"Reassessing the role of supply and demand on housing bubble prices" (PART 2)

Think of these posts (part 1 is here) as supplements to the paper. I’m working through some of the details a little differently than I did in the paper. (I first looked at the problem of controlling for incomes in Appendix 3 of the previous paper.)

In this post, I’m going to step back a bit and look how my price/income slope helps to highlight trends in housing compared to some of the existing literature.

It is hard to intuit how much of the high prices of the supply-constrained cities falls systematically on families with lower incomes. Figure 1 shows incomes and home prices across Phoenix and Los Angeles in 2002 on linear scales. It’s hard to tell here that prices are especially high for low-income Angelinos.

Figure 2 shows incomes and home prices in Phoenix and Los Angeles in 2002 and 2006, but this time both axes are on a log scale. An odd thing happens when you do this. The trendline of home prices in every city basically line up like rays from a single source.

I think the reason is that spending on housing is highly determined by income. In an unconstrained context, people will tend to spend something like 3 or 4 times their income on a home. For households with high enough incomes, where, on the margin, all their housing expenses are for luxuries, it is easy to make adjustments so that their spending falls in that comfortable zone.

Where housing is expensive, it is due to municipal rules that act as barriers. Homes will be torn down by the representatives of an effective governing body, supported by the citizenry, unless that governing body has permitted their construction. This creates scarcity, which inevitably favors those with more resources. Since shelter is a human necessity, families with fewer resources must increase their spending above that comfortable level in order to claim some for themselves.

2002 Phoenix had relatively ample housing supply, and so home prices across the metro were pretty similar. There was no bidding war for an artificially scarce asset. It has become less ample over time. And, housing is exceptionally scarce in LA, so home prices swivel up and down as if tethered at some point where incomes are very high.

It is still hard to intuit this pattern, because the baseline case - Phoenix in 2002 - rests on an angle. And, that is one reason why viewing housing costs as a price/income ratio is a helpful first step to thinking about housing affordability. Figure 3 compares these 4 city & time combinations using price/income.

They still act as if they are tethered at some fulcrum point at the lower right. But, now, the baseline is an easily conceived flat line, and deviations from that flat line are expressed as the slope of a line. Phoenix, in 2002, had enough housing that practically any family could live in a home whose cost was somewhere close to the comfortable range. Income still determined the price and quality of each family’s home, to a large extent. But, families didn’t have to spend more than that comfortable range.

It is true that the slope of the price/income line increased in both Phoenix and LA from 2002 to 2006. That is, in part, a reflection of changing demand. So, it is not wrong to say that rising prices from 2002 to 2006 were triggered by a boom in housing demand. And, the existing literature notes that demand drives prices higher when supply is constrained (inelastic, the economists call it) than when supply is unconstrained.

But, there is an interaction with income here that, as far as I can tell, has gone largely unnoticed. In any context, under any given demand conditions, homes are more expensive in LA than they are in Phoenix. And, furthermore, they are systematically more expensive for poor families in LA than they are for richer families. And, furthermore, in the 2002 to 2006 boom period, the prices from city to city changed in proportion to the pre-existing conditions. In other words, where poor families faced higher costs in 2002, their costs rose proportionately higher.

This is a subtle distinction, but it makes a transformative difference in how you think about changing home prices, and the forces that are changing them.

Atif Mian and Amir Sufi famously argue that newly loose access to credit was the primary driver of rising home prices during this period. They note the importance of credit scores (which correlate with income) in their conclusions:

House price growth was similar from 1998 to 2002 in high and low credit score zip codes. However, house price growth was much stronger in low credit score zip codes from 2002 to 2006, especially in inelastic housing supply cities. To our knowledge, proponents of the passive credit view have never addressed this pattern. Why did house price growth accelerate so much more dramatically in low credit score zip codes? The credit supply view provides an obvious explanation: mortgage credit for home purchase was expanding rapidly in these neighborhoods, which pushed up housing demand. In inelastic housing supply cities, house prices rose in response to the demand shock.

