RealPage, Collusion, and Rents

There was a Propublica exposé on RealPage, which produces software and consulting services for property managers. Following that exposé , some states have filed lawsuits against RealPage charging collusion.

RealPage aims to help landlords set rents to maximize earnings. Reasonable enough. The claim is that when RealPage can gain enough market share in an area, they can strong-arm landlords into setting rents based on their inside information, and so the pricing ends up basically being monopolistic.

Sophisticated defenders of the lawsuits point out ways in which this technically meets the definition of collusion. I’m not a legal expert on the definition of and limits to collusion, so I don’t have an opinion on the case. I think the logical claim seems reasonable. It could reach a level of information sharing and price cooperation that could meet the technical definition of collusion. And, it is also possible that the laws are written in such a way that it could be legally guilty of collusion without actually being collusion in any important economic sense. The company claims that using their service raises landlords’ net income by a few percentage points.

How does this work?

I’m not sure any RealPage critics have actually tried to think through how such collusion could make much difference. I have tried to, and I can’t quite figure out what the end game would be.

Let’s say that in a city, there are 100,000 apartments with average rent of $1,000, and 4,000 vacancies. And, let’s say that, as it stands, in 3 years, there will be 110,000 apartments, renting for $1,000, and 4,400 vacancies. 10,000 extra units and 400 extra vacancies, at the same rent level (just to keep it simple).

OK. So, now, the software comes to town. So, the idea is that this software systematically allows landlords to engage in monopolistic pricing by raising rents and accepting higher vacancies. (Withholding extra vacant units is central to the claims. See the Arizona Attorney General here.)

Now, there are 100,000 apartments with average rent of $1,050, and 5,000 vacancies. That means that the landlords have increased their revenues by 4% (which is in the range that I think RealPage claims).

They were making $96 million [(100,000-4,000) x $1,000].

Now they make $99.75 million [(100,000-5,000) x $1,050].

How will it look in 3 years? Well, if this is an ongoing strategy and there is no effect on new construction, then, in 3 years:

They were set to make $1.056 million with 4,400 vacant units.

Now, they will make $1.097 million with 5,500 vacant units. Still 4% more.

If this is how it goes, on into the future, why are all the landlords still building all the extra 10,000 units if they are just keeping 100 of them purposefully empty? Why not just build 9,900 units and pocket the savings?

This is not how a monopoly works. A monopoly doesn’t set the price at a lower quantity level but still produce the original quantity. Yet, the slack is definitely part of the narrative of how the critics think this works.

Furthermore, if revenues are boosted 4%, why wouldn’t that induce more construction? Why wouldn’t that lead to 11,000 new units instead of 10,000 new units? Even skeptics of the supply shortage generally think that developers produce more units when they can gain more profits. And, as far as I know, none of the RealPage critics claims that landlords have a lock on new entrants.

So, I assume that the RealPage critics imagine a market where there is just always an additional 1% slack in the stock of apartments. I guess?

If this software does lead to systematically higher vacancy rates, in 3 years, there are 110,000 units renting at $1,050. Since the market clearing rent was $1,000, presumably there would be some developer who would be willing to build more apartments, until the rents declined to $1,000. Or, at least that would be the lower bound.

(By the way, it’s sort of funny in the video of the Arizona AG, how all the b-roll shots are full of cranes building high rise apartment buildings. It’s kind of weird, really, that the video visuals focus on new construction.)

It seems like the market would end up somewhere close to the original rent price, but all the landlords using the software would just end up with extra slack. And, this is where I run into trouble, because that sounds like an equilibrium where landlords are actually making less profit than they were before, and I can’t imagine how it ends up in any other scenario.

I suspect the obvious answer is that, on average, over time, the software doesn’t actually lead to persistent systematic higher vacancy rates. Sometimes it does and sometimes it doesn’t.

Building a Narrative

You can see the morality play coalescing as the RealPage anti-narrative builds by choosing outlier stories, mixing concepts, and accumulating motivated rhetoric.

