Shadows of Non-Filtering in Housing

I’m working on a new paper tracking aggregate real estate values over time, and I happened upon this curious nugget. This is a little bit of speculative analysis, but these little shadows of our hobbled housing market show up all over the place, if your personal Overton Window is positioned to see them.

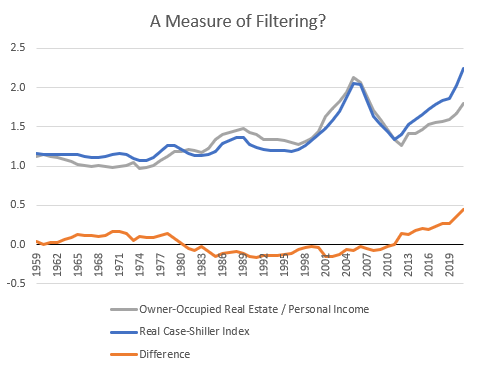

Figure 1 is a chart from 1959 to 2021. The gray line is the estimate of total owner-occupied real estate from the Fed, divided by total personal income estimated by the BEA. The blue line is the Case-Shiller price index, deflated with CPI. The orange line is the difference between the two.

These are fundamentally different measures. The aggregate value/aggregate income measure is the estimate at a point in time. Compositionally, it changes over time. We build new homes and we earn higher incomes over time. The Case-Shiller measure and the CPI attempt to track the real value of the existing housing stock over time, without compositional changes.

Over time, they track pretty well because the housing stock changes slowly, but also, housing tends to filter down when we build more. So, for instance, imagine that in a given year (with no inflation), the average income is $50,000 and the average home costs $100,000. The next year, the average income is $51,000 and the average home costs $102,000. What tends to happen is that a couple of families with high incomes build especially nice homes, move out of their old homes, and families with lower incomes move into them. So, if you tracked all of the homes that had cost $100,000 last year and were owned by families with $50,000 incomes, what you might find is that those homes still were worth $100,000 and their owners still had $50,000 incomes. But, they would be a slightly different group of owners, a little lower on the income distribution than the owners of those homes were last year.

So, when there is a natural growth in the marketplace, compositional changes should not cause these measures to diverge. In fact, when Robert Shiller deflates the Case-Shiller index with CPI inflation and says that home values should remain stable in real terms over the long term, he really implies that this sort of filtering happens. Incomes grow at more than the rate of inflation. So, the real Case-Shiller index, deflated by CPI inflation, would rise over time if the price/income remained stable over time and existing homes didn’t filter down through normal transactions as family incomes increased.

Or, to put it more generally and simply, Case-Shiller measures the changing value of existing homes, not new homes. If existing homes are getting relatively cheaper, Case-Shiller will decline relative to other measures. If existing homes are getting relatively more expensive, Case-Shiller will rise relative to other measures.

As you can see in Figure 2, Americans were building a lot of homes in the 1960s and 1970s. Real per capita housing expenditures (real rents) were rising. And, in Figure 1, Case-Shiller was declining relative to the estimate of all owned home values. Then, after 1980, relative housing expenditures slowed down a bit, and in Figure 1, Case-Shiller increased a bit. Existing homes were rising in value at a slightly faster pace than new homes were changing the composition of the housing stock.

Finally, after 2008, real housing expenditures per capita flatlined, and in Figure 1 there was a sharp divergence between the value of existing homes (deflated with general CPI) and the value of all homes (deflated with incomes).

