Housing needs supply-siders, again

Aaron Brown, Michael Mendelson, & Clifford Asness have an article at the Dispatch titled, “Half of America Cannot Afford to Live, and Other Wrong Numbers”. There is an ongoing debate about whether positive economic indicators or negative consumer sentiment surveys are more indicative of the current American economy. This article is a compelling entry differentiating facets of what is actually happening, and what the appropriate solutions are.

There is something to the notion that average people can’t get by. Health care is a big part of it. It’s a peculiar service where we feel an especially strong sense of shared egalitarianism about access to technically available treatments. As per capita health care expenditures rise to an increasingly large portion of the median income, households are increasingly exposed to financial stress and uncertainty unless we fund progressive transfers to cover unplanned health expenses.

Most of us have to fill out those half dozen forms before any health care appointment promising to give the doctor the discretion to bankrupt us with bills full of $1,000 aspirins if they deem it necessary. On this issue, our own doctors make sure we feel like we are an unexplained headache and an insurance denial away from destitution. So, the rhetoric the authors are pushing against is salient for Americans, even if we aren’t technically living “paycheck to paycheck”. But, the authors’ diagnosis is reasonable. If I may try to paraphrase: We have an embarrassment of riches, some obstructions that make the dispensation of those riches inefficient, and some portion of the population that can’t fund what many consider to be a humane portion of those riches.

On the one hand, our definition of humane is inflated by our general economic well-being, so referring to these problems as “crises” seems presumptuous. On the other hand, it has become harder for some portion of the population to afford a quality of life that we do consider humane, and it sure feels like a crisis to some of those who are dealing with the worst of it.

The authors present anecdotes to helpfully illustrate how national average numbers can hide many nuances and wildly different outcomes.

This kind of mashing is the basic move of the contemporary affordability discourse. Catastrophic situations affecting small numbers of people are blended with mild discomforts experienced by very large numbers, and the resulting mixture is called a crisis…

There are real affordability problems in the United States. Two of them, by our count…There are two groups in real trouble: a destitute tail that is small and brutally squeezed, and a much larger squeezed-talent class that is doing everything right but still cannot replicate its parents’ material life. Everyone else is fine, or fine enough, or in the kinds of trouble we are not obligated to call a crisis. The two groups need opposite remedies, and the “single homogeneous affordability crisis” framing makes that impossible to see.

They propose:

These two problems require completely different policy responses. The first example is a redistribution problem, requiring cash transfers, safety nets, regulatory crackdowns on the worst predators. The second is a supply problem and requires zoning reform, occupational licensing reform, and breaking up the entrenched cartels in housing, healthcare, education, and childcare. The packages don’t overlap.

I agree with the authors’ point that when policies are engineered to solve the “affordability” problem without differentiating between these two separate experiences, public resources tend to be allocated very regressively. For instance, blanket student debt forgiveness might cover $100,000s for a Harvard grad with good job prospects while paying off only a few thousand dollars in loans for a person that was drawn to a half-rate education program that leaves them with few prospects. Paying off student debt for both of them, and leaving it at that, increases the inequality between them.

But, on the topic of housing, Brown, Mendelson, & Asness come up short. In housing, it really is one problem. And it is a crisis. This is similar to the CATO Institute posts I wrote about recently. In both cases, they understand and support some of the appropriate solutions to the housing crisis. But, through a series of empirical blind spots, rhetorical reactions against viewing it as a crisis, and a lack of appreciation for some aspects of the problem, they end up stepping on their own feet, reducing the sense of urgency for some solutions while not seeing the need for other solutions, and actually supporting causes of the crisis.

The “superstar” cities aren’t super.

The authors contrast Americans who are simply poor - lacking in resources - who need public support, with the households in the second group, for which they identify zoning reform as one of the solutions. The key observation they associate with the housing issue is:

Picture a 32-year-old physician married to a 32-year-old software engineer. Combined household income, $400,000. They cannot buy a house in San Francisco or Boston or New York within a sane commute of their jobs.

The “superstar” city and agglomeration explanation for high home prices rears its ugly head. San Francisco, Boston, and New York have a lot going for them. They are places that some people move to aspirationally. But, that isn’t what sets them apart, as a group, from the rest of the country. What sets them apart is that they, along with Los Angeles and San Diego (all together, the Closed Access cities), limit home building to levels lower than any other major city in the country.