The ProPublica piece from October 2022 has the broadly stated title, “Rent Going Up? One Company’s Algorithm Could Be Why.” The article describes several, somewhat unrelated, characteristics of the software.

Several times, the article notes how its recommendations are ruthless, with no empathy for tenants. This is an important factor in the narrative building. Really, there is no other way it can go. Of course, an algorithm is going to tend to press for more turnover than a human manager is, both because the manager prefers not to have to deal with turnover and also because they may empathize the the tenants who have to deal with moving. Mainly, what this serves to do in the final narrative is to establish the corporation and the software as “the other” - as not-human. To actually remove our empathy for them. Assume the worst intentions. Apply attribution error without reservation. (Their lack of empathy leads to setting rent because of math instead of empathy. Then, our lack of empathy toward systems that use math to set rents leads to our shared willingness to exaggerate the effect of the software.)

Sometimes the software recommends holding more vacancies to hold out for higher rents.

In some locations, it has very high market penetration and comprehensive market information.

There is an anecdote of a tenant whose landlord (who used the software) tried to raise their rent. The tenant wasn’t able to convince them to forgo the increase, but they were able to rent another unit in the same building for less. This suggests that the software clients were being very aggressive with existing tenants.

The article does note some limitations on the software’s effect. In this anecdote, the article suggests that the software was imperfect, and some rent hikes wouldn’t have been revenue enhancing.

Nicole Lott said that when the building where she worked as a property manager near Dallas started using YieldStar, the software determined that similar buildings in the area were charging more. It pushed for steep increases.

“It really jumped rates up,” Lott said. “Leasing slowed down to a crawl.”

She and other staff challenged the software, asking the division of her company that oversaw YieldStar for a review, she said. The landlord ended up raising rates more gradually, she said.

“We didn’t think we could get those rates,” she said. “In some cases we were right and in some cases we might have been wrong.”

And, the article is meant to establish the software as a cause of rising rents, but in the end, it acknowledges that it, at most, adds a few percentage points of additional profits for its client landlords:

What role RealPage’s software has played in soaring rents — which in the decade before the pandemic nearly doubled in some cities — is hard to discern. Inadequate new construction and the tight market for homebuyers have exacerbated an existing housing shortage.

But by RealPage’s own admission, its algorithm is helping drive rents higher.

“Find out how YieldStar can help you outperform the market 3% to 7%,” RealPage urges potential clients on its website.

Few tenants know that such software, owned by a privately held company, has had a hand in rent increases across the country.

The article then describes the rental situation in Seattle. Rents have risen more there than just about anywhere, and many landlords use the software there. The article compares a RealPage client that raised rent on a couple by 33%. The couple moved 10 minutes away to find more affordable housing.

Another building that isn’t a client kept rents lower. The article then notes that Seattle has been especially tough for renters. And, it notes that many “people with higher incomes often ‘down rented,’ choosing cheaper apartments that would otherwise have been available to people making less. Seattle should have had a surplus of 9,000 apartments affordable to people making 80% or less of the median income, the study found. But tenants’ down renting as prices rose turned that surplus into a deficit of 21,000.”

Now, again, let’s think this through. Facing higher rents, 30,000 units that might have otherwise been “affordable” were claimed by tenants “down renting” to get by - much like the couple that faced the 33% increase. The high rents induced them to reduce the housing they were consuming. Were RealPage landlords just leaving 30,000 units empty? (To be clear, this article doesn’t claim they were.) Presumably, those units were claimed by new tenants paying the higher rents.

So, how was it going to help the aggregate situation if every building kept rents low like the non-RealPage building did? In effect, the existing tenants would have been subsidized by generous landlords. They would have stayed in larger, better appointed apartments as a result, and the net effect would have been less housing in Seattle for everyone else.

If these apartments had all kept rents below the market-clearing rate, do you think Seattle would still have had that surplus of 9,000 “affordable” apartments instead of a deficit? Show your work.

