January 2024 Erdmann Housing Tracker Update

OK. I think I’ve gotten to the bottom of some of the mysteries in recent trends. Some of what I had tentatively hoped was a California YIMBY miracle and much of the mysterious recent affordability improvements in New York City are probably related to the Covid flight from cities, the work-from-home phenomenon, etc.

First, the basics for this month. The boring housing market continues. Rents and prices rose moderately, on average, for another month. As I have noted in many previous posts, this is mostly just a mechanical supply and demand trend, which moved up along with the transitory rise in general inflation. There are some brief diversions between prices and rents, which, if you really want to, you can ascribe to things like interest rates.

Figure 1 is a poor man’s (or lazy man’s) picture of these trends. When rents are increasing at a faster pace than other prices, home prices rise along with them, but at a greater than 1:1 pace. If we match up the US rent and price trends from 2015 to 2019, then, after a blip or two, they end up matching right up again. This poor man’s chart is cheating a little bit on the details, but this is the basic story. Rising rents are causing rising prices, and the period of transitory inflation in other prices is just a blip in that path. For the most part you can have a better grasp of the national housing market by ignoring a lot of the big stories about what is driving the housing market and just keep it very simple.

I have been calling this the boring market because good macro-economic management kept housing construction stable through Covid. Between that and declines in population growth, it has looked to me like housing production is finally at the low end of a sustainable pace, and future expansion might finally, slowly, reverse some of our supply shortage.

As I have mentioned in my recent inflation posts, it looks like rent inflation is bottoming out at a slightly higher level than we might have hoped. One tricky aspect is the estimate of population growth. Much of the trend has been and will be driven by immigration, which has been highly variable through Covid and the changing presidential administrations. And much of it may be undocumented, so it is hard to track. It is possible that it has recently increased substantially.

Even top end estimates of migration will add up to a population growth rate no higher than the typical growth rate over the past century, so there is no reason why housing can’t keep up. But, it would explain why rents might rise at any given level of production.

What’s Going on in New York City?

So, you might think that the opening paragraph is a bit silly. Of course fleeing the cities and work-from-home shifts have been affecting home prices. But, the Erdmann Housing Tracker looks specifically at changes in home prices that correlate with local incomes. Inadequate supply systematically raises costs on locals with lower incomes who are willing to pay more for housing to hold onto the idiosyncratic endowments of location. This isn’t an observation about simple, average price appreciation. It is an observation about a peculiar type of price appreciation.

The Covid era shifts in housing demand have been specifically related to the value of population density that is positively related to incomes and the negative externalities associated with density. As I have discussed in previous posts, I think the way economists discuss urban density is too simple. There is obviously productivity value from living in some large cities which attracts workers who earn high incomes. But, the straightforward agglomeration story is outweighed by the complications ignored by that narrative. Within dense cities, density is an inferior good. The poorest neighborhoods are generally the densest neighborhoods.

For the tracker, this gets tricky, because inadequate housing supply raises costs on the poorest neighborhoods the most. When that happens, in cities with dense urban cores, it also raises the cost of dense housing. So, the value of density and the cost of inadequate supply have a spurious correlation.

I have elected to “Keep the tracker simple, stupid” by simply tracking the relationship between regional housing costs and incomes. In some ways, controlling for things like density or different property tax rates can produce a more valid estimate of local supply conditions.

Generally, local density in American cities is so unimportant that a density control hasn’t mattered much. And it would be really hard to control for because the relationship between density, home values, and local incomes has varied from city to city and over time.

But, I think, in this instance, changing demand for dense housing has created some false flags in the tracker data.

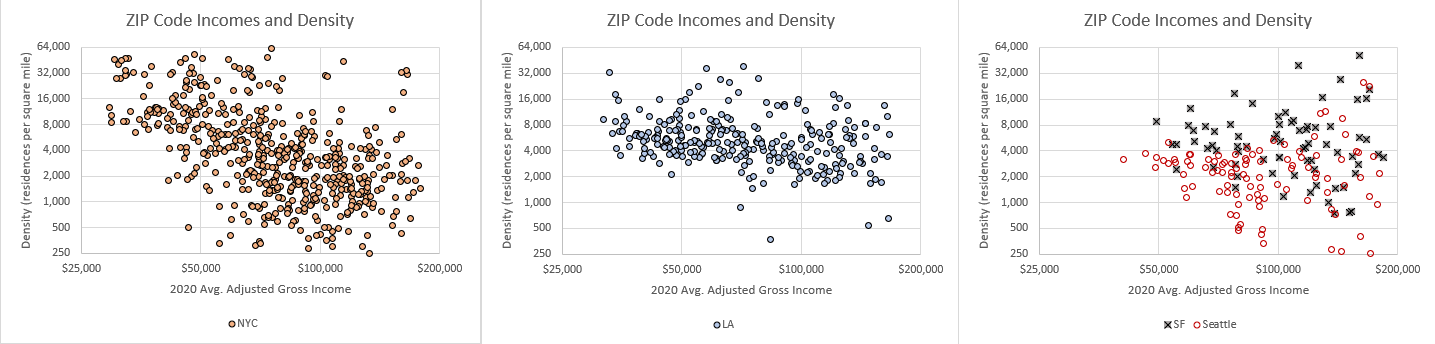

You can see this by looking at a handful of cities where density is probably most relevant. Figure 2 shows the distribution of households across New York City, Los Angeles, San Francisco, and Seattle, according to income and residential density.

