Revisiting Boise

About a year ago, I took a look at Boise. It has been a popular topic in spite of its small size, because it was one of the western cities that seemed to have an especially large housing boom during the Covid period.

Frequently, Boise was identified in 2022 as being overvalued by 60-80%, though many analysts, such as Mark Zandi at Moody’s expected only about a 20% cyclical correction. My model helps to clarify the sources of that valuation deviation.

In the end, Boise dropped by about 15% before prices levelled out. Last year, my model identified about 20% of cyclical inflation in Boise. I suggested that there was no reason to, necessarily, expect a steep price decrease, because that cyclical correction could happen over a period of years, where prices could remain relatively flat while incomes grew to make up the difference. As it happened, the 20% cyclical price deviation was reversed in a year by the 15% price correction and 5% growth in incomes, give or take a percentage point or 2.

I have been arguing that the overvaluation has been related to building capacity and excess margins for the homebuilders. My commentary on Boise, suggesting that prices might not need to fall at all, was probably a bit aggressive. In this case, the cyclical price inflation was largely due to the capacity constraints of the builders. Backlogs were bloated and builders were raking in excess margins. This was not a stable equilibrium. It would be hard to maintain an overheated market that was just overheated enough to create a controlled stabilization in nominal home prices.

Ironically, the recent decline in home prices in places like Boise was due to the difference between the current market and the 2007 market. There was no reason for the steep national decline in prices then, and there is no reason for a steep national decline in prices now. But there was some reason for the recent correction back to normal homebuilder margins. The 15% decline in Boise prices was related to the unusual capacity condition of the homebuilders in 2022. New home prices were elevated roughly 15% because of that. And now much of that has reversed, a bit more in some places like Boise than in others.

My model did predict the scale of the correction.

Figure 2 shows the Erdmann Housing Tracker estimates for Boise. There have been some revisions to this since last year. Some of the difference is due to updates in ZIP code incomes. They are reported with a lag of a couple of years, and recent months must be estimated from previous trends. So, there are minor changes when the IRS reports updated annual average incomes by ZIP code. Also, at the start of 2023, Zillow implemented an update on their methodology, in their ongoing work to make their estimates as accurate as possible. Those changes seem to have taken a bit of the edge off of price estimates in 2021.

But, all in all, as of mid-2022, the tracker had an estimated cyclical inflation of just over 20%, and with the updated numbers the estimate in mid-2022 is just under 20%. With the price correction over the course of late 2022 and early 2023, the tracker cyclical estimate has slid right into a new normal at a nearly neutral spot. There is no more cyclical correction to look out for. Of course, it is always possible to create a cyclical decline. But it would be unnecessary. All further sustainable declines in Boise home prices will need to be associated with a building boom that brings down rents.

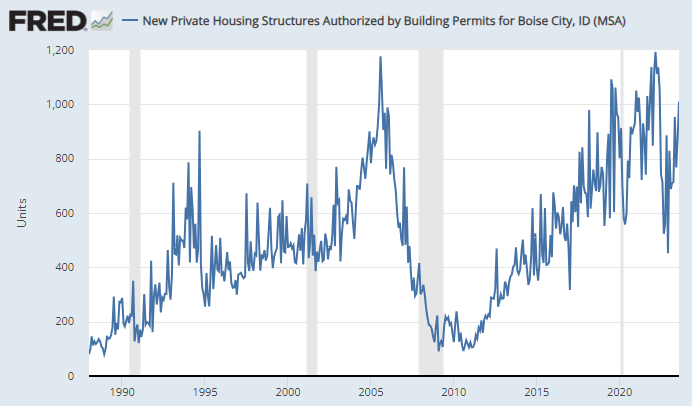

In late 2022, it looked like the building boom might fizzle in Boise. Fortunately, it has returned in 2023. In August, new permits were issued at a pace moving back near the highs of early 2022.

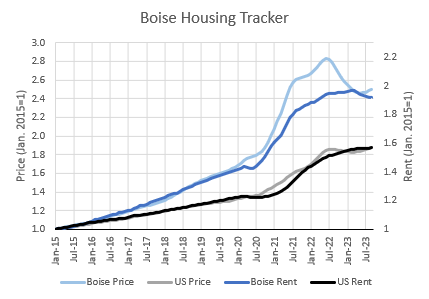

Finally, in Figure 4, I compare rents and prices in Boise and the US. The implied price/rent ratio is higher in Boise than in the US, which can be for a number of reasons, such as property tax rates, expected future rent and inflation trends, etc. Here, I have indexed them all to 1 in January 2015.

When rents are rising excessively, prices rise at more than a 1:1 ratio. This means that rising rents lead to rising price/rent ratios, and this is a big source of confusion that has been embedded in much of the academic and lay literature about housing. In the US, I have argued that when prices and rents are aligned from 2015 to 2019, the subsequent changes are also aligned, as in Figure 4. When rents spiked, so did prices, at the same proportion they had been since 2015. And, with just a couple of small deviations, they have ended up at similarly levels in 2023.

Figure 4 shows that Boise rents have increased at a faster pace than US rents. Boise prices have increased at a faster pace than US prices. And both of them have increased at the same proportional faster pace. Boise prices did diverge more from rents in 2022. The 15% relative decline in Boise prices has brought it back down to the Boise rent trend - shown in the blue lines in Figure 4.

To reverse prices from here, both in the US and in Boise, we need a building boom that will slowly moderate rents over the course of years.

Kevin, your deep dive into Boise’s housing market is incredibly insightful! It's fascinating to see how the dynamics of supply and demand, especially in the context of a post-Covid world, have shaped this vibrant city. Your observations about the cyclical corrections and the relationship between rents and prices really highlight the complexities of the market.

Boise, ID has always intrigued me, not just for its real estate trends but also for its community spirit. I recently came across wpwebdesignboise.com, a web design company in Boise, ID that beautifully reflects how local businesses are adapting and thriving in this evolving landscape. It’s a testament to the resilience of Boise’s economy, showcasing the creativity and determination of its residents.

As we navigate these changes, it’s encouraging to see new building permits on the rise again.