Accelerating A Narrative

Earlier this year a video by a group called “A More Perfect Union” highlighted several lawsuits against RealPage. The video waves off the claim that supply and demand are responsible for any of the rent inflation. The Arizona Attorney General, who is pushing one of these lawsuits, explicitly makes that assertion, calling supply-side explanations “bunk”.

And, more recently, The American Prospect, has published an article that fully discards any limits to scale that were in the Propublica article. “By now, you have probably heard of Yieldstar, the private equity–owned software that numerous plaintiff’s attorneys, tenant advocates, and state attorneys general say is actually a front for a sprawling nationwide cartel that fixes rent prices to ludicrous heights and has caused the cost of an apartment to surge between 50 and 80 percent over the past seven years in several of the markets where the software is employed.”

This is laughable. This is like claiming that you could lasso the moon. Vacancy rates across the country are in the single digits. For landlords to be able to collude to raise rents 50% to 80%, they would need to hold tens of millions of units off the market to raise rents that much. I estimate a nationwide shortage of something like 20 million units, and, yes, if we had those units, it might reverse 50% to 80% of rent inflation. We don’t have the units.

These claims are so outrageous and so explicit, that it is clear that their authors are simply incurious about what they are asserting. They don’t have a misconception. They simply aren’t conceiving anything. Just like with the mythological supply glut in the 2000s, there is nothing to debunk. The purveyors aren’t concerned with the facts that they imply. There are no studies to try to replicate.

And I think the Prospect article is interesting. If you can see how it is ridiculous, it is an interesting study in rhetoric. It is a collection of anecdotes and an odd mix of various financial actors engaged in various forms of greed, power, bad faith, and irrationality. If you weren’t inclined to be curious about the ridiculous foundation that purports to make all those anecdotes important, then I am sure that they appear to add up to a striking and noteworthy story.

Oddly the article is mostly about property owners failing because they overpaid for buildings based on inflated rent expectations. Everyone is losing. Even the building owners. And it’s all because of the software!

Rents went up across the country because landlords got together and just flexed there muscles, and with no other change in supply and demand, they pushed up rents 50% just by insisting. There are two types of people in the world. Those that think that assertion requires striking, earth shattering, detailed connecting evidence. And those that don’t really need any.

If your reaction is, “Kevin just doesn’t get it. I know landlords who jacked up rents after they started using RealPage.” You’re still focusing on the insufficient one-two facts. They may seem compelling. They are not. They are not definitive evidence. Nobody denies any of those facts. I am just insisting that you have to work through the macro-level implications to make the claims about these activities that are commonly being made.

The same thing applies to so many claims about what caused home prices to rise up through 2005. “You don’t get it. I knew brokers making ridiculous mortgages. I knew bankers taking ridiculous risks on CDOs.” Invariably, the bad behavior happened in 2006. But, as with the articles about RealPage, details about timing, causality, and plausibility have long since been left in the wake of the narrative.

To me, what is most interesting about the Prospect article is how much it reminds me of almost every book I have read about the financial crisis. This is how popular non-fiction works. This is how conventional wisdom develops. This is a pattern. And, it’s not a robust method for understanding the world and making it better. This is moral panic non-fiction.

Market critics may not repeat themselves, but they frequently rhyme

In the parallel world of narrative building, I would place the Propublica article around 2005 and the American Prospect article around 2007 or 2008.

Back then, the bad guys weren’t apartment consultants. They were mortgage lenders. The conventional wisdom is centered around a set of technically unassailable facts, clearly true observations, and various anecdotes, just like the RealPage articles are. Loose credit can boost consumption or investment. Banks that are undercapitalized are riskier. When outcomes don’t match the assumptions of models underlying financial securities, investors take losses. Some people made investments with unrealistic expectations.