These authors, as so many do, have internalized the “superstar” explanation for why they are so expensive, and so they associate these cities with wealth and high-tier amenities. Their example highlights them as cities that rich people want to live and work in. So, without saying it out loud, but simply by choosing what observations to make - what to notice or not notice, what to identify or not identify - they implicitly categorize these entire metropolitan areas totaling around 50 million Americans - as belonging to the “talent class”. They make the common error of thinking that Boston, New York City, and San Francisco are expensive because rich and productive people want to live there, and so it is the homes that rich and productive people live in that are overpriced.

They are overpriced because they have a housing crisis and the reason they seem like places rich families live is because the crisis has forced millions of poor families to move away.

It’s kind of bizarre, if you think about it - the scale of things that have to not be noticed in order to make this rhetorical choice. But, that choice is nearly universal. They would come off as contrarian if they didn’t make that choice.

I can’t be too hard on them. In “Shut Out”, where I was relitigating the 2000s housing boom and bust, I was still writing sentences like “We have been taking out mortgages in a bid to go where the jobs are.” That’s technically true, in that jobs tend to be in urban areas, in general. But, I was wrong to suggest that that described Boston or New York City any more than it described Dallas. They are all creating good jobs and attracting households with high incomes at a similar pace. Boston and New York City just don’t create jobs for residential construction, so they have created a housing crisis that weighs most heavily on their poorest existing residents.

Americans are moving to where new housing is legal. In a nutshell, where it isn’t, the lack of housing creates enough poverty to limit newcomers and remainers to the families with the best jobs.

Just counting net domestic outmigration from those 5 expensive, house-poor metropolitan areas (the Closed Access cities) over the past 30 years, something like 10 million Americans were regionally displaced by rising regional housing costs. That’s net. If there is some amount of revolving migration, where rich or productive Americans move to those cities, and poor residents have to move away to make room for them, then the number of economically displaced residents is higher than 10 million. 10 million displaced Americans is a lower bound on how many Americans were made poor by the zoning problem in those 5 metro areas - poor enough that they chose displacement as an economic remedy.

And, for every household that moved out of those metropolitan areas, there are several households still living in them who are poor because of high housing costs. They are in the first group. And the solution they need isn’t handouts or public support. The only reason they might need handouts or public support is because of the zoning problem.

I agree with these authors that their two groups have some distinct problems and solutions, but on the topic of housing, the problems and solutions are intermingled. And it really is a crisis. If 10 million people arrived on American shores from some other place because remaining in that place had become economically untenable, we would have little problem knowing what to call it.

The authors write that if there were an affordability crisis:

You would expect mass starvation, or at least mass migration out of the country. You would expect the streets to be lined with the dispossessed.

Does mass migration out of cities count as something? And, in case they haven’t noticed, yes, the streets are increasingly lined with the dispossessed.

Those cities have a true shortage. At current rates of building, the way those markets equilibrate is that each year a couple hundred thousand families have to feel poor enough to accept regional displacement. Of course, households have some agency in deciding who leaves and when. But, that dilemma is built into the system. Every year a couple hundred thousand families have to feel so bad about their economic situation that displacement is preferable. For every one of them, there are dozens who feel bad, but not quite bad enough to give up on staying.

And, the only reason it looks like a problem for the “talent class” is because it has been happening for so long that the stress of that process has advanced up to families with six-figure incomes.

There aren’t two stories for housing. There is just one.

In other words, the observation these authors make about the stress on the family in Boston earning $400,000 a year is, accidentally, a confirmation of the intuition that “half of America can’t afford to live” that they are attempting to counter. This error shows up again, and again across the political spectrum. They think nicer places, where the “talent class” lives are getting more expensive. That’s not true. It’s the opposite. They think this is a “talent class” problem, but the only reason it is a problem for that family is because the problem of being poor (because of costly housing) is reaching up toward families with six-figure incomes. Of course, it doesn’t pose an existential problem for the rich family, because with that level of income, they have choices. But, it is exactly the same problem that the poor are having, just of a lesser scale.

