Random notes

yield curve, rental vacancies, and price trends

Just a few visuals here that I think are interesting.

Yield Curve

First, let’s compare changes in the yield curve before Covid and since Covid in Figure 1. The labels are the date of the curve. The x-axis is the future date that each point on the curve corresponds to. On August 17, 2021, a contract to lend money immediately paid about 1.3% and a promise to lend money in the future in June 2027 would pay 2.8%.

I was on recession watch before Covid. I had a large long position in bonds, which was doing pretty well and then did really well when Covid came. I am not sure what would have happened if Covid hadn’t come. I think JPow was doing as well as any recent Fed Chair at lowering the target rate just fast enough to avoid recession. I don’t know where it would have ended up. But, in the meantime, it was a pretty standard monetary cycle. If we have to use rate targets to describe monetary policy, then, the target rate was raised a bit too much, slowing the economy and lowering long term rates, and the