All those true things get bundled up into a package of easily digestible culprits about what caused the crisis. In fact, those culprits had already widely been blamed for the crisis that would happen even before any crisis was coming. So, when the crisis did happen, it served as confirmation about the culprits that everyone had, ready to pull out of their pockets.

And, since it confirmed preset culprits, there really was very little effort into confirming the details. So, we basically have a truism (When there is a financial disruption, the riskiest players lose the most.) and a factual observation (There had been an increase in activity in some financial securities with unusually risky elements.) and the actual nuts and bolts of the ensuing events are presumed rather than established.

That combination was so compelling that it required no factual confirmation to become canonized as an explanation for the financial crisis. I mean that literally. There are important parts of the canon that nobody looked into, like the notion that housing construction had gotten ahead of demand, necessitating a period of deep decline in housing starts. A lot of big claims about that were made by important people at important moments. Nobody looked closely at the claim. There is one rudimentary paper from the New York Fed that tries to quantify boom era supply.

As far as I know, my Mercatus paper on the subject is the most sophisticated attempt at quantifying the role of housing supply leading up to the Great Recession. I’m not saying my paper is sophisticated at all. My paper is, at best, Master’s level work. It’s just all there is on the topic because literally nobody actually bothered to do sophisticated analysis on possibly the most important economic question of the last 30 years.

The financial explanation was prepackaged. More subtle and broadly curious explanations were too unpopular to even consider.

And so, the financial explanation became the gas of the financial crisis. It was real. It was true. And it fills up any explanatory container you need it to.

The entire narrative becomes a product of us-vs-them thinking. Attribution error. Every outcome is the result of the greed of financial actors. That is axiomatic. From that axiom, what can we deduce?

From 2005 to 2008, the narrative went:

Some mortgage originators are being sloppy or predatory.

Predatory mortgages are the reason for rising home prices.

Predatory mortgage lenders are getting more desperate for new business. They started creating dangerous new financial securities to try to make their underwriting malfeasance less transparent.

Borrowers were bound to default.

Declining home prices must be due to overstretched borrowers.

Home prices will need to decline enough to chasten the reckless lenders.

The wave of failing financial firms is the natural comeuppance for firms whose greed left them holding the bag when their collective scheme collapsed.

This starts with an accurate observation and a truism. Some lenders are more reckless than others, and this is a time where there are more reckless lenders. And, then the rest of the list is littered with overstatement, inaccuracies, misplaced fatalism, and Schadenfreude.

The one overriding feature of this narrative is the antagonist. Originating mortgages with high fees to less qualified borrowers in 2005 didn’t cause the net domestic migration of millions of the poorest residents out of our most expensive and most housing-deprived cities, year after year, for decades. It doesn’t really even have anything to do with bankers slicing and dicing existing securities in 2007 to sell derivatives that happen to be benchmarked to the payments on some mortgages. The only thing that draws all the various parts of the story together is the financial devil at the center, placed there by the narrator.

The books about the period, like “All the Devils Are Here” are like medieval literature touring the ironic punishments of hell. After detailing all the supposed ways that Wall Street insiders took advantage of us, “All the Devils Are Here” notes;

What’s remarkable, in hindsight, is that despite their many advantages, so many Wall Street firms, blinded by the rich fees and huge bonuses the CDO machine made possible, duped themselves as well. As one close observer says, “There was plenty of dumb smart money.”

The story is about a pit of vipers, and eventually they turn on themselves.

The American Prospect article is fully in that end-game mode. Most of the article is about how landlords and their bankers convinced themselves that this new software was their road to riches, and now, as a result of their hubris, they are all taking losses. The software could single-handedly raise rents 50%-80% across the country, but every scheme has its limit, and now the vipers are turning on themselves.