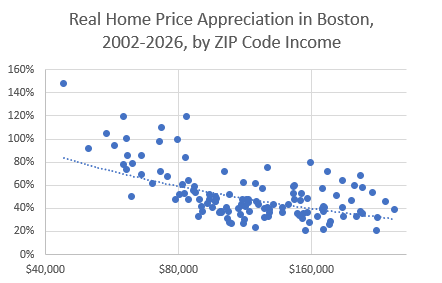

Figure 1 shows real home price appreciation across Boston, by ZIP code income. At the high end, prices are up around 40% adjusted for inflation. At the low end, they are up 100%+. To keep housing affordable, the hypothetical rich family above has to compromise on things like commute time. Families with incomes below the median don’t have anything left to compromise, so they mostly get inflated rents until they leave the region.

Just mull this over for a moment, given Figure 1. Think about how universally misguided the approach to the housing crisis is that directing their observation about high housing costs in Boston to a family with an income of $400,000 instead of to families with $60,000 incomes will meet little resistance from readers of the article, on either side of the debate. Fundamental misdirection stipulated by all sides as true.

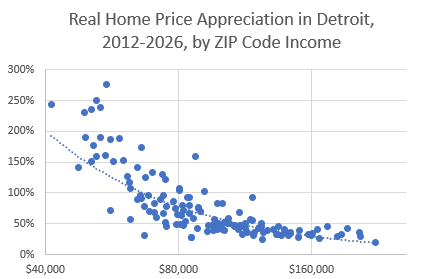

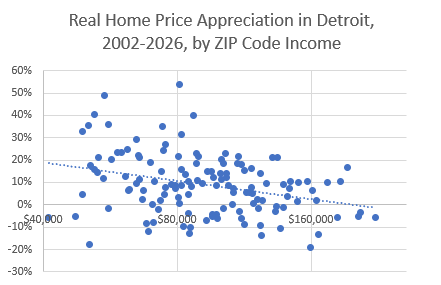

The mortgage crackdown in 2008 brought construction activity across the country down to Closed Access levels, and so, since then, every city has developed this pattern. Figure 21 shows real home price appreciation in Detroit since 2012.

There are similar patterns across the country in rent inflation, though the scale isn’t as high as in price inflation because each 1% of inflated rent is associated with more than 1% of price inflation.

Notice how there are a lot fewer ZIP codes with incomes below $80,000 in Boston than in Detroit. The most important reason for that is that families making less than $80,000 moved away from Boston. The reason the $400,000 family is feeling stressed in Boston is because the housing crisis makes $400,000 feel closer to being poor than it used to.

There are a lot fewer ZIP codes in Boston with average incomes under $80,000 in Figure 1 than there are in Detroit in Figure 2 because it is harder to live in Boston on $80,000. Boston has a housing crisis because the shortage means that there aren’t homes in Boston for families who don’t have high-paying jobs.

The poorest residents across the country now have the same pressures as the poor residents in Boston and New York City. Of course, they have a lot further to go to catch up to the high costs of Boston and New York City because the shortage in Boston and New York City has been binding for longer. On the other hand, the formerly poor residents of Boston and New York City had cheaper cities to move to. That option is being closed as other cities become more expensive.

The housing crisis has nothing to do with subsidizing demand.

The issues above aren’t particularly conservative issues. They are pretty universally shared blind spots. The conservative part is the authors’ sentiment toward demand. They note the problem of subsidizing demand while obstructing supply. And, this can be a legitimate problem. It is an important element in the high cost of health care, for instance, because if someone is in an accident or contracts a communicable disease, we feel a moral obligation to subsidize demand for their healthcare.

Regarding subsidized demand for housing, they write:

Federal housing policy since the 1930s—the GI Bill mortgages, FHA, Fannie and Freddie, the mortgage interest deduction, the low-income housing tax credit, Section 8 vouchers, the Community Reinvestment Act—has been an enormous, sustained, bipartisan effort to make housing more affordable. The cumulative subsidy probably runs into the tens of trillions in present value over the postwar era. And the result is that housing in productive metros costs more relative to income than at any point in living memory.

The reason is not a mystery. Essentially all of these programs subsidized the demand for housing while local zoning rules restricted the supply. Subsidies that meet a fixed supply capitalize into the price of land.