They continue:

In cities with very elastic housing supply, there was little house price growth from 2002 to 2006 and there was little reason to expect house price growth from an ex ante perspective. Yet even in these cities, mortgage credit expanded by more in low credit score zip codes seeing a relative decline in income growth. When we shut down the house price growth expectations channel by focusing on elastic housing supply cities, we still see an expansion in mortgage credit to low credit score individuals. This supports the view that the expansion in mortgage credit supply was not simply a function of house price growth or house price growth expectations. To our knowledge, advocates of the passive credit view have not addressed this test from Mian and Sufi (2009). If the expansion of mortgage credit supply to marginal households was purely a function of house price growth expectations, why did such an expansion occur even in elastic housing supply cities with no house price growth?

In fact, supply constraints always push up prices more in ZIP codes with lower incomes, regardless of credit conditions. Expansion of mortgages on the extensive margin is not necessary for that. And, the continued increase of home prices in ZIP codes with low incomes since the Great Recession, in spite of very tight lending standards, confirms this. Mian and Sufi are correct that there was an extension of lending from 2002 to 2006. Surely, it must have been a factor in the rising demand for housing. But, mortgage expansion is not necessary to get these price trends.

There was an expansion of mortgage credit at that time. But that isn’t why prices increased so much in poor neighborhoods of some cities.

Controlling for differences in metropolitan area prices and incomes may have exacerbated these issues.

In Appendix 3 of my previous paper, I noted that “recent work from Card, Rothstein, and Yi and Hoxie, Shoag, and Veuger has shown that housing supply elasticity is a primary driver of different metropolitan area income trends.”

“Before regional differences are removed, the low-tier ZIP codes in Los Angeles that experienced such high price appreciation had relatively normal income growth. But when compared to other ZIP codes in their counties, as they were in Mian and Sufi’s analysis, they appear to have the lowest income growth in the country. That outcome is likely the result of geographical controls and adjustments in Mian and Sufi’s data; by attempting to control for regional variations, they may have introduced biases from regional variations.”

“It is possible that metropolitan areas with inelastic housing supply create more variance in ZIP code income and more credit stress in ZIP codes with low incomes, so that the variables Mian and Sufi used were not independent. The correlations between ZIP codes with low incomes within their counties, negative relative income growth within their counties, high credit stress, and high price appreciation could all be caused by inelastic housing supply.”

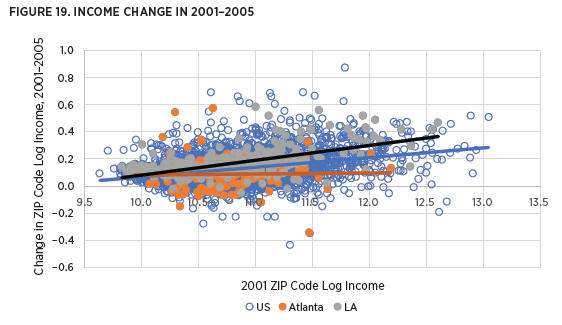

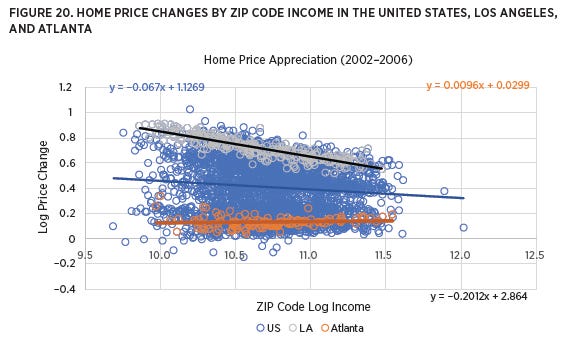

Figures 4 and 5 are figures 19 and 20 from my paper. In the first, you can see that during this period, income growth in LA was more varied and more top-heavy than most cities. Atlanta is shown here as a counterexample along with national data. The poorest ZIP codes in LA had similar income growth as the poorest ZIP codes in Atlanta, but they had much lower growth than the richest ZIP codes in Los Angeles. And, in the chart of home price changes (Figure 5), you can see that in amply supplied Atlanta, prices increased similarly across the metro, while in Los Angeles, prices increased more in poorer ZIP codes. Controlling for regional differences makes it look like those poor neighborhoods in Los Angeles simultaneously had the lowest incomes, the worst income growth, and the highest home price appreciation in the country. All of those issues may be related to the lack of housing supply.

