Home construction leading the almost recession recovery

I’m going to go out on a limb here, and I’m posting this just before Hovnanian gives us a taste of home sale trends through January with their 1st quarter 2026 earnings report today, so that I might have to eat my hat before the ink is dry on this post. I think we’re going to start to see new home sales finally start to increase, in earnest.

I previously wrote a series of posts about the new business cycle. My thesis is that Ed Leamer’s point about housing and the business cycle was right. Construction employment is an important leading indicator. And, now that we are deep into a ridiculous shortage of homes, it will be very difficult or impossible to create a policy context - either monetary or fiscal - that is recessionary enough to lower construction employment significantly. It will be very hard to have a recession.

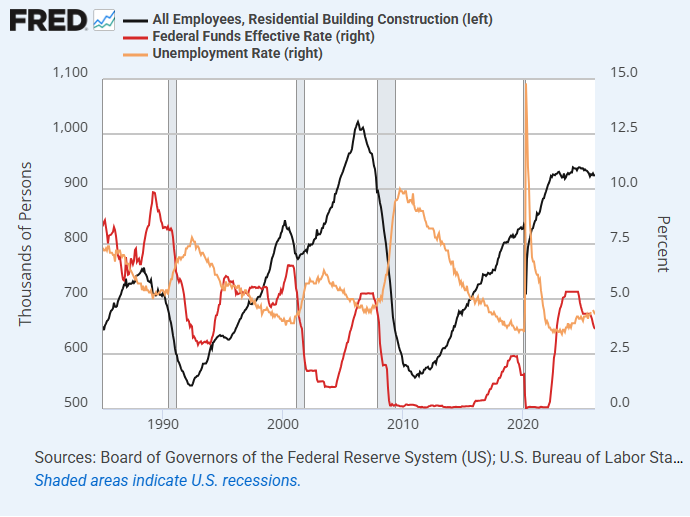

Figure 1 shows a regular pattern through recessions. The Fed raises rates. Residential construction employment peaks and declines. General unemployment stops declining. The Fed realizes that conditions are deteriorating, but they realize it too late. They start lowering the target interest rate, but not enough to reverse the decline. Eventually, the Fed manages to stimulate enough to stimulate a return to growth. Construction employment leads us out of the recession, and unemployment rate soon peaks and starts to decline.

In Figure 1, the only divergences from that pattern are that construction employment didn’t recover after 2008 until the rest of the economy was already recovering, because we had national Munchausen’s Syndrome and were committed to that outcome. That is why it was such a deep recession. As I have complained many times, even Ed Leamer, the one who could have led us, had Munchausen’s Syndrome, and even wrote in 2015 that there were too many construction workers.

The other divergence is that the Fed had started cutting rates before 2020 even though residential construction employment was still rising, and then Covid interrupted the normal cycle.

Looking more closely at more recent trends, they have all the markings of a would-be recession under the condition of a ridiculous housing shortage. The excess inflation that followed Covid ended abruptly in July 2022 when the Fed Funds rate was still quite low. I think, arguably, all of the rate hikes since then were recessionary. It doesn’t matter. It’s really hard to create a recession with a ridiculous housing shortage.

So, construction employment stopped rising in the summer of 2022, almost immediately after the Fed started raising their target rate. Mortgage rates had started moving higher earlier, and while I think the effect of mortgage rates on construction activity are a weaker, secondary factor, the rise was steep enough that it might have been a factor, too, regarding the exact timing and shape of the flattening of residential construction employment.

By mid-2023, unemployment had bottomed. That’s the official start of the almost recession. The Fed was very late to lowering the target rate in September 2024. But it didn’t matter. It’s very hard to have a recession when there is a ridiculous housing shortage.

It looks like the unemployment rate has peaked. It went from 3.4% in April 2023 to 4.5% in November 2025, and was down to 4.3% in January. I think the main reason residential construction employment hasn’t led the way out of the would-be recession is that the sector is capacity constrained by other factors outside of labor.

Also, migration into high-growth regions is a trigger of new home construction, and the moderation of migration into the southern growth regions still has not corrected back to cyclically neutral trends. When it does, expect to see new single-family home construction activity finally rise.

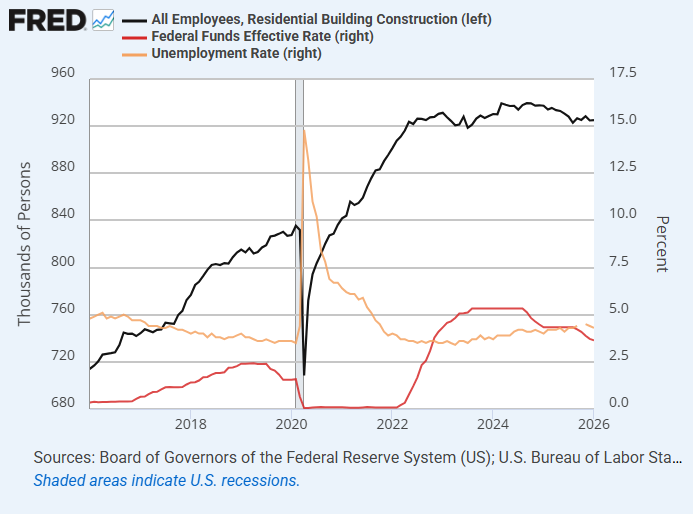

November and December’s new home sales numbers were both higher than any month since 2022. They might be revised down. But I think it is possible that we are seeing the early green shoots of the next step up. Possibly, homebuilder guidance will start to surprise to the upside.

This reminds of my days working for the S&L industry, junior lobbyist, circa late 1970s.

Back then, it was whack the housing sector to cool the economy, in spades.

Hard to digest fact: In 1972, the US was building housing units at 2.5 mil a year. On a population of 208 million.

Now the US has 350 million people. About 1.4 mil housing units a year being built.