This is sloppy and wrong. First, they leave out some things. They leave out the fact that homeowners don’t have to pay income tax on the rent payments they don’t have to make to themselves that a landlord would have to claim as income. That’s the largest subsidy for housing, and for homeowners, by quite a distance. The mortgage programs hardly amount to anything in actual dollars, compared to it, and arguably aren’t even a subsidy any more. Now they are more a managed oligopoly that collects economic rents in excess fees for the federal government while private lenders are prevented from competing.

But, more importantly, the authors don’t mention property taxes, which are several times larger than all of these subsidies, combined. Property taxes are a sort of consumption tax aimed specifically at housing. Property taxes are a good tax. I support using property taxes. But, since we have them, on net, we are definitely not subsidizing demand for housing. Housing isn’t expensive because of subsidies.

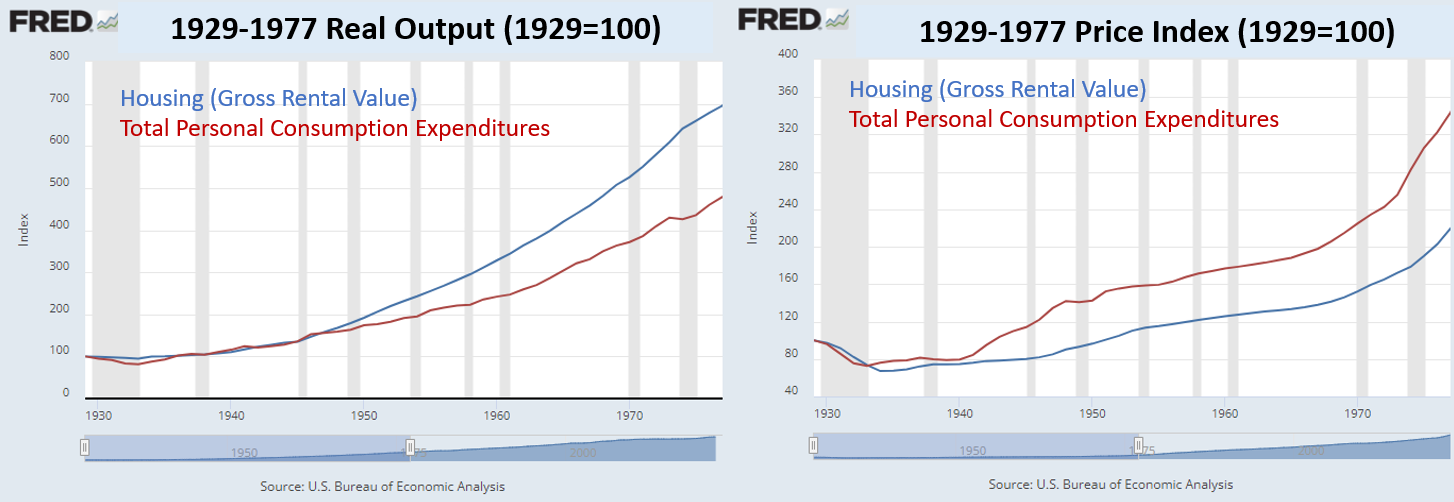

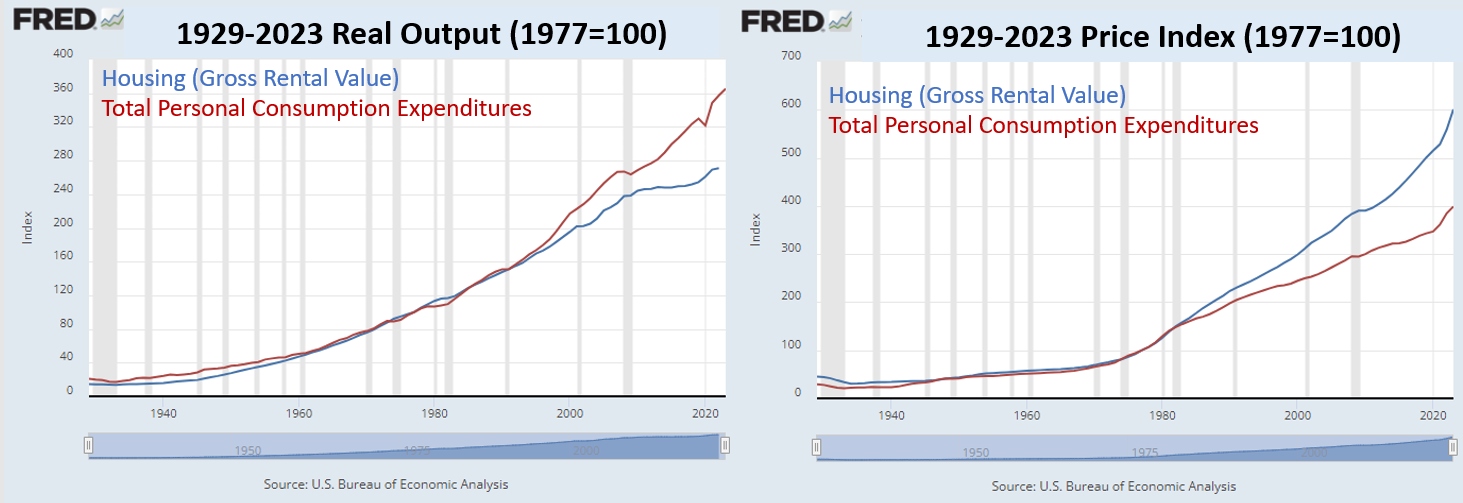

Furthermore, Homeowners are suppliers. Some of those subsidies are supply subsidies - GI Bill mortgages, FHA, Fannie and Freddie, the mortgage interest deduction, and the Community Reinvestment Act. They might tweak demand of purchasers a bit higher, but to the extent that they do, they are operating through their capacity as buyers. They increase price/rent ratios. Where supply is relatively elastic (everywhere for most of our history, almost everywhere until 2008, and almost nowhere since then) price is anchored to the cost of construction, and those programs lowered rents. The sustained, bipartisan effort to make housing more affordable was a success. As Figure 3 shows, Americans got more housing (left panel) and paid less for it (right panel) throughout the mid-20th century, during the first 4 decades of those programs.

Because the authors treat these supplier subsidies as if they are only demand subsidies, they have missed the most important change that happened with these programs. In 2008, 1/3 of the 20th century clientele of the government mortgage programs lost access to mortgage funding. And, since those supplier subsidies had been holding rents down, we have experienced unprecedented rent inflation and undersupply ever since. And, as noted above, it is highly regressive rent inflation.

