Responses to My Plea for Looser Lending: Salim Furth

Earlier, I reviewed Dean Baker’s response to my Washington Post op-ed. The long and short of it:

In the op-ed, I argued that overly tight lending since 2008 has caused rents to rise significantly and is the main cause of post-2008 housing affordability struggles. I used Atlanta as an example of a city that didn’t really have a building boom or a price bubble during the subprime lending boom from 2003-2007. Yet, tightened lending caused prices and construction to collapse in Atlanta, to an extreme, especially in working class neighborhoods that especially depended on reasonably generous lending.

Baker’s post is titled “There Was a Housing Bubble in Atlanta Prior to the Crash”.

I appreciate that Baker took the time to comment on the op-ed, but, it’s disappointing that a generation-defining catastrophe is still being dismissed with a wave of the hand more than a decade later. I just don’t think Baker is engaging thoroughly with the facts. His response did, however, give me the chance to add some details to the op-ed for clarification for readers willing to engage.

On the other hand, Salim Furth has a post up at Market Urbanism, titled, “Toward an Erdmann Synthesis” that makes some productive points. He also brought in details from the recent Conor Dougherty New York Times piece on Kalamazoo, and my reactions to that. As far as I know, Dougherty hasn’t seen my posts on Kalamazoo. I was pretty hard on him, too. (I don’t know. Am I too cantankerous?) Maybe there isn’t much for him to say. Honestly, the more I think of it, the more that I am baffled trying to understand how the world would even work if we followed the main thrust of his article - that upper-middle income residents of the rust belt should be getting rent subsidies.

My point, which dovetails with my Washington Post piece, is that if we allow those families to get mortgages, we won’t need to subsidize the more expensive rent payments that we do allow them to take on. Dougherty’s solution basically suffers from the hand-waving consensus characterized by Baker. The mortgage moral panic and its aftermath created some crazy, unprecedented, extreme outcomes, and if your Overton Window doesn’t point in the direction of the mortgage crackdown, then the world is going to be confusing. You’ll be benchmarking to ruin and blind to the only path out of it.

Since functional, generous mortgage access made us house-richer, as a society, the removal of functional, generous mortgage access made those who can’t get mortgages house-poorer. Those families in Michigan with six-figure incomes who can’t qualify for mortgages don’t need rent subsidies. They just need to get used to their kids sharing a bedroom like their house-poorer parents’ generation did. Selective generational devolution seems confusing and unfair, so it seems worthy of subsidy. It is unfair.

The mortgage crackdown is responsible for this newly inequitable housing market. If we aren’t going to reverse that, then subsidizing renters is just going to prolong the adjustment. There is no human right to having a 2,000 square foot house instead of a 1,500 square foot house. I doubt that a coherent public budget could be created to even try to comprehensively accomplish such a thing.

Furth’s Comments

The basics of my claims are that rent is the important measure of housing affordability. Cutting off mortgages lowered prices too far, cratered housing construction, and caused rents to rise. An analogy I like to use is that the mortgage crackdown in 2008 was like trying to make bread cheaper by cracking down on the purchase of farmland.

Furth accepts my framing, at least for the sake of the discussion. He writes:

Although I’ve been Erdmann’s colleague for most of this time, I’ve maintained wide priors on the question of credit standards. Many other scholars, left and right, are skeptical of the broad, century-long trend of encouraging (and subsidizing) homeownership….

…This doesn’t tell us whether subsidies are good or not. It wouldn’t exactly be a surprise if a milk subsidy made milk cheaper, right? Housing markets are weirder than milk markets, but it’s still not that weird to think that housing subsidies make housing cheaper.

Quibbles and Clarifications

Subsidies vs. Permission

Furth framed federal mortgage support systems as a question of the effects of subsidies. I think we need to be careful about defining what has happened, because it is important to the sense of scale. In “Building from the Ground Up”, I estimated that as of 2019, federal tax subsidies for homeowners totaled about $288 billion. The mortgage tax credit is usually what people talk about. But landlords have to pay taxes on their rent income while owners don’t, and that’s the largest part of the $288 billion. That year, property taxes amounted to about $264 billion.

Property taxes are relatively flat across incomes, even regressive in some jurisdictions. Tax benefits tend to be regressive, if only because taxes paid are generally progressive. So, I would argue that housing isn’t particularly subsidized or taxed. It’s pretty neutral. And, to the extent that it is subsidized, it is mostly the richest homeowners in the most expensive homes that are subsidized. Subsidies are not, and probably have never been, important for the marginal home with a buyer that may or may not qualify for a mortgage under a tightly regulated regime.

