Rents shouldn’t influence monetary policy

I exclude rents from inflation indexes when I analyze monetary policy. I have excluded it for years. I wrote a chapter for my books arguing that policy algorithms like the Taylor Rule should exclude rent from their price indexes. I removed that chapter in both cases to streamline the narrative. In hindsight, I probably should have kept it in “Shut Out”, because I think it is important. But, by the time I realized that it didn’t fit well in “Building from the Ground Up”, Shut Out was finished and printed. Although, I have developed the idea a bit further since then, after having more time to consider the price patterns that I found in my Mercatus papers and that I use in the EHT.

So I have written about it, but I don’t think anything thorough has reached public eyeballs.

First, I am not alone in this thinking. The methodological lags in the collection of rent price indexes has been a problem during and after the Covid transitory inflation. JPow! has talked about that a lot, but he tends to return to reporting the full index when addressing the press.

But, that’s a temporary issue. There are other problems with using rent to inform cyclical monetary policy decisions.

The CPI is the price index compiled by the Bureau of Labor Statistics. Shelter accounts for about 1/3 of the CPI and about 45% of core CPI (CPI without the volatile food and energy components). Shelter is mostly rent.

The Personal Consumption Expenditures price index is compiled by the Bureau of Economic Analysis. Housing is only about 15% of that index. The PCE index is technically the index that the Fed targets to 2% inflation. Since housing is a smaller component of the PCE index, it has tended to run lower than CPI in the recent decades that have been affected by the housing shortage.

But, the CPI is published with more detail, and so it is the index that tends to attract public discussion. It is the index I will focus on here.

Imputed Rents of Owner-Occupied Homes

Most homes are owned, and owned homes tend to be larger and more valuable than rented homes. So, about 25% of the CPI Shelter component is cash rent paid by tenants and about 75% is imputed rental value of owner-occupied homes.

Europe uses the Harmonized Index of Consumer Prices. Those indexes exclude imputed rents of owner-occupied homes.

It makes sense for some indexes to include the rental value of owned homes. It makes sense as an estimate of cost of living and quality of life over time. It needs to be accounted for in GDP statistics. Homes provide the service of shelter over time, and it wouldn’t make sense to exclude the value of that service from our estimates of economic consumption.

But, it doesn’t makes sense to include rental value of owner-occupied homes in cyclical monetary policy analysis. A family living in a home, free and clear or with a fixed mortgage payment, mostly only has changing utility expenses, which are accounted for separately, and occasional maintenance and repair. A change in the rental value of their home has no direct effect on their household spending.

As I mentioned in the previous post, one reason that the Fed tightened leading into the Great Recession was because rent inflation was high (Figure 1). Core CPI inflation excluding Shelter had been well below the 2% target for most of 2007.

Core CPI inflation roughly averaged 2% from 1997 to 2020. Core CPI excluding shelter was rarely above 2%. CPI Shelter inflation was never below 2% except for 2009 through 2011 during the foreclosure crisis when millions of families involuntarily lost their homes.

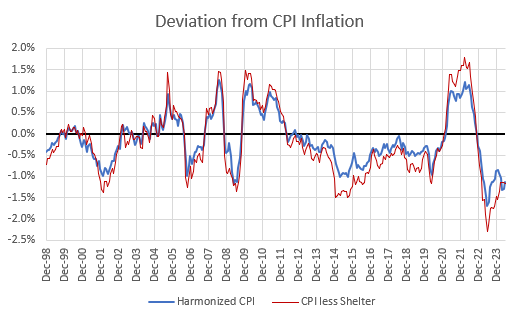

Figure 2 shows how much indexes that exclude Shelter have deviated from the CPI index over time. (Basically the distance between the black line and the blue line in Figure 1, except here I am using the full CPI index instead of core CPI.) The red line in Figure 2 is CPI with Shelter excluded. The blue line is Harmonized CPI, meant to match the European price indexes. You can tell that the exclusion of shelter from the harmonized indexes is the main difference between them and the CPI index because the harmonized index parallels the CPI excluding Shelter measure in Figure 2.

The main difference is that the CPI less Shelter index excludes all rent, not just imputed owner-occupied rent. So, basically, the deviation of harmonized CPI inflation from the standard CPI inflation has about 3/4 of the volatility of the CPI less Shelter, since owner-occupied rent is about 3/4 of the Shelter component.