We reversed the 20th century. Now we keep compromising our real consumption of housing more and more (Figure 4, left panel) and we are paying more and more for it (Figure 4, right panel). Much of this has been a result of sharply curtailing access to the mortgage programs the authors complain about.

Describing the American housing market in 2026 as “subsidizing demand and obstructing supply” is partially true, but it is mostly true because the sharp retraction of mortgage access through the FHA, Fannie, and Freddie is acting on the obstructing supply part of the equation.

You could argue that both sides of the scissors cut on supply and demand, and if you discount what I have written above, you could argue that under conditions of obstructed supply, any sources of demand stimulus still will be an important source of rising costs. In that case, expanding access to mortgage programs back to 20th century standards might just cause home prices to rise. There is some truth to that in the Closed Access cities. And, there is even some truth to that nationally right now because the curtailment of those programs permanently set back our capacity to build homes so much that we are still struggling to re-establish a national capacity to build a sustainable number of new homes. Under these conditions, more purchaser demand from broader mortgage access might not have an immediate effect on supply.

But, in an important way, even the standard “scissors” claim is wrong. In the Closed Access cities, there is a fixed supply of homes. Some 200,000 families will have to choose displacement this year. That doesn’t change if we get rid of the FHA. It doesn’t change if we get rid of Section 8 vouchers. Some 200,000 families will have to feel poor enough to give up living in their home cities this year. And the amount of stress it takes to get 200,000 families to move is not particularly sensitive to housing subsidy policies. Changing those policies might change who will feels poor enough to move. It might change the rent or price levels associated with 200,000 outmigrants. But, it won’t change the economic stress required to get 200,000 families to choose displacement. And, really, that stress, the cause of that stress, the regressive but shared reflection of that stress, and housing’s role in creating it, is the point the authors have failed to understand.