Before the 2008 debacle, Fannie and Freddie arguably created lower interest rates for their borrowers of about 0.25%. That amounts to about $13 billion annually. It’s a drop in the bucket. It is unlikely to be mathematically important to the $3 trillion annual rental value or nearly $50 trillion market value of owned homes.

One could argue that they are a subsidy beyond the basic dollar savings because they create markets for marginal borrowers.

To that I would say that:

That isn’t a subsidy. It’s a public service. It’s modernity. Like having a stock market or roads or electrical utilities.

That probably made a big difference 60 years ago, but the financial economy is much more sophisticated today. And, in the runup to 2008, the GSEs and FHA lost a ton of market share. Whatever you think of the private securitization boom, it is hard to argue that the marginal pre-2008 homebuyer required federal mortgage subsidies. There is a lot of motivated reasoning on the right against the GSEs, and a lot has been written trying to pin the pre-2008 mortgage boom on them. One thing some people have tried to argue is a sort of “I learned it by watching you” argument that the GSEs paved the way for the recklessness of the private markets. The Olympics was great. My capacity for viewing gymnastics has been sated until 2028.

The post-2008 market can most accurately be described as a market where millions of potential borrowers with anything less than pristine credit are simply banned. The QM patch, which relieves mortgage originators of regulatory threats if the federal agencies accept their mortgages, allows the federal agencies to earn monopoly profits on the mortgages that are originated. They are originating mortgages with negligible default risk and raking in fees for the federal government.

This is why millions of households across the country are renting homes they could buy with mortgages that would be much cheaper than the rent they are paying. The supply of mortgages is being throttled. Those households are the deadweight loss.

The subsidy or monopoly profit the GSEs might be affecting is trivial compared to the loss from the borrowers that have been banned. If a family is renting a home for $2,000 that they could buy with a mortgage payment of $1,500, that difference is a window onto the massive deadweight loss we have imposed on families. In the end, the deadweight loss is expressed as rent inflation. (And, I’m using shorthand here on the relative payments, but on most homes, the equilibrium in a market without capital constraints would settle at mortgage payments higher than rental payments. Just check your own house, if you’re a homeowner, at Zillow. It is highly likely that the mortgage payment a new leveraged buyer would need is higher than the rental value of your home…. Hey! I have an idea! If that’s the case, we should make it illegal for you to get a mortgage until homes in your neighborhood are cheap enough to bring down those mortgage payments! Affordability! Where’s my Economics Nobel?)

The scale of any subsidies associated with mortgage rates is miniscule compared to the cost of denial. The interest rate on a denied mortgage is ∞%. So, the cost of denied access is unbounded. How does denial compare to rate subsidies? What is ∞/0.25%? The cost of denial to households depends on the alternatives available to them. (To put this in analogous terms, if we made zucchini illegal, zucchini would have an infinite cost, but households would buy squash instead. So, the practical cost of banning zucchini would be determined by the cost of squash.)

The practical cost of the mortgage crackdown might not have needed to be that high. If new apartments were also broadly permitted, it might be that rents would not have to be that much higher to trigger new construction again. But, since apartments are commonly blocked, rents have continued to rise until it has started to trigger the construction of single-family homes built to rent.

As I have written about elsewhere, there is a movement to ban large scale landlords from buying single-family homes. That would be it. That would be the last alternative. If we ban that, then rent inflation might become truly unbounded. It will only be moderated by the continued intensive decline in the housing conditions of renters. Much of that moderation has taken the form of homelessness, and I would expect that to continue if we ban large scale single-family rental homes. We probably will, either nationally or in selected locations.

I have never really missed a payment on anything in my life. I have been making mortgage payments on the home I live in for more than 20 years. I even refinanced a couple times. There was a brief period a few years ago where I was able to check off all the boxes to meet all the new “Ability to Repay” mandates, and I refinanced again. And I will make all those payments until the mortgage is paid off. For 90% of the time since 2008, I wouldn’t have even filled out the application forms because the bankers made it clear there was no way I was getting approved for anything.

There are millions of us who own homes and are in that position. Whatever subsidies there ever were for housing, on net, were much smaller than the current deadweight loss from the lack of mortgage access, which covers private lending channels as well as public.