Housing construction tends to be a leading recessionary indicator. And, it is natural that if production of housing slows, rents will rise. It is common for recessions to follow a period of Fed rate hikes. And, as Figure 2 shows, in the periods leading up to each of the last 3 recessions or early in the recessions, in 2001, 2006-2007, and 2013-2020, inflation indexes that exclude rent typically were 0.5% to 1% lower than the full CPI inflation estimate. Rent inflation has pushed the Fed to be tighter leading into recent recessions.

And, remember, almost all of that rent inflation is imputed rental value of owned homes that the homeowners aren’t even aware of. It doesn’t involve the use of cash or money at all. Yet, the Fed has tightened the money supply because rent inflation was high.

What Should Get Measured?

Really, the fact that imputed rents are largely divorced from short-term, cyclical spending trends is plenty of reason to exclude it from price indexes that inform cyclical monetary policy decisions.

But, I think there are additional reasons why all rent should be excluded - even cash rent. The rent and price patterns that I have discovered and written about illuminate some of these reasons.

First, let’s back up a bit.

Prices are part of a dense web of signals. When something is in short supply or when it is sought after, the price goes up. Those higher prices signal to producers that it is worth more effort to make more of it. Prices do all the heavy lifting in a modern, complex economy. They tell investors and workers to make more engines and fewer buggy whips. More communication software and fewer telegraph machines.

You have to be careful about excluding things from price indexes because everything is codetermined. If consumers must spend more on one thing, then they have to spend less on something else. If producers invest capital in one good they have to reduce investment in another good. If you exclude the inflation from one category, then you are creating observer’s bias, because inflation in other categories might be lower as a result of the extra spending going to the inflated category.

There is always a distribution of price trends around the average inflation rate, and all those individual parts of the whole are part of the broader web of information that directs production into different products.

There are a lot of transfers that aren’t related to production, and so we don’t track them as part of consumer inflation, personal consumption expenditures, or GDP. If someone gives you a gift or steals from you, that is just a transfer. It doesn’t raise GDP. If you give old clothes away or sell them at a garage sale, that is generally not included in aggregate price and production data.

There are some used items that are tracked. Durable goods, which are used over time, are a bit more complicated. The effort to produce a car is complete when it is sold, but the service of transportation will happen over a period of time. And, demand for new cars is related to the prices of used cars. If an innovation allows cars to have a longer use-life, then the functional supply of cars will increase. That might lower the prices of used and new cars, and allow for more spending on other goods and services that might raise other prices. So, used cars are arguably part of that web of production decisions.

Land vs. Structures

Before the 1980s, you could say the same of used homes. The United States was producing an adequate quantity of homes. Residential investment was high. Land values were low and stable.

In that context, used homes are like used cars. The production was complete when the homes were finished, but the service of shelter was delivered over a long period of time. This creates a relationship between used homes and new homes. New construction innovations that allow larger homes to be constructed more cheaply might lower the price of older homes. The prices and rental values of old homes are a reflection of all those tradeoffs and changes in productivity. Or, if there aren’t innovations in new construction and new homes get more expensive, the rental value of old homes may rise.

The rents on old homes, in that context, reflect signals in both directions about decisions to consume and produce.

That is mostly not true about rents on old homes today. Housing is a bundle of a structure and the land it sits on. More than 100% of the increase in American rent, as a percentage of total spending, since the 1970s is due to higher land value.

There are a few different ways to see this.

One way is to compare rent inflation and the growth of real rent over time to other forms of consumption (Figure 3). If we assume that construction costs are stable, an increase in real rents reflects new or improved structures. An increase in rent inflation reflects rising rents for the land. Figure 3 shows these trends for housing, relative to other goods and services. The rising price index is excess rent above the general rate of inflation (Here, using PCE data).

As Figure 3 shows, homes aren’t getting more expensive because they are getting better and bigger. They are getting more expensive, all else equal.

Are homes getting more expensive because it costs more to build them, or because the land value is rising?

Let’s say in a very simple economy existing homes cost $100,000 with minimal land value. Because of a lack of productivity improvements, a new home now costs $105,000. In that case, all home prices might rise to $105,000 because of the higher replacement value. Few new homes would be constructed because families would cut back on the housing they consumed until the cost was back in line with incomes.

So, that condition would lead to a rise in rent and price inflation and a decline in real growth, just like in Figure 3.