And, this problem - the particular conservative blind spot on the housing crisis - is actually the main source of the crisis. The retraction of lending access through federal over-regulation of mortgage lending and the tightening of underwriting at the federal agencies is what turned the regional housing crisis into a national housing crisis. That is what made Figure 2 for cities all over the country look like Figure 1 had looked for a few coastal problem cities.

The authors unwittingly support the policy choices that caused the crisis they are unable to see. We are missing 15 million homes or more, because of the sudden retraction of mortgage access.

That created an affordability crisis. Zoning reform would address the crisis - the crisis of poverty, the crisis of the first group of people, who just don’t have enough money. These authors have identified that reform, but aren’t quite able to see the full implications of it - only applying it to the couple making $400,000. The other reform that could help - broader mortgage access - isn’t on their radar because they think the solution is the problem.

By 2005, economically motivated migration from the housing-poor Closed Access cities became so heavy that the destinations of the movers couldn’t build enough homes to keep up. We didn’t have enough homes. The housing crisis in the Closed Access cities spread the symptoms of the housing shortage beyond the housing-poor regions. And from that housing-poor starting point, the retraction of credit access led to construction activity 6 years later that was still only 1/4 of what it had been in 2005 when the shortage had still just been regional. Twenty years later, construction is still catching up. One doesn’t have to squint at a chart of new home construction to imagine that the scale of the problem - 2 full decades now of recession-level housing construction - is worth identifying as a crisis.

Of course, the poorest among us are the most affected by this shortage, and the shortage makes them poorer. So, one might be tempted to observe that where the housing shortage has the most devastating effects, the problem is that those families are too poor.

If a lack of adequate housing is creating the poverty, how do we make that distinction? I think the framework the authors have laid out here is sort of unfalsifiable. What is the observable difference between a housing shortage that is causing poverty and an economy where some people lack housing because they are poor while families of means are being squeezed because housing is expensive? In a context where both ends of the spectrum are actually experiencing the consequences of the same housing shortage, what observation could falsify the rhetorical approach these authors are taking?

In a way, at an abstract level, they are making a Progressives redistribution argument. But you can’t redistribute your way out of a shortage. No amount of cash transfers can stop the outflow of families from New York, Los Angeles, San Francisco, and Boston. No amount of cash transfers can help 15 million households form if cities won’t permit new homes, and federal mortgage agencies won’t approve mortgages for the homes those households would need. Well, I suppose, some amount of cash transfers could substitute for mortgage access, but I doubt that the authors prefer an endgame of broadly socially distributed and funded housing. That would be an example of the sort of expensive over-reach that poorly targeted policies lead to, which they argue against.

In fact, the housing subsidies they note that are true demand subsidies, such as low-income housing tax credit & Section 8 vouchers, seem like examples of the public support they claim is appropriate for Americans whose problem is being poor. And, so, by failing to center the housing crisis as a cause of poverty, they are sort of arguing against themselves. Do they want cash transfers and redistribution to secure housing for “a destitute tail that is small and brutally squeezed” or is subsidizing demand the problem, as they suggest when they discuss housing subsidies? If households are destitute because of a housing crisis, these authors have unwittingly replaced a straightforward situation with a paradox. We can’t redistribute our way out of a supply crisis. They recognize that the redistributional policies in housing haven’t been working. They should take the next step and recognize that redistribution hasn’t been working because there is a supply crisis.

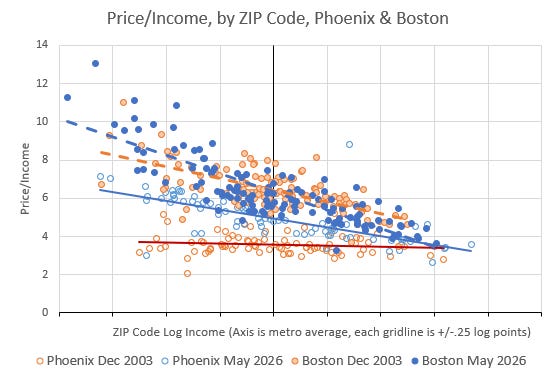

Figure 5 compares price/income ratios across Boston and across Phoenix in 2003 and 2026. Phoenix is an especially fast-growing market, so the supply crunch that followed the mortgage crackdown has especially led to price inflation there, making Phoenix look more like Boston.

