Mortgage affordability is a lot worse now than it was a couple years ago, and the difference between now and a couple years ago is largely the prevailing mortgage rate.

The sharp rise in rates did greatly slow down transaction volume in existing homes and temporarily caused a spike in cancellations on new homes where buyers didn’t have rates locked in and lost access to funding during construction.

However, EHT readers know that mortgage rates don’t have much of an effect on home prices. So, we have a trading advantage over housing bears who will keep expecting a crash for the indefinite future.

But, how can this be? How can such a rise in buyer costs have so little effect on the market for new homes?

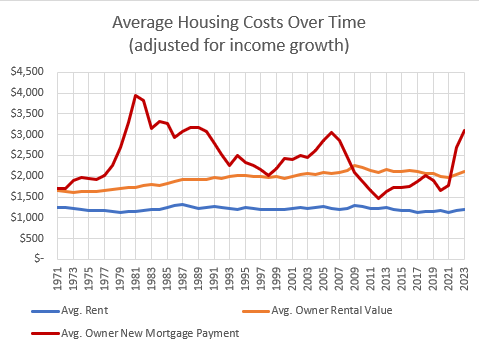

Figure 1 compares average rent for renters, average rental value of owner-occupied homes, and the mortgage payment required to buy the average owned home (based on 5% down and a 30 year mortgage). This sort of chart is a favorite among the permabear set because, really what you’re interested in is the difference between the orange and the red line. Like all nominal measures these rise over time. That means that the differences also increase over time. And, so you’re eyes are tricked into overestimating the recent divergence.

Adjusting for inflation doesn’t quite help because incomes rise over time, even after adjusting for inflation. So, in Figure 2, I have just deflated everything by the average nominal household income over time. In other words, in 2023, the average renter paid $1,204 per month. If the average income of the average renter in 1971 had been the same as the average income in 2023, the average renter would have paid $1,251 in 1971.(1)

In figure 2, mortgage payments are relatively high compared to rental value. On the low side of where they were in the 1980s, and about the same that they were in 2006.

Importantly, there is little stability in the measure. I can understand how one might intuit that it should be stable.

In most topics, we require more than intuition. Causal stories about interest rates do not. Intuition seems to be enough to repeat assertions on this topic.

So there is constant chatter about reversion to some mean in the red line in Figure 2, which clearly does not have a stable mean.

As I say, in a world full of astrologists, you don’t have to be an astronomer to gain an advantage. The neutrality of simple ignorance will give you an advantage.

Figure 3 is the ratio between the mortgage expense for a new buyer and the rental value on the average owned home, over time.

I am going to borrow some analysis from a previous post. In that post, I estimated the rental value of American homes that was related to structures and minimal land value, and the rental value related to inflated land value that comes from obstructed supply. In that post, I argued that American real estate values can be estimated over time with stable gross yields. There is one yield for structures, which is high because structures require maintenance and upgrading. There is a different yield for land, which is lower because it doesn’t require those expenses. The price multiple of land is about 3 times the price multiple for structures, on average.

There are 3 deviations from these yields:

Inflation, which increases yields in nominal dollar terms (and increases mortgage rates).

Cyclical changes, which are minor changes in yields that tend to even out over time.

The one-time credit shock in 2008 that lowered price/rent ratios permanently.

Regarding inflation, the mortgage affordability measure that we typically see, and which I am using here, is the mortgage payment at the point of purchase. But, in a highly inflationary environment, rents will soon overtake mortgage payments. The mortgage affordability measure has an inherent bias that doesn’t reflect the lifetime cost of ownership.

That doesn’t mean it’s a totally worthless measure, but it must be used with care, and we certainly shouldn’t expect it to have a stable mean.

There is a tendency among financial professionals and certain schools of economists to be, frankly, a bit misanthropic. Their mental model of financial markets is that buyers are undisciplined lemmings who will take on the largest mortgage they can get approved for, to their own demise. (The popularity of this attribution error is all over the mythologies that drove the Great Recession.) So, they think that either tightening debt to income limits, shortening amortization schedules, or raising interest rates has a mechanical effect on home prices because the lemmings will have to adjust their purchase size to the new maximum mortgage amount.

That is why the mortgage affordability measure seems important. With that mental model, the lifetime cost of ownership doesn’t matter. Demand is limited by the initial cash outflow buyers are allowed to get.

The effect of initial cash outflows isn’t non-existent, but it’s not nearly as important as it is given credit. With so much institutional buying and all-cash buying, it may be less important than ever. And, we can intuit the scale of the importance by looking at what happened to housing markets when rates spiked in 2022. Probably the most significant change was that the average size of new homes declined a bit.

Rent for structures vs Rent for inflated land

Anyway, I digress. To get to the bottom of the mortgage vs. rent issue, we need to understand what rent is paying for.

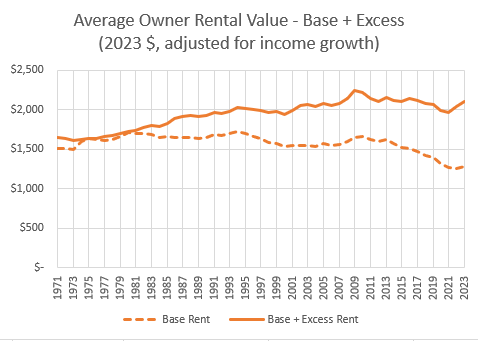

Using the model from the earlier post, Figure 4 estimates how much of the average rental value of owned homes has been due to structural value vs. inflated land value over time. In 2023, $1,285 of the average owner-occupied rental value was for structures and $822 was inflated land value.

Between the 1980s and the 2000s, the rise in rents was all due to inflated land value. (Think of rents on homes built before the 1970s in LA and San Francisco.) Since the Great Recession, new home construction has been very low. The housing stock has been stagnant while incomes grew.

The average rental value remained relatively level during the 2010s, but clearly, that has been a combination of a depreciating stock and increased land inflation. It takes residential investment to increase the total rental value of structures, and since 2008 residential investment has frequently not even kept up with depreciation of existing units.

The rest of my analysis is below the paywall.

Keep reading with a 7-day free trial

Subscribe to Erdmann Housing Tracker to keep reading this post and get 7 days of free access to the full post archives.