In that same simple economy, if 1,000 existing homeowners passed a rule that only one new home could be built each year, then if there were 10 new families, homes might be bid up to $105,000. The higher price would cause some families to reduce their housing consumption so that only one net new home was used.

In that case, there would be a rise in inflation and a decline in real growth, just like in Figure 3, even if construction costs remained the same.

So, what has been the cause of housing inflation in the US? Is the construction more expensive or is it the land?

One way to tell is to compare the change in home prices over time to the change in the cost of building homes over time. And, furthermore, we can compare the change in existing home prices and new home prices over time to the cost of building over time.

Figure 4 does that. Over nearly 40 years, the price of new homes per square foot has roughly tracked the cost to build them. The price of existing homes has risen by substantially more than that. The difference from the mid-1990s to today amounts to nearly 40%. Existing homes have inflated 40% more than new homes.

Productivity has been notoriously poor in construction. And there is excess inflation in the cost of residential investment. Figure 5 shows that inflation in residential investment has outpaced general GDP inflation by 50% to 85% since 1995. This suggests that both issues are at play - higher cost of structures and increased land rents.

Notice the pattern in Figure 5, though. The highest inflation has been in multi-family structures, followed by single family structures, followed by other residential investment (other forms of housing, improvements, brokers’ commissions, etc.). The cost inflation has been highest in the forms of residential investment that face the most opposition.

In many ways, political opposition to housing is manifest as higher costs - queueing for and responding to design review; waiting for inspections; adding mandated designs, materials, or amenities; etc.

One way I would put a lot of the high costs that have crept into American housing is that zoning and land use regulations basically make the cost of many potential projects infinity, because they are simply prohibited. So, high costs end up being a negotiating tool for the developers. “What hoops can we jump through to get the cost of this project from infinity to $2 million?” Maybe in an unburdened market, it would only cost $1 million to build that project. But, $2 million is better than infinity. And, if a city has obstructed enough other housing, maybe $2 million can still bring in enough rent to justify the cost.

So, a lot of costs are downstream of political obstruction. And it would be hard to quantify all the ways that happens.

This is where the Erdmann Housing Tracker Model can be useful for thinking this through. There is a predictable pattern in American housing markets that can further help differentiate land rents from construction costs.

Figure 6 shows home price/income ratios across the metro areas for 2002 Phoenix (which was building 13 new homes per thousand residents), 2024 Phoenix (9 new homes) and 2024 LA (2 new homes per thousand residents, similar to rates common there for years).

Most cities before the 2000s looked pretty similar to Phoenix in 2002. And, before the 2000s, a square foot of housing cost more hours of the average worker’s labor than it does today, if only because real wages were lower. Homes were much smaller then than they are today. And, in every city, households could sort themselves among the stock of homes in a way that was affordable for almost everyone. If you look far enough in the past at families with low enough incomes, we might bristle at the quality of their homes, but the cost was manageable.

How do we know the cost was manageable? Millions of poor families were moving into LA and New York then. Today millions of poor families are moving away.

So, we know what a market that is defined by high costs looks like. Most markets before this century looked like Phoenix in 2002 in Figure 6. Homes were affordable, but homes were smaller and there were more people living in each of them.

Also, the average family in the past spent a smaller percentage of their income on rent than the average family today. When the extra hour of work doesn’t get you much more shelter, you tend to buy less of it. Rents take more of the average family’s income today because families have to pay land rents in order to remain close to grandma, a job, friends, a place one understands and feels a belonging in, etc.

People will pay more rent for all those things and sometimes will even go without shelter for all those things. People don’t systematically break the bank for 200 extra square feet.

Of course, the notion that they would break the bank for 200 extra square feet is popular in the confused miasma of conventional wisdom about our “housing bubbles”. There are always differences in the cross-section of personal decisions, and so there are always risk-takers to point to when the economy turns south or costs rise.

As Figure 6 should make clear, rents have gone up more on the single mother trying to make do in a run-down 70 year old house in a declining part of town than they have on the 3,000 square foot McMansion that you might imagine someone breaking the bank for.

This is a common problem in these micro- vs macro- details. When there aren’t enough houses, homelessness rises. But, homelessness will obviously be correlated with personal issues. The most vulnerable residents will be homeless. Many of them will have made some poor decisions. And those poor decisions will be easy to point to as explanations for their fate.

Blaming the 2000s bubble on covetous overspending and blaming homelessness on drug addiction and mental health are two expressions of the same cognitive bias.