One way to estimate the deadweight loss is the value of the real estate Americans aren’t consuming. Relative to pre-2008 trends, that is nearing $1 trillion annually.

From World War II to 1970, federal mortgage programs increased homeownership substantially relative to the status quo with an undeveloped financial sector. They were important. That period was associated with high levels of residential investment but it wasn’t associated with high home prices or increased nominal spending on housing, and it was associated with declining real rents.

One could say that, still, in 2007, federal tax benefits were a net subsidy for homeowners. They increased both supply and demand in housing in high tier markets that value tax benefits. But, did the marginal homeowner with below-median income in 2007 pay any income taxes? Would they have owed taxes if they were taxed on the rental value of their homes? Maybe a little. Probably not much. Did access through federal mortgage agencies increase homeownership? Private securitization pools had been taking market share from the FHA for a decade by 2003 and then from 2003 to 2007 they were taking market share from the FHA and Fannie and Freddie. By the 2000s, it doesn’t seem like marginal new home buying activity was dependent on federal mortgage programs.

Was there a time when the marginal American mortgage borrower could be characterized as being subsidized, on net? Yes. To the extent that was still true in 2007, it has been reversed many times over. Now we block reasonable borrowers and route the remaining borrowers through the national mortgage agencies and charge them elevated fees.

How much has supply been cut?

The lack of construction since 2008 isn’t in question, but what about the mechanism?

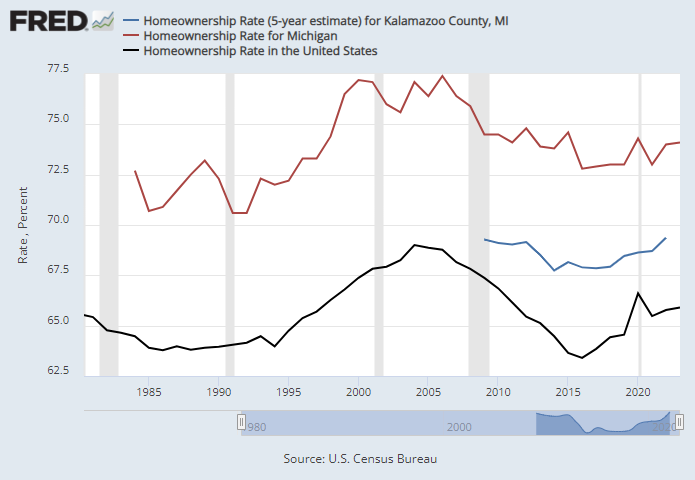

The mechanism through which I assert that supply has been cut off is through the decline in owner-occupier purchases, so Furth rightly looks at homeownership rates for clues about the scale of the change. In Figure 2, I show the homeownership rate for Kalamazoo County, which only stems from 2009, for the state of Michigan, which goes back further, and for the US.

This is a bit tricky. There are 3 margins on which the published homeownership rate for Kalamazoo County needs to be adjusted to account for the change relative to the counterfactual.

Homeownership peaked in 2004. Construction started to decline sharply by early 2006. The private securitization market was collapsing by early 2007. The extreme tightening of lending into the prime space started around the end of 2007. So, the Kalamazoo measure doesn’t quite go back far enough. Let’s say that, in total, homeownership was down 2% in Kalamazoo from 2007 to 2019. For the state of Michigan and the US, it’s a bit more than 3%.

An aging population creates an upward slope in the homeownership trend. Working age homeownership was about the same in the US in 2004 as it had been in the early 1980s. All of the rise in the aggregate number was because older age groups tend to be homeowners. And much of the rise that remained after adjusting for demographics was was from rising homeownership among retirement age Americans.

In a counterfactual with a stable credit environment, demographics would have pushed homeownership up about 2% more since 2007.

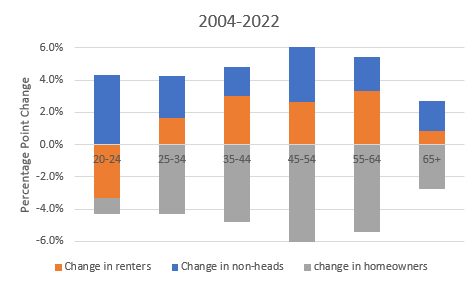

Figure 3 As the housing supply condition has worsened and spread, it has started to affect headship rates. On net, from about 2005 to 2015, the mortgage crackdown turned a lot of homeowners into renters. But since then, the shift has been mostly from renters to roommates. When a 30 year-old is is still living in their parents’ basement, they have neither bought a house nor formed a household, so they do not change the homeownership rate. Headship rates have declined in all age groups. And, for each point decline in the homeownership rate, there is about one additional American who has not formed a household. So, that’s another 2% or so of buyers missing from the housing stock associated with fewer homebuying households.

