In this post I am going to revisit a factoid from the financial crisis that is one of the many points at odds with conventional wisdom. And, it ties in to my counterintuitive points about mortgage access and housing affordability.

To recap:

There was a subprime/Alt. A credit boom from 2004 to early 2007. However, the credit boom was not a particularly important factor driving home prices higher, and it also was not associated with an expansion of homeownership to families with low incomes and bad credit.

There was a deep, regulatory retraction of prime mortgage credit after 2007, unrelated to the earlier boom (except that myths about that boom were the motivation for enforcing it). That credit bust was responsible for a deep collapse in home prices and construction and for most of the damage of the crisis.

Distressed Debt

My broad description of what was happening before 2007 is that the urban housing shortage was making homes more expensive in the housing-constrained regions. Those regions are populated by (1) existing homeowners who are house-rich, (2) new households that are financially distressed, whether they are renters or homebuyers, and (3) existing renters who are forced to move away by the tens of thousands each year. In those regions, the new mortgages were helping households with high incomes remain in those cities. In most of the rest of the country, homeownership and home prices were not particularly unusual and so those mortgages weren’t associated with much of a change in buyer behavior.

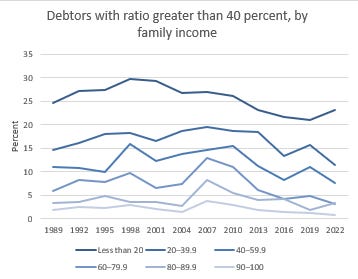

The long-and-short of it is that, the subprime mortgage boom was associated with declining debt payments for the poorest American households, level debt payments for average American households, and sharply rising debt payments for the richest American households. (In “Shut Out” I discussed evidence that the earliest declines in homeownership in the bust were among the richest households. Homeownership among average households didn’t decline until after the recession. The crisis was not caused by mortgages to poor families that got in over their heads.)

In Figure 1, you can see that the spike in high debt payments in 2007 is limited to the richest families. The prevalence of high debt-to-income ratios have generally declined since 2007. This is for a sample of all households from the Survey of Consumer Finance. Average debt-to-income (DTI) for all households follows a similar trend.

Who Has High Debt Payments?

In numbers tracked by AEI, however, DTIs in all the agency conduits have been rising since 2013.

The same pattern shows up in a longer timeframe tracked by the Urban Institute, in Figure 3. There was a rise in DTIs before the Great Recession, which coincides with the rising distressed debt levels of the richest households in Figure 1. Then, average DTIs declined until about 2013 and bumped up a bit in 2019. This is similar to the SCF data above, but the SCF data has a general downward trend and this doesn’t. And, in both the Urban Institute and AEI data, DTI is basically at all time highs while debt levels in the SCF have continued to trend down.

So, what’s going on? The difference is that the DTI’s from the SCF are for all families and the DTIs reported by AEI and the Urban Institute are for new mortgage borrowers at the point of purchase.

This relates back to my previous post. You have to be careful with mortgage affordability measures because, in nominal terms, a fixed rate mortgage stays the same over its life. Rents increase with inflation. That means that in real terms, mortgage payments decline over time while rent payments stay the same.

Comparing the mortgage payment of a new borrower with the rent payment of a renter is not apples-to-apples.

So, basically, the AEI and Urban Institute numbers reflect the fact that homes are very expensive, and our front-loaded fixed rate mortgage products make the initial payment on expensive housing very high. That makes it hard to buy.

So, the reason that SCF data shows a decline is that, even though homebuyers are taking on higher initial DTIs today, there are fewer of them than there used to be.

In Figure 4, I show SCF data for average DTIs for all households, by age.

This highlights a couple points. First, you can see here that the initial DTI is only relevant for a short time. Households, systematically, pay down their debts after their first home purchase. On any given year, the debt held by older cohorts is much lower than the debt held by younger cohorts.

As I mentioned in the previous post, conservative (with a small c) analysts and policymakers tend to have a misanthropic view here. The high initial payment makes the fixed-rate mortgage popular among some pundits and policymakers. Longer-duration mortgages and floating rate mortgages are likewise unpopular because they can be used to lower the initial payment. (You tend to see cynical reports of some country or agency introducing a longer-duration mortgage product, as if this will just increase the loan size households will take out, and also the prices of homes.) The high starting payment of fixed rate mortgages forces first-time homebuyers to purchase a smaller house, and this is thought (wrongly) to keep home prices moderate by limiting demand through credit constraints.

What it actually does is pushes first time homebuyers to take on more financial risk to get into the house they prefer.