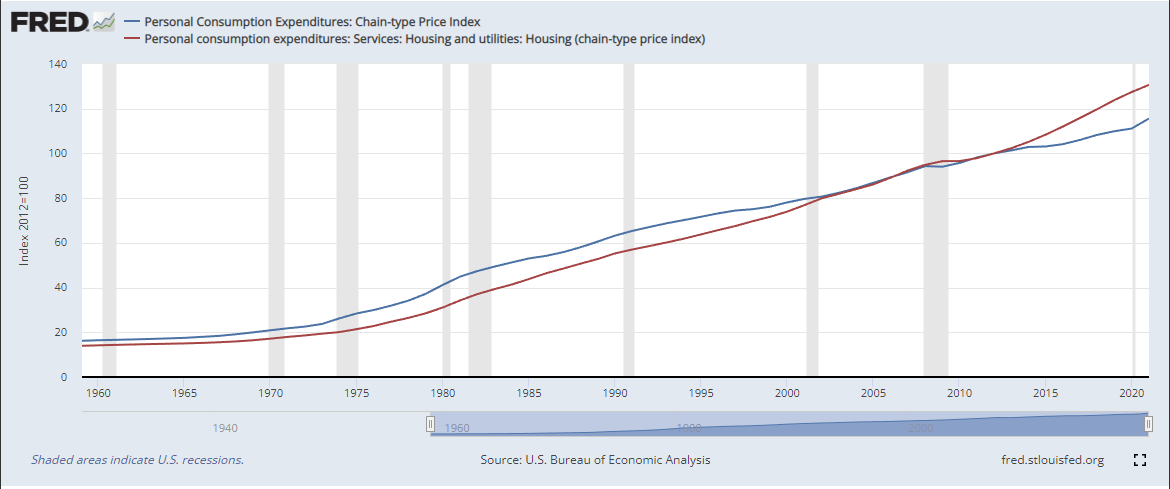

In Figure 3, you can see that rent inflation shot up relative to general inflation at the same time (shown here with PCE measures - housing in red and other prices in blue).

For 50 years, the relative difference between the Case-Shiller measure and the point-in-time measure for changing home values varied between +/-15% or so. Now it’s suddenly nearing 50%.

The literature measuring filtering directly takes years to construct because you have to track transactions of homes and owner incomes over decades. Recent research on the incomes of apartment tenants, which turn over faster, shows that filtering has reversed from norms, so that new tenants in a given apartment unit now have rising incomes over time. I think my recent work provides a measure that can give an indication of filtering in real time, even for owned homes.

In the meantime, these trends are so obscenely out of the norm that it doesn’t exactly take a magnifying glass to see what is happening. Raising interest rates or banning new neighborhoods built by private equity to rent isn’t going to bridge this gap. And a few hundred thousand extra apartments under construction isn’t going to reverse a decade or more of scarcity.

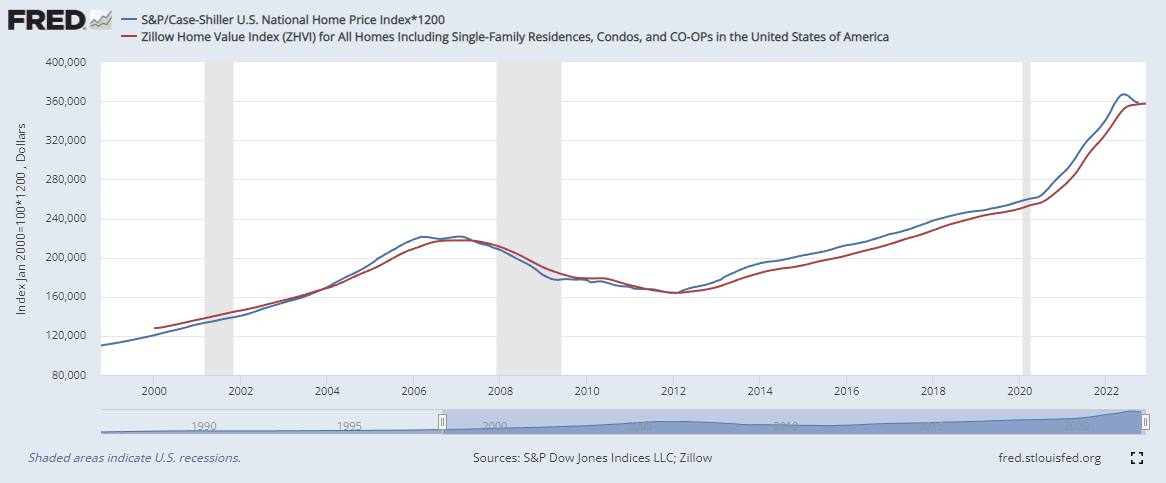

PS. Notice, in Figure 4, this divergence doesn’t show up between the Case-Shiller index and the Zillow ZHVI. The Zillow index is like the Federal Reserve measure of home values, in that it is a snapshot in time, changing in composition over time. But, Zillow is roughly a median measure while the Federal Reserve and Case-Shiller measures are value weighted. As readers of the EHT know, inadequate supply causes median home prices to rise more than high end home prices do. So, I suspect that there are countervailing forces here. The lack of filtering is moving the Case-Shiller value up because of the lack of changing composition from new homes and down because of the unbalanced effect of upward filtering on prices, roughly cancelling each other out.