The American Prospect article links to another article that is a collection of failed projects and malfeasance, and I’m not even sure how to analyze these articles. It’s just a collection of outlier anecdotes. It’s such a pure form of prejudicial narrative building, there isn’t an actual foundation of logic underneath it to critique. In the articles, there are bankrupt properties, going unmaintained, with very high vacancy rates, and sometimes purveyors who may have mishandled investor money or overcharged tenants. The RealPage software is somehow the central figure in the same way that the mortgage lender was the central figure in stories back in 2007 of the working class homeowner who couldn’t take care of their ailing parents and afford the cost of their home in suburban LA.

When you get far enough down the path of pure attribution error, you end up with a very compelling narrative that doesn’t actually have any connective tissue.

My main point here is to hope that if you can see this in the American Prospect articles, to reach back and see the parallels in the literature and news of 2008.

As Tyler Cowen warns, “bad guy” narratives lower our IQ. In a narrative without vipers, it might be easy to imagine that borrowing rates jumping from 3% to 7% in short order, inflation going from 2% to 10% and back to 2% in short order, supply chains for new buildings got gummed up for years, and a million and a half Americans dying in a pandemic, might lead to a rough couple of years for some subset of property owners.

Could all that be the cause of some challenges in the apartment space, and maybe even desperate moves from some shady characters? Or is it the software?

Likewise in 2008, in a viper-less narrative, might there have been a few important things going on that would have caused us to think differently about the hardships that were coming down on us?

Revisiting 2008

Every educated person in this country has read versions of that Prospect article, applied to the financial crisis. Loaded, motivated stories of greed and recklessness, and they think they are educated on causality. The main obstacle to a broad understanding of the crisis and the damage we have been doing to ourselves ever since requires so much difficult unlearning that would have to happen. Unlearning is so much harder than learning.

The biases of the viper narrative seeped deeply even into the academy. This happens in countless ways, in practice. One way is that papers that attempt to quantify the economic of loose lending on the boom and bust control away 80% of the data.

Then, they’ll find that of the remaining 20%, things like credit access explain a few percentage points. And, then, the implication is, if it explains that much of the 20%, imagine how important it was to the 100%.

I wrote a paper where I didn’t control away 80% of the data. I actually found a larger role for credit access than the conventional literature does, but I also find that the factors lurking in the 80% far outweigh the importance of credit access. And, then, conventional critics will say that I’m “wrong to think that finance wasn’t involved”. When the library is full of books about vipers, and you see a book that only has a chapter about vipers, it will naturally feel like this author’s trying to avoid writing about vipers.

Here I will revisit how my paper compares to the existing literature to highlight the scale at which this observer’s bias strangled academic investigations into the 2008 crisis. I will compare my findings to the findings from a paper that was published in the Journal of Financial Economics in 2021, “What Drove the 2003-2006 House Price Boom and Subsequent Collapse? Disentangling Competing Explanations”, by John M. Griffin, Samuel Kruger, and Gonzalo Maturana. Their paper follows the typical approach.

The abstract begins:

Ten years after the financial crisis, competing and often contradictory narratives have arisen around the central question of what can explain the massive rise and fall in house prices around the crisis. We provide a unified framework and use detailed cross-sectional data to examine four variants of the excess credit supply channel and three variants of the speculation channel that have been proposed in the literature.

That’s it. Four variables about excess credit. Three variables about speculation. Those are the light posts under which we will be looking for our proverbial keys. Could there be other causes of the boom and bust?

In regressions of their variables against price changes, they found two that were statistically associated with both the rise and fall of home prices in a given ZIP code - the market share of subprime lending and the prevalence of lenders who misreported second liens (as a proxy for reckless lending). The subprime lending variable comes from Mian and Sufi’s work and the lender variable comes from the authors’ own work.

In ZIP codes with one-standard deviation more subprime or reckless lending, home prices rose just under 3% from 2002 to 2006 and declined almost 4% more from 2006 to 2010. From this they report at the end of the abstract, “Overall, our findings suggest that excess credit supply, particularly through subprime and dubious mortgage origination, stimulated housing demand and played a large role in the crisis.”