The myths and misanthropy associated with the Great Recession probably make that sound naive. Of course, we’ve all been primed to think, homes are only expensive because entitled young couples with overly generous lenders bid them up like proverbial avocado toast. I would hope that any YIMBY who has put any reasonable amount of thought into the implications of a housing shortage can come around to how ridiculous the logic is there, and thus how downright toxic these popular stories have been. Deeply toxic and damaging.

It will be a hopeful day in America when the Greater Fools who have been using their authoritative pulpits to push the “Greater Fools” theory of home prices take a cold shower and then a quiet seat in the back row to watch the young generations dig out of the mess they were given.

Now that I think about it, the notion that home prices get bid up so high because young borrowers don’t have any sense and regularly overextend themselves is the same sort of rhetorical trick as claiming that your city has a homelessness problem because there are so many drug addicts and mentally ill people, and they just flock to your city because they love it so much.

There’s no shortage of housing! Everyone is just making bad choices! And they make those bad choices in our city in particular because our city is so awesome and everyone wants to be here!

The high payment is only temporary risk, because the debts will tend to decline relative to their incomes over time. So, really, these mortgages just focus more risk at a certain vulnerable portion of our financial lives.

Anyway, lending standards tightened in 2008, and notice in Figure 4, what has happened since then. Debt payments have declined for younger families and increased for older families. We have delayed when families take on mortgage debt, and so that debt is lasting later into their lives.

It might look like, at least, this change has lowered DTIs on average, but it appears to me that the lower average is largely due to lower homeownership. Because, again, the Urban Institute and AEI data shows that new homebuyers have higher DTIs than they ever had.

All the mortgage tightening didn’t due a thing to make the finances safer. It just blocked families from homeownership.

Consider the wretched irony that some pundits react to these ever higher DTIs by calling for even more tightening of lending standards. If we just keep making it illegal for more people to build, or buy, or finance houses, surely, they will eventually become affordable!

Why has tight lending pushed up debt payments?

Last September, I walked through lifetime mortgage payments and rent payments in a couple posts using charts like Figure 5 and 6.

First, it wouldn’t necessarily have done so. If we had paired tightened lending standards with radical upzoning and urban land use deregulation, then single family homes might have been replaced with multi-family infill, and maybe rents wouldn’t have gone up so much. It’s not quite that simple, but obviously if we had built 600,000 or more multi-family units a year for the past decade instead of 300,000, the unprecedented rent inflation of the past several years would have been more moderate.

But, we didn’t, so rents have risen substantially while mortgages were suppressed and construction was low. As I discussed in the previous post, rent inflation is land inflation, and inflated land carries a high price.

The prices of low tier homes in most cities now fetch a higher price/income ratio than they did at the peak before 2008. My working theory on that is that those are typically older neighborhoods that are typically depreciated with some negative amenities, but well located. The metro-area wide shortage(1) of homes has increased excess land value across each city. So, replacement value (where a stable cost of construction should anchor marginal home values) is now higher because a higher land value is bundled with the average home.

In any case, the lack of construction has increased rents and rent inflation. Figure 5 shows a simple comparison of mortgage and rent payments over time with 2% expected rent growth.

Figure 6 shows a simple comparison of mortgage and rent payments with 3% expected rent growth.

In a supply constrained market, higher rent inflation will increase the cost of a home in the later years, but it increases the cost of a mortgage in the early years.

Tight lending is the reason DTIs are so high.

(1) Economists are touchy about using the word “shortage”. It has a specific meaning in supply and demand economics that doesn’t just mean “I wish we had more of this.” I respect that.

I have used it since early on in my housing writing, and the reason is that housing markets have many elements of a true shortage - queueing (either developers at the planning department, wait lists for subsidized units, or homeless encampments), price controls, quantity controls, even explicit objections to new supply because the price is too high. If the term “shortage” doesn’t apply to American housing, then the word is so pedantically limited as to be meaningless, so I have increasingly used the word without caring much about how careful I am.

Kevin, I do not dispute your argument of a housing shortage. However, in addition to the factors limiting supply there is another contribution. This is that the demand for second homes has greatly increased. The trend peaked in the pandemic years. Lately there has been a softening.

If boom and bust economics play out we may see housing becoming especially more affordable in the next few years. Some second home owners who joined the multiple home ownership club during the pandemic / short-term rental business frenzy will sell. Others will be pressed to sell due to financial stress. And builders who ramped up construction in 2023 and 2024 to meet demand may discover a buyer's market and respond with more buyer incentives.