There are 3 distinctive patterns. New York City, in the left panel, has areas that run the full gamut from not dense to very dense, and there is a relatively strong negative relationship between density and income. The poorest residents almost exclusively live in the densest ZIP codes.

Los Angeles has much less variance in density. There is actually still a negative association between density and incomes, but it is hard to pick out because there just isn’t that much diversity in density. The average poor ZIP code is more dense than the average rich ZIP code, but there is a lot of variance around the average relative to the range of densities across the metro area.

San Francisco and Seattle tend to have a pattern where average densities are not systematically correlated with incomes. But the poorest ZIP codes have moderate densities while richest ZIP codes can be very dense or very not dense.

Home prices tend to be higher in dense core areas in cities where the dense core has urban amenities like effective public transportation. But, the amenities generally have value for poorer residents. So, Price/Income ratios tend to be higher in dense ZIP codes, and it is the result of both higher prices and lower incomes in those ZIP codes.

In all cases, if inadequate supply causes prices in poor neighborhoods to rise the most, and causes migration into and out of some of those ZIP codes, then rising prices from an increase in demand for density can be hard to distinguish from rising prices due to inadequate supply. Are prices rising in dense neighborhoods because rich households are seeking density, because poor households are moving out of the metro area and thus out of the dense neighborhoods, or because poor households are staying in their neighborhoods but paying more because of inadequate supply across the metro area?

I don’t know if there is a dependable way to quantitatively measure these differences reliably. But, there are some qualitative ways to consider the data.

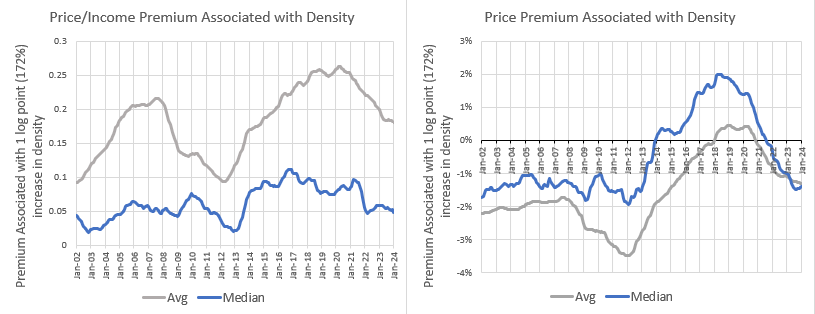

Figure 3 is an unweighted average of the 30 largest metro areas. The left panel is the price/income premium associated with more dense ZIP codes. (A coefficient of 0.1 means that a 172% increase in density is associated with a price/income ratio 0.1 points higher.) The right panel is the price premium associated with more dense ZIP codes. (A coefficient of 1% means that a 172% more dense ZIP code is associated with a price 1% higher.)

As the right panel shows, in the US, since our cities have been so bereft of amenity-providing density, density has actually been associated with lower prices. That is probably because in most cities, density is mostly associated with older neighborhoods with old apartments.

Notice that before 2008, the price premium for density was flat, and on the left panel, the price/income premium for density in the median metro area was flat, but the price/income premium for density in the average metro area increased.

That is because the entire rise in home prices in dense ZIP codes before 2008 was just a side effect of inadequate supply in a handful of metro areas. Costs in poor neighborhoods were going up in supply-deprived cities, and in those cities, poor households tended to live in more dense neighborhoods.

Keep in mind, this second order effect on prices is quite small in the broader scheme of things. Price/income ratios in poor neighborhoods in the most housing-deprived cities have risen to double digits. An additional 0.2 point increase that happens to have a spurious correlation with density is small compared to those other factors. That’s why I keep the tracker simple. Outside of some isolated spots, density just doesn’t amount to a lot quantitatively in US housing markets.

In the post-Covid period, prices and price/income ratios have been declining by both measures. This is likely associated with a decline in demand for dense neighborhoods associated with Covid and work-from-home. It doesn’t really matter if a city has density-related amenities. Covid created negative externalities with density, and work-from-home shifted value away from dense neighborhoods.

My concern here is with the effect this has on the Erdmann Housing Tracker. In most cities, I’m not sure that it matters much because they don’t have the sort of density that provides value to households with lower incomes. There isn’t much variation in density, and there isn’t much correlation between density and income. So, the recent devaluation of density doesn’t interact with the components of the tracker in most places. But, it does matter in a few places like New York City.

There are a few other cities that seem like they have the bones to create value from density - like Chicago or Philadelphia. Probably, in a different economic context they might require a similar analysis. Given enough demand, they would likely face some scale of supply constraints similar to those that are making other cities expensive. But, in their current economic condition, they aren’t reaping the problems of inelastic housing supply.

I will be getting into the tracker data a little bit, so the details are below the paywall for subscribers. The summary is that the flight from cities related to Covid doesn’t bias my supply affordability measure very much, except for in New York City. The recent flight from dense neighborhoods in New York City has reduced the cost pressures on poorer neighborhoods there. This shows up in my model as an improvement in supply conditions in New York City. Supply conditions are actually more likely worse than ever, but the Covid flight is providing temporary cost relief to dense poor neighborhoods.

There appears to have been some increased demand for dense neighborhoods in New York City in the years before Covid. That produced the opposite bias, making NYC supply conditions in the EHT appear somewhat worse than they were. Outside of New York City, controlling for density doesn’t generally matter that much.

Keep reading with a 7-day free trial

Subscribe to Erdmann Housing Tracker to keep reading this post and get 7 days of free access to the full post archives.