January 2024 Residential Construction and New Home Sales

In this month’s update, I want to start out with a discussion of home prices and home sizes.

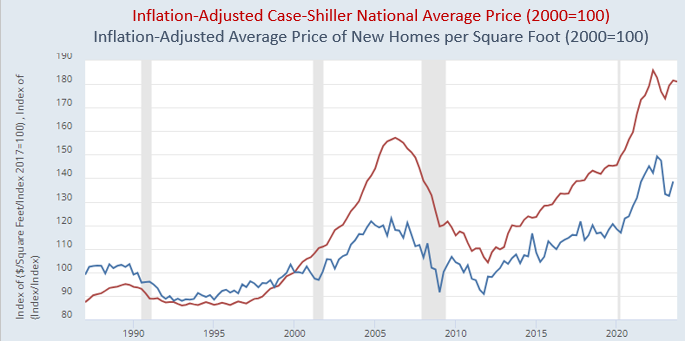

First, Figure 1 is a comparison of the average price of new homes and the price of existing homes, as tracked by Case-Shiller. There are several reasons for these measures to diverge. If you can’t build many houses in Los Angeles, then existing homes in LA get more expensive and new homes in Albuquerque stay the same, even if there are a few more of them.

Political opposition to housing increases the prices of older homes more than new homes. The divergence in these measures since the late-1990s is a signal of obstructed supply.

Another reason for a divergence is a change in the composition of new homes. The stock of existing homes, of course, changes little from year. But, changing market conditions can more quickly change the types of homes that are built and sold. And, over the long-term, as household income rises, new homes have tended to be nicer and larger over time.

As Figure 2 shows, the sharp rise in mortgage rates in 2022 was associated with a decline in the average size of new homes started. Those homes are just now flowing through to completions, and the average size of completed homes will soon follow.

There have been other shocks and down-shifts in home size (going back to the mid-1980s where the quarterly Census data begins). Neither of those were associated with rising interest rates. The sharp downshift in new home size in 2008 was associated with the deep cut in incomes in 2008, while mortgage rates were declining. The downshift in new home size after 2014 happened while mortgage rates were low and steady.

In Figure 3, I again compare the Case-Shiller home price index with the price of new homes. But, here, I adjust for the changing size of new homes. If new homes are getting larger, then their price trend will be overstated and if they are getting smaller, their price trend will be understated.

Making this adjustment causes the measures to diverge even more. This actually improves the information here. The diversion is real. Again, this is because when LA doesn’t build enough new units, prices on old homes in poorer neighborhoods in LA rise more than new and newer homes do. And, more new homes are built in other regions where home prices are lower.

In Figure 4, I tweak the adjustments a little more. Here home prices are adjusted for rent inflation, rather than general inflation, and like in Figure 3, I adjust new homes for size. Since the CPI rent measure has had a known lag issue since 2021, most of the spike in these measures after 2020 is a short-term data bias. The dotted lines are a simple correction to that lag.

Figure 4 further clarifies the difference between new homes and existing homes. The price of new homes has basically tracked with aggregate rent inflation. It is existing homes where price/rent ratios are much more volatile and have an upward tilt over time.

Finally, in Figure 5, I adjust both measures for the cost of construction (using the BEA’s residential investment price level measure). Again, there is divergence between new and existing homes. Existing homes have risen in value relative to the cost of construction. This suggests that costs aren’t an important factor in rising home prices, because the cost of their construction was determined years or decades ago. Of course, my research clarifies why this is the case. (Filtering - “trickle down”, as it were - is the source of affordable housing and the lack of adequate new supply reverses that filtering.)

In contrast to existing homes, the price of new homes over a period of decades is, to a first approximation, a matter of the cost of construction. Rising rents and rising cost of construction are likely causes of the declining size of new homes since 2014. It seems that rising costs changed the composition of new homes, but the number of units continued to increase.

The existing stock of housing is inflated an additional 25% beyond the cost of construction. The cost of existing homes is not tethered to construction costs.

A couple takeaways:

Many of the reforms that would allow more new homes to be built would also lower costs - faster permitting, lower land costs, etc. - but the main benefit of reforms would be to lower the price of existing homes. Additional reductions to costs would be secondary to that primary effect.

Much of the decline in recent new home prices has been compositional - buyers are choosing smaller homes to counter rising building and borrowing costs. On a real square foot basis, there just isn’t a lot of variance in the prices of new homes. There has been some pullback in the nominal average price of new homes. Some of that has been from a switch to smaller homes, and some of it has been from a reversion of above average costs and builder profit margins back to the norm. Those each accounted for several percentage points of decline. The decline in new home prices is not some boom-bust cycle unrelated to fundamentals. There isn’t some other shoe waiting to drop that’s going to pull down new home prices even further.

By the way, these trends are sort of another way to look at the point I make with the Erdmann Housing Tracker numbers…

This month’s data and more discussion below the paywall.

Keep reading with a 7-day free trial

Subscribe to Erdmann Housing Tracker to keep reading this post and get 7 days of free access to the full post archives.