weeds.