Phoenix in 2003 only has group one - some poor residents who would need public support in any context. There wasn’t a stressed “talent class”, and housing was affordable throughout the Phoenix metro area. Homes sold for less than 4x neighborhood incomes across Phoenix. Those who needed help were families facing idiosyncratic needs with incomes well below the ZIP code averages shown here. Their first group (poor families who need help) existed, and always exists to some extent.

In Boston, the average household had to spend more than 6 years of income to buy a home. The richest Boston families had to make compromises (like longer commutes), but they still tended to spend about 4 years of income on their homes. The average Boston household spent more than 6 years of income because they were halfway between the poorest Boston households that lived in homes worth 10 years of income and the richest households that spent 4 years of income. In other words, the housing crisis was making everyone in Boston more like poor households. It was stealing years’ of income. The poorer they were, the more years the shortage took. Whole portions of the Boston population had to spend more on housing than the idiosyncratic households with very low incomes in Phoenix had to in 2003.

That’s one difference between a crisis and a non-crisis. The high cost in Boston in 2003 was systematic and universally felt. It was a product of living in city with a housing shortage. Now, 2 decades after the mortgage crackdown that these authors might think reduced the problem of subsidized demand (if they think about it at all), Phoenix looks similar to Boston. Most households in Phoenix now live in homes that claim a portion of their incomes that only the idiosyncratic poor households would have experienced in 2003.

Again, to look at Figure 5 and think this is a “talent class” problem, or, worse, to think it is a “talent class in Boston” problem, is untenable. That makes it easy to critique, I think, because this isn’t a conceptual problem. It’s empirical. These authors probably just don’t know about the trends in Figure 5. They have been failed by the economics academy.

This is a supply crisis. There would be no way to make housing affordable in either Phoenix or Boston by idiosyncratically targeting support to families who happen to have historically unusual, and frequently financially debilitating, housing costs. That policy would have applied to Phoenix in 2003. It doesn’t apply today.

The poorest American families need zoning reform and mortgage reform because we have an affordability crisis caused by a housing shortage. A housing crisis is creating poverty. We need, and will always need, some redistribution and public support. It will be difficult to relieve America’s affordability problem with redistribution and public support as long as we have a housing shortage that creates an affordability crisis.

There is one housing affordability crisis in the United States. At the two ends of the spectrum of that crisis, there are two groups in real trouble: a destitute tail that is small and brutally squeezed, and a much larger squeezed-talent class that is doing everything right but still cannot replicate its parents’ material life. The only Americans who are fine, or fine enough, or in the kinds of trouble we are not obligated to call a crisis, are families that owned homes before the crisis started, who have received unearned windfall gains on their inflated homes. The two groups need the same remedies, and the “There is no affordability crisis” framing makes that impossible to see.

Here is the figure for Detroit from 2002 to 2026. Much of the post-2008 price appreciation in cities like Detroit was just a return from very suppressed prices initially caused by the mortgage crackdown back up to replacement value. But, even with the depressive effect of the mortgage crackdown on low-tier prices in Midwest cities like Detroit after 2007, there has been more price inflation in poor neighborhoods than in rich neighborhoods over the whole period.

That last bit about the unearned windfalls is a big key here.

If I buy a house for $400k, I expect to pay roughly twice as much in property taxes as I would to buy a house for $200k.

But for a lot of these [expletives voluntarily redacted], they feel entitled to pay the exact same property tax on a house that doubled from $200k to $400k in the last 20 years.

I've written about "subsidizing demand" in regards to progressive housing policies. I don't think it's to blame for unaffordability but I do think it's regressive and distortionary.

It shouldn't hurt affordability because subsidy incidence works the same way as tax incidence. Maybe it raises prices but it shouldn't hurt affordability post-transfer (at least for the select subsidy recipients).

Subsidizing homeownership is clearly regressive and distortionary though. Property taxes are equally applied to rentals and owned homes. It's the multitude of other policies and untaxed imputed rent that are homeownership specific. Unless you're really low income, you don't get many handouts for renting but you get many for buying.