US Residential Housing: A Simple Story in 4 Acts

Don’t read this post as some sort of econometric model. The charts that follow are based on various estimates and simple models I have written about before. Nothing has been estimated to the 3rd decimal point or anything. But, I thought that maybe it would be helpful to walk through the basics of the Erdmann Housing Tracker thesis on American real estate valuations.

tl;dr: Rent explains almost everything. Rent inflation leads to high prices and high price/rent ratios. And there was a credit shock in 2008 that permanently lowered price/rent ratios. That’s it. The rest are details and noise.

Rent Inflation

Figure 1 tracks rent inflation over time. Here, I use the price chain indexes (PCE Owner-Equivalent Rent) / (Total PCE) & (PCE Tenant Rent) / (Total PCE).

Notice how in the past 20 years, these have diverged significantly. This is because rent inflation from supply constraints is highly regressive. That’s a major motivating point behind the Erdmann Housing Tracker. When cities allowed adequate new multi-unit home construction and most families were able to get mortgage financing for single-family homes, the most important effect was that those new homes kept rents lower for non-owner tenants.

Economists talk about filtering - that when you build more luxury homes, the existing homes filter down to families with lower incomes. This is the full implication of filtering. And this is part of the tragedy of the myths of the 2000s housing bubble. Economists that would identify as classical liberals - as advocates for supply-side economic policies - should be the loudest proponents of filtering. It is the ultimate supply-side issue. Building luxury homes for rich families keeps the rent down on old homes that poorer families live in.

But they are lost in the wilderness. They were convinced of the primacy of demand-side causes of high home prices. So, they generally favor the tight lending policies we have had in place since 2008, and they have nothing to say about this. An incredibly clear confirmation of supply-side economics. But, the way to make supply-side economics work again, immediately, is to loosen mortgage lending back up so that millions of families can fund single-family home purchases again. That would bring rents of poor tenants down. It would be a win for America and a win for supply-side economics. And they won’t stand for it. They can’t see it. They won’t see it.

So, as far as I can tell, there is roughly zero academic, political, or advocacy support for the one thing that might be able to reverse the damage of the past 20 years while we work on reversing the damage of the past 100.

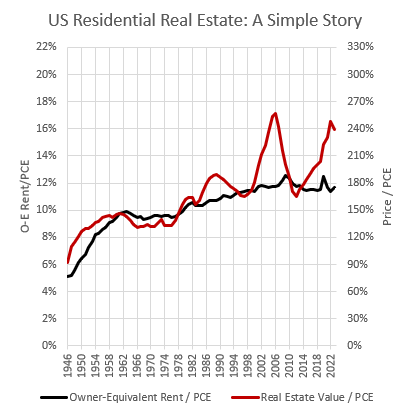

Residential Real Estate Value

In Figure 2, I compare the total estimate of rental value of owner-occupied housing as a percentage of all personal consumption expenditures, and the estimated total value of owner-occupied real estate, relative to all personal consumption expenditures.

You might think that this shows that rent inflation does explain everything, that each 1% increase in rents leads to a 1% increase in prices, that there was a big bubble in the 2000s that reversed, and that there is now another big bubble.

That isn’t quite right. Before the 1980s, when US construction was robust, it was the case that factors such as liquid finance markets and government housing programs increased the consumption of housing over time, especially coming out of World War II. Rent inflation was stable or low, but the rental value of homes was rising because we were building more.

When Americans were simply consuming more housing, then prices remained moderate, or even declined relative to rents. It is reasonable to assume that a 1% increase in real rents (actual walls, roofs, etc.) will be associated with a 1% increase in total real estate values. Until the mid-1980s, the total value of owner-occupied real estate generally was about 15x its annual rental value. (The right scale of Figure 2 is set to 15x the left scale.)

Demand-side factors or progress - productive construction methods, liquid and accessible capital markets, subsidies and taxes - induce more real housing consumption (or less in the case of things like taxes).

But, the rise in rent inflation comes from not building homes, and that leads to much higher home price appreciation.

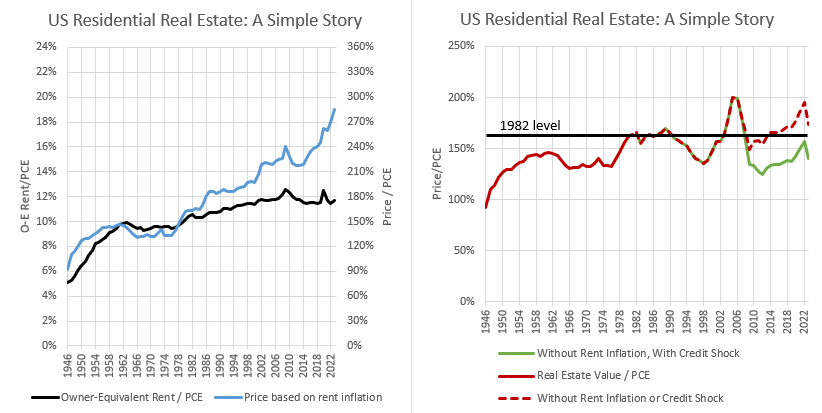

Rent Inflation

Figure 3 adds a new measure to the comparison. The blue line is set to have a sensitivity to the rent inflation after 1982 from Figure 1 of 2.8. For each additional 1% inflationary rental value, home values are set to increase 2.8%. (I have adjusted the post-Covid estimate to reflect rent inflation implied by Zillow rent estimates, since the BEA estimates currently have a lag due to methodology.)

That is the path of relative home values that is related to rent inflation due to supply constraints. That is a price path that is more in line with trends in Canada and Australia. They also have stumbled into a legal system that obstructs traditional city-building, but they did not institute the deep lending shock that the US did in 2008.