They controlled for the differences between cities, income levels, etc. The R2 on their individual regressions for all variables for 2002 to 2006 - both the statistically significant ones and the weak ones - ranges from 0.844 to 0.847 and for 2006 to 2010 it ranged from 0.802 to 0.826. In other words, they controlled away 80% of what had happened.

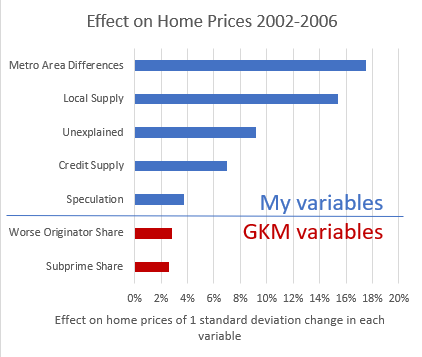

To give a visual sense of scale, in Figure 1, I show the (Zillow) national median home price from 2000 to 2024 (deflated with per capita income). Then, I show the trend in median home prices for metro areas 1 standard deviation above average and 1 standard deviation below average. In other words, a relatively cheap and relatively expensive city.

GKM only look at differences within cities. So, in Figure 1, I have added the effects of their most important variables in 2006 and 2010 for both the expensive city and the cheaper city.

The average home in the expensive city topped out in 2006 about 65% above its price in 2000. According to GKM, ZIP codes within that city with less or more subprime and reckless lending increased by 62% or 68% instead.

In the less expensive city, homes increased by 3% or 9%, depending on credit conditions.

The difference in scale between what was seen (because we bothered to look) and what was unseen was massive.

Within each metro area’s housing market, I have found a peculiar pattern in home prices that differentiates between the effects of endemic inadequate supply and short term changes in demand. So, I can extract information from all that “unseen” about what causes home prices to change.

Figure 2 compares the scale of various factors that I found from 2002 to 2006 to the 2 strongest variables that GKM found.

MKG conclude that their variables “played a large role in the crisis”. That’s the extent of their discussion.

I describe the effect of my variables from most to least important. The metro-area differences, by the way, are largely associated with migration surges of families leaving housing-deprived cities and adding demand for housing in other cities. Eventually, in my conclusions, I get to credit supply and speculation.

One additional kick-in-the-gut irony is from the 2006 to 2010 period: GKM conclude that the statistical significance and the scale of their 2 most important variables during that period (the little squiggles around each metro area in Figure 1 in 2010) prove that they were key to the boom and bust. What goes up must come down, and those variables were important in both directions.

Valuations in the cheaper (blue) city increased 4% and then declined by 40%. They controlled for that. In other words, they removed that 40% collapse from what had been relatively neutral valuations from the basket of observations that they considered important. The important thing was the 4% effect of subprime and reckless lending.

In the paper where they established the importance of their reckless lending “worst originator” variable, Griffin and Maturana took note of the fact that in cities that didn’t have a shortage of housing, reckless lending wasn’t associated with rising prices in the boom, but was associated with collapsing prices in the bust. In other words, they noticed that the blue line in Figure 1 wasn’t symmetrical. There was only a bust, not a bubble. Their conclusion was:

In summary, the fact that a high concentration of the worse originators is related to house price crashes in areas of elastic land supply indicates that the relation between dubious origination and crashes is not due to the worse originators solely concentrating in areas of tight land supply. The increase in credit in areas of elastic supply seemingly led to unwarranted housing construction and a subsequent crash of house prices. While each test above may not accomplish identification in its purest form, it seems extremely difficult to construct a coherent alternative explanation that is consistent with all the previous results.

The reason they said “seemingly”, as I mentioned above, is because nobody bothered to check on housing construction. And, in fact, when I did check, what I found was that there isn’t a single stinking city in this country in the last 30 years where anything remotely resembling “unwarranted housing construction” happened that could have caused a 5% price correction, let alone 40%.