The high cost of housing in American cities today is the result of wholesale obstruction of new units, which creates a bidding war for the land underneath those homes. It is a bidding war richer households win, by simple brut force of having more money.

If construction cost was the cause of a significant part of high rents and prices, rents and prices wouldn’t be so negatively correlated with housing production across metro areas (2 units in LA vs 9 to 13 units in Phoenix) and they wouldn’t be so negatively correlated with incomes within metro areas (13x income in poor LA and 7x income in poor Phoenix vs 3-4x income in rich neighborhoods).

Additional Theories About Rents

Also, if my intuition about home valuation multiples is correct, if land fetches a much higher price/rent ratio than structures do, then higher construction costs would not lead to higher price/rent ratios. Price/rent ratios would be stable. Price/rent ratios have been elevated.

Finally, as I noted above, home prices could only rise to such heights in cities like Los Angeles because of the idiosyncratic value of endowments. The value of staying near grandma, etc. When the price of a commodity, like a bushel of corn, rises, it is true, pure inflation. But paying a ransom to live near grandma is not commoditized. It’s very personal. Nobody can produce a grandma in another city to respond to that price signal. The reason families are paying such high premiums is precisely because they can’t trade grandma for something else. There can’t be grandma arbitrage markets.

Families would happily move rather than pay exorbitant rents if they weren’t tied down to those endowments. This goes to my argument that scarcity and families paying to avoid regional displacement are more important than agglomeration economies in our high home costs. Price signals from agglomeration value could direct new production. If high rents were from agglomeration value, there could be an argument for considering them in monetary policy.

Scarcity comes from blocked production and the high rents it leads to come from families sorting into those who will move to economize versus those who will pay all they have to stay put. A personal, idiosyncratic, non-tradable, unproducible value. Not a price connected to production.

So this is two layers of abstraction from the interconnected web of prices and production. Paying a ransom price for land so that you can remain in a place that has deeply personal value you can’t give up.

Concluding Remarks

Is it all land rents? I can’t say for sure. It is possible that high construction costs from low productivity in residential investment also are having an effect. Maybe in addition to the affects of the asymmetrical price/income ratios across cities, all homes are a bit smaller than they would otherwise be, and the number of members of the average household might be a bit larger than it would otherwise be.

However, those huge variances in rent and price between and across cities suggest that land accounts for the vast majority of the excess rent inflation and excess valuation.

My point is that those extreme changes in prices, negatively correlated with incomes, in Figure 6 are clearly land rents. Land is not produced. It was here, and someone has ownership of it. When rents on it rise, we don’t make more land. In fact, when rents on it rise, we don’t even make more houses. That is because the land rents are not natural. They are enforced.

They could decline someday, and when they do it will be because we have produced more homes. But, in the meantime, there is no reason to treat even cash rents as a component of consumer inflation. It is a transfer. Ten years ago, someone paid their landlord $1,000 for a structure and $100 for the land under it. Today, they pay someone $1,000 for the structure and $1,000 for the land under it.

It’s like a gift or a theft or a ransom. Money in one person’s pocket instead of another’s. It isn’t consumption or production or a change in total income. It’s a transfer. Currently when there is rent inflation, we treat that transfer as an increase in nominal income and production while real income and production remain unchanged.

I am strongly in favor of a Fed program of targeting nominal income growth instead of inflation. But, here, they both have a similar problem. A transfer is being treated as inflation and as an increase in nominal income. The only way that transfer is going to affect production is that the landlord will choose to spend it on a different set of goods and services than the renter would have. But it creates no direct change in the price signals of those goods and services as a result of the land fetching a higher toll. It isn’t really income. No labor or capital were involved in its creation.

Every once in a while, you’ll see an attempted “Gottcha” on economists where someone will describe two people repeatedly paying each other for an item they keep trading back and forth, and they will say that this increased GDP. Economists will then patiently chime in to explain that this is not GDP.

But, economists are doing something similar with rent on inflated land value. The payments are all in one direction, but they are just as divorced from economic production as the proverbial item being repeatedly traded.

It would be too difficult to try to adjust GDP statistics for this. And, it remains an important signal for cost of living, etc. But, we should exclude rents from inflation indexes used to direct monetary policy.

Describing this in terms of endowments and transfers makes a lot of sense. Great food for thought, thank you for sharing.

Btw, Singapore leaves rent out of core-inflation.