As I mentioned, don’t get too hung up here on whether that path should be 10% higher or lower. I’m just walking through the basic conceptual point. There are a thousand papers out there with bad concepts and coefficients estimated to 5 decimal places. The benefit of analyzing an issue that is beset by such extreme outcomes is that we can get closer to the truth by going in the other direction - getting the concept right and not worrying too much about the details. (I did arrive at this coefficient with some regressions of real rent, rent inflation, a credit shock dummy, and home prices over time, but once you have the concept, the coefficients follow, and if you don’t accept the concept, the coefficients probably don’t matter.)

By this estimate, home valuations were a bit bearish in the 1990s, a bit bullish in the 2000s, and very bearish since then.

Credit Shock

In Figure 4, I have added one more measure. Using the credit component from the Erdmann Housing Track, I have added a credit shock to the estimated price. This is a permanent price shock of a little more than 20%. This is the shared price shock after 2007 across all cities unrelated to earlier credit access. In other words, in the average city, the most expensive homes had relatively stable prices after 2007 and the least expensive homes lost more than 40%. (As far as I can tell, the current state of the art in econometrics is to not control for the post-2007 tightening of credit or the extreme changes in prices that were associated with it.)

So, even though it looks like I just fitted the line in Figure 4, the scale of this coefficient comes from cross-sectional analysis both across and within cities.

Finally, Figure 5, in the left panel, compares owner-occupied rental value as a % of total personal consumption expenditures to the estimate of home values that is based only on rent and rent inflation.

In the right panel, I show the theoretical price trends that would have happened, ceteris paribus, if there had been no excess rent inflation since 1982 and if there had been no rent inflation nor a credit shock.

There was still quite a bit of cyclical activity! On that, one reply I frequently get is, “Why can’t it be both supply and demand?” I agree! But, if we take a “Why can’t it be both?” approach, the demand-side factors are (1) cyclical issues that are neutral over time, and (2) lending issues that are decisively austere. At the same time, there is a 75% premium (and growing!) on American housing that is entirely from the supply problem.

All three issues affect home prices, and all three have the power to push prices up. And, the appropriate response to what they are doing is to focus entirely on the supply problem. In practice, the “Why can’t it be both?” approach is generally a way to hold onto overestimates about the effect of demand factors on housing costs. The aggregate price/rent ratio has gone from 15x to 24x. That is a supply problem, and it is really easy to keep believing that is a demand problem. “Why can’t it be both?” enables that mistake. Treating elevated price/rent ratios as a demand problem led to the credit shock. It is the cause of most of the supply problem.

The 4 Acts

Act 1: pre-1982 - building and real growth

Act 2: 1982-2007 - regional building constraints, rent inflation, excess value

Act 3: 2007-2012 - credit shock

Act 4: 2012-2024 - nationwide building constraints from the credit shock, nationwide rent inflation, prices inflated from rent and deflated from credit shock

Act 5: 2024-future - New build-to-rent neighborhoods might stem future excess rent inflation and stop additional price appreciation. I think a return to more generous lending to owner-occupiers will be required to reverse it in the mid-to-long term.

In the very long term, I think it may reverse on its own. General supply and demand issues would not be able to push the aggregate value of owner-occupied homes sustainably above 200% of personal consumption expenditures. The level that I benchmarked to here in 1982 was about 166%, which would be the cyclically neutral value of owner-occupied homes. Demographically adjusted homeownership rates peaked in 1981, so we might reasonably infer that the early 1980s marked the high water mark of home values that reflected pro-housing public policy biases.

Home values are currently about 240% of PCE, and current rents would justify home values totaling 285% of PCE. Patterns of rents and prices within cities suggest that all of that excess value is driven by resistance to regional displacement.

In our peculiar, tightly fettered housing market, prices are driven higher by families who resist helping the market to find an equilibrium. In a market that was just generally limited in the supply of housing, select families wouldn’t spend 50%+ of their budget to remain in cities where they have longstanding endowments and local knowledge. Families would spend, on average, 10% to 12% of their budget, and maybe up to about 30% in some cases, on a smaller home or a home in a different location.

Keeping housing this inflated requires constantly pushing on that disequilibrium and making families less comfortable where they are and where they began. People will revert to spending norms over time. They will acclimate to being housing poor. They will live in smaller units. They will slowly move away from the cities they are connected to. But, that will take decades or generations.

Building more housing now, and funding more mortgages now, will remove the pressures on that equilibrium. All the demand stimulus our current building capacity could take would move us back to pre-Great Recession norms. Then, likely, it would take local land use regulation reform to push aggregate home values down further.

It is counterintuitive, I confess. Demand stimulus might be able to create some cyclical ups and downs - even relatively sizeable ones. It could be that a housing boom would increase the displacement pressures on families in the Closed Access cities (New York, LA, San Francisco, Boston, and San Diego) which are already substantial. But, the potential for downward pressure on home values in the rest of the country is much greater. With maybe some short-term cyclical hiccups, mortgage growth would be associated with lower home values.

Would that we could do it all.

Great post that distills your housing insight.* One-stop shopping, I love it!

* Now if only there was a way to explain your counterintuitive view without recourse to technical PCE ratios, etc., perhaps it could be sold to a wider audience. Still, hopefully some key policy makers get it.

I searched your article and the words "immigration" and "immigrant" do not appear. Any article discussing housing that doesn't address the massive influx of both legal and illegal immigrants is a waste of time. On the other hand, evict the 40 million or so illegals, revoke immigrant status for millions of not-yet-citizens, and bang, housing problem goes away.