To summarize, according to GKM: The 4% drop associated with reckless lending “played a large role in the crisis”. The 40% drop in cities that weren’t even expensive? They’re sure if we looked, we’d find a standard explanation.

I think I may be being too hard on American Prospect, because America’s top economists, vetted by its top reviewers, and published in a top journal, thought it made sense to just intuit that in the physical world we live in of 2x4s, concrete, and gypsum board, every city in the country pulled enough of that into shelter in just a couple of years to lower the aggregate value of all real estate by 40% or more.

Maybe RealPage could single-handedly increase rents by 80%. Hell, maybe I could go out on my porch and blow a song on my kazoo and cause the universe to implode. I haven’t checked the math, but the intuition checks out.

To the average educated person, GKM’s findings seem reasonable, their conclusions seem to follow, and after all, we’ve all read the libraries full of books about the vipers. Since the vipers and their various activities would generally fall under my 4th and 5th categories, in order of importance, any educated person will think I am mostly just ignoring what happened. There was no literature available to be educated in any other way to have any other reaction.

So, to the educated, the blue bars in Figure 2 appear to represent the less comprehensive conclusion. The blue bars are the results that stubbornly ignore what everyone knows happened.

Whacking Day - The Policy Response to Vipers

The response to the observer’s bias in 2008 was disastrous, of course. On net, generous mortgage lending creates a lot of positive externalities, and so cutting them off as much as we did was really bad.

The policy response here would be to break up RealPage or somehow make information aggregation illegal for landlords. It doesn’t amount to much, and its absence won’t amount to much either.

The big worry I have these days is that these backlashes push further. It is already a populist point-scorer to call for getting Wall Street investors out of single family housing. I don’t think that will lead to a crash like we had in 2008. It will just prevent the one last chance we have of escaping the never-ending grind that is bankrupting working class tenants and filling our parks with tents.

That’s almost worse, because the human suffering associated with it will be worse - more basic - than the financial stresses we imposed on homeowners after 2008. But, it won’t create a “big event” that will have everyone talking. Every day, people will just be giving up on a decent life, struggling to get by, and dying. Out in the shadows. Or, in Phoenix, more accurately, in the sun.

The RealPage stuff doesn’t really worry me. But, I wouldn’t have been worried by the various sources of focus in 2005 or 2006 either. It’s the snow-ball effect that gets you. By 2008, when we were communally engaged in financial self-flagellation, the avalanche was too strong to stop. I’m afraid the RealPage backlash is just one more prong in the pitchfork when the masses come for the vipers again. In 2026, when the completion of 300,000 new build-to-rent homes triggers the angry mob, “Remember the rent algorithm” will be on their battle flags.

PS. Today, Christian Britschgi at Reason.com has a nice rundown of the RealPage topic. It includes discussion of this paper written in 2023 that quantifies the effects. They find, generally, that it improves price discovery, which means that rents decline more when demand is weakening and rise more when demand is rising.

I think this falls in the larger category of “Closed Access makes all good things bad”. Closed Access makes good jobs, immigration, local amenities, and many other things “bad”. Add one more thing to the list: Closed Access makes price discovery bad.

Of course, I largely agree with this post.

But there is also a market argument that the Realpage would not be able to successfully sell product unless it worked.

But, as usual, the real solution is about 10 or 20 million more housing units in the US.

BTW, 10 million units at $500k each is $5 trillion.

Sounds like a big number, but US GDP in 2023 was $27.4 trillion.

The government spends $1.4 trillion a year on DoD, VA and pro-rated interest on the national debt.

Moreover, the private sector would build the housing, if allowed.

I'm confused as to why a landlord would have to buy a software service like RealPage when a few minutes of searching on the internet can yield good data on market rents for a particular geographic location. A multifamily property owner in a competitive market has a compelling incentive to keep occupancy rates as high as possible for as long as possible. They have to be tactical about how much they jack up monthly rents, and in this respect I think there's a larger story about how large unit buildings will command higher rents than small unit buildings.