One broad way to estimate the total drop in homeownership compared to the counterfactual is to compare demographically constant homeowners/capita in 2019 (33.6%) to 2007 (37.2%), shown in the right panel of Figure 3. That’s a drop of about 10%, which corresponds to a decline of homebuyer demand of about 7% of the US stock of homes.

These are broad statistics with a lot of noise, but the one good thing you can say about generation defining catastrophes is that rough numbers are good enough to see what’s happening.

The reason I’m using 2019, by the way, is that homebuilding has been stuck in supply chain constraints since Covid appeared. Without those constraints, many more homes would have been constructed. But I think they would largely be rentals if they had been. Supply has been practically constrained since 2020, but if it had not been, supply would have started to expand even with the loss of owner-occupiers because rents had risen enough to trigger the alternative. (More on that below.) So, I used 2007-2019 as the important time period here.

Figure 5 compares the number of homes permitted in Kalamazoo from 1996 to 2007 to the number built from 2008 to 2019, as a percentage of the stock of homes. It grew by about 16% before the crackdown and about 6% after. Proportionately, the US numbers aren’t particularly different. Most of that difference can be accounted for by the 7% of homeowners that are missing relative to the counterfactual.

Build-to Rent Single-Family Homes

One prediction that I make, which I hope the reader will consider a corroboration of my claims here when it turns out to be right, is that most of the marginal rise in housing construction moving forward will be large scale single-family rentals. They have never been a significant market segment in US housing, for good reason. Funded households naturally have always outbid institutional landlords for single-family homes. This is a really weird market that shouldn’t exist. And most recent marginal growth in housing supply has been rentals, and will continue to be rentals.

Detroit is reportedly one of the cities where it is taking off. The only reason it is suddenly becoming a huge market is that we have artificially prevented families from being owners.

Every time you see a report about this surprising new build-to-rent market, and every time you see people marching and yelling that to make housing affordable again we need to ban Wall Street landlords, save a few neurons to remember that that cantankerous old Erdmann Housing Tracker dude predicted this. Come track me down, and we can drink ourselves into a stupor watching the pitchfork wielding mob self-immolate.

Anyway, the cost of a denied mortgage is infinite, but it appears that the alternative of renting is becoming feasible after a permanent rise of about 25% in the average rent and about 40% for the poorest renters.

On that issue, Furth makes an interesting point. He writes:

We can add: rental subsidies don’t boost construction much because they’re targeted to people who aren’t close to being able to afford new construction and/or because zoning limits the land available for multifamily construction.

Since a lack of housing supply systematically creates regressive rent inflation, there is an interesting issue here. And, maybe, Michigan’s rent subsidies aren’t as bad as I first thought. The upper-middle income families getting subsidies in Dougherty’s article would have been buyers in the late 20th century. And, it appears that, nationally, as I wrote above, the missing homes that they would have bought might be associated with excess rent inflation of 20% or so on those same homes. Now builders are getting interested in building them.

Poorer families that have seen 40% excess inflation are living in 60 year-old poorly maintained apartment buildings that are not particularly influential to the new housing market. Maybe it is the case that giving the upper-middle income families a 20% rent subsidy will cause the houses that would have been built to be built again, and, as a result the 40% excess rent inflation on those old apartments will also go away. Those old apartments aren’t particularly connected to the new-build market, but they are definitely affected by the newly-unfunded households who are crowding into the higher tiers of the rental market. Maybe the total result of those subsidies won’t really be regressive because they will solve the housing supply problem, and the housing supply problem is much more regressive than upward flowing rent subsidies are.

It’s still a waste of public funds, but maybe the outcome would be better than I presupposed.

Not-So-Superstars

One last quibble for Furth. He writes, “His (my) other core point, that ‘closed access’ superstar cities have made it too hard to build, is clearly correct.” I won’t be too hard on Salim here, because even in “Shut Out” I was framing the issue that way. But, I have become allergic to the “superstar” designation. Some of the exceedingly expensive cities may be superstars. San Francisco is the most obvious example. But, being superstars isn’t why they are expensive. They are expensive because they have been extreme outliers in blocking housing growth.