The regional controls make their incomes and income growth look bad. And mortgage expansion isn’t necessary to cause home prices to rise more in ZIP codes with low incomes. But, you can see how Mian and Sufi could be easily and firmly persuaded that these trends confirmed the central importance of credit supply.

Finally, Figure 5 here highlights again just how overwhelmingly important the city was in determining price trends. Mortgages or no mortgages, high incomes or low, ZIP codes in Atlanta and Los Angeles experienced vastly different trends of a much higher scale than the intra-city differences. That is the story here. The rest is a footnote in either case. And that footnote was largely determined by supply constraints.

There are cities that traditionally have looser local housing supply, where, nonetheless, prices shot up similarly to Los Angeles during that time - places in Arizona, Florida, Nevada, and inland California. These are the cities I call “Closed Access” and “Contagion” cities, respectively. And, I think the comparison between those cities is informative.

Figure 6 compares price changes from 2002 to 2006 for 4 pairs of metro areas. The gray metros are Closed Access cities whose populations were stagnating and even declining at the time, where tens of thousands of families - generally families with low incomes - move away every year and were especially moving away from 2002 to 2006, where home rents and prices are especially high, and where even at the beginning of the period housing costs were especially high for poor families. The red metros are Contagion cities whose population growth generally has been higher than average, where population growth spiked from 2002 to 2006 (mainly because of the families moving away from the Closed Access cities), and where generally price/income ratios were relatively similar for poor and rich families in 2002.

Without exception, the negative correlation between price appreciation and income is in the Closed Access cities. The Contagion city with the most slope is Miami. And Miami is the Contagion city that has the most Closed Access-like characteristics - for example, average permitting rates and a relatively steep price/income slope in 2002 at the beginning of the period.

So, even where other cities experienced high price appreciation and active lending markets, there wasn’t much income-sensitive price appreciation. It’s only in the Closed Access cities.

In Figure 7, you can see that by applying controls to erase differences between metro areas, these differences are exaggerated. This is systematic across the country. The income-sensitive price appreciation that Mian & Sufi took as confirmation that credit to buyers with lower incomes was driving prices higher only shows up in cities that were bleeding low-income families at a massive rate.

Figure 8 aggregates the 28 metro areas in my data set into “Closed Access” and everything else.

So, there is a bit of a two-step dance that happens with our experiences of this period, the academic research, and the conventional wisdom about what happened. When I present my retelling the the boom and bust to Phoenix audiences, there are inevitably insiders in the audience who are indignant at my attempt to rewrite history.

“I was in the trenches! I saw these loans being tossed out to anyone with a pulse! And, you’re going to come here and tell me it didn’t happen?!”

But, the evidence that the “credit supply” academics point to as confirmation of their thesis didn’t happen in Phoenix! It didn’t happen in any of the “bubble” cities. It only happened in cities which continue to be expensive for their poorest residents, continue to bleed outmigration of their poorest residents, and continue to refuse to permit an adequate number of homes.

As I wrote in the previous paper:

Most analysis, such as Mian and Sufi’s referenced above, implicitly or explicitly, attributes rising prices in each ZIP code to the character of the residents in that ZIP code. Are they credit-constrained? Are their economic prospects improving? And so on. This seems reasonable. But home prices in the parts of Los Angeles where incomes are lower are not being driven higher because of the rising incomes of their residents. They are being driven higher by the encroachment of demand associated with rising incomes in the other parts of Los Angeles. In Los Angeles’s supply-constrained environment, housing markets are increasingly being driven by substitutions across neighborhoods and across metropolitan areas. The controls applied by Mian and Sufi assume that those substitutions aren’t important and that each ZIP code’s housing market is driven by its own residents.

…Local residents with low incomes weren’t driving home prices in their neighborhoods higher. On net, they were being forced to move to other, less expensive metropolitan areas. The higher prices rose, the more locals with low incomes moved away.

Stay tuned! There are more twists and turns yet to come….