The “closed access” cities have been collectively losing population since before Covid. Some of them might have avoided being extremely expensive with even just 1% annual population growth over the past couple of decades. Maybe the most super of them would have needed to grow more like 3-4% annually, like Austin. They aren’t growing. They are shrinking.

And, what the mortgage crackdown has proven is that every city, super or not super, is capable of accumulating regressive rent inflation with “closed access” levels of new housing production. “Superstarness” is neither necessary nor sufficient to become excessively expensive. See Austin. Blocking new housing is both necessary and sufficient.

There is nothing wrong with the literature on agglomeration economies and the value of cities. It just has little to do with our current predicament.

Or, maybe Kalamazoo became an international hot spot while we weren’t looking. Why didn’t Dougherty consider that possibility? Maybe instead of regressive rent subsidies, the newly super Kalamazoo should ban Arab sheiks and Chinese billionaires from buying fancy pied-a-terre in downtown condo buildings.

There is one proper diagnosis (a lack of supply, whether through blocked permits or blocked funding) why housing in the US has become expensive and a hundred misdiagnoses. As Furth noted in his post, Kalamazoo helps clarify the issue because it makes many of those misdiagnoses obvious. But, as Dougherty’s piece makes clear (to my reading) we aren’t going to get to the correct diagnosis through a process of elimination of the misdiagnoses. There will always be more. Eventually, the elephant in the room will drop enough dung to make its presence undeniable. I intend to smear it in some faces as long as that process of awareness needs helped along. Or, as in the case of banning Wall Street landlords, maybe we will eventually just collectively insist on being buried in it.

Kevin,

Insufficient housing supply is the issue. Low supply means housing costs too much and it means the housing market fails to clear. The lack of clearing creates bottlenecks similar to gridlock on a city street. But why is there insufficient housing supply? It is because of government regulations.

Where I live in Maryland, restrictions and regulations on new construction mean new SFH construction is only economical if it has a price level in excess of $1.2 million. New town home construction sells for $700k. New condos sell for $500k. There is a huge increase in construction cost as the housing density is decreased. Given there is plenty of land what explains this? It is artificial constraints imposed by local and state governments. Three of the biggest regulatory costs are (1) Impact fees (2) Fire suppression (3) Septic. Combined, these add several hundred thousands of dollars to the price of a SFH. Recognize that Fire suppression and stricter septic regulations are new requirements added in the past dozen years. Escalating impact fees are also a recent development.

These issues are not just blue state blues. I have a friend in Tennessee who bought land several years ago with the intent to build a house. This new house remains unbuilt due to the the difficulty in hiring a builder to do the work at a reasonable price. Because my friend cannot build a new house, he is living in a small house that would otherwise be a starter home for someone else. This is the gridlock that happens because governments have made new home construction so expensive and difficult.

Up until 20 years ago, new home construction in growth areas of the country was a constant activity. This meant there were plenty of skilled suppliers / contractors and there was a diverse market of homes always on the market. People could buy new low cost homes and then in a few years move up to a more expensive home, allowing the previous home to add to the supply of homes available to new buyers.

The GFC killed this economic model and I think you are correct that financial regulations are a factor. I believe the greater issue now is over-regulation of home construction. Suppliers and contractors cannot commit high capital to building single family homes because the time and costs to permit new lots, homes and infrastructure is too high.

This was jam packed dense. I won't take issue with any of it. I will ask a question on motivations and zoning. Let's posit that all buyers want their purchase to appreciate, at least to keep up with inflation and possibly more, Say "Rate of inflation + 6%". Normal housing would expect "Rate of Inflation, only". So to get that extra 6% (making housing an "investment" equal to a long term stock index) you need to either stimulate demand, or throttle supply. The normal situation in growing cities is to do both. They stimulate demand by attracting industry, and they throttle supply by saying "no" to increased density. That pushes prices up, and pushing prices up drags rents up, pricing the lower income half of the population out of the purchase market, and very possibly out of the rental market as well. So no matter what the interest rate is, or the mortgage qualifying standards are, most purchases become cash buyers. [ And current homeowners want to keep it this way to keep their invest type returns.] To some extent Freddie and Fanny are just on the sidelines for this. They were severely (self) wounded in GFC, and are still over cautious. But isn't the real story here the Demand for mortgage backed securities in the secondary market? And isn't that demand low?

Now, one suggestion. How about a lending standard change that says two years of rental housing payments in good standing, qualifies a buyer for a mortgage with a PI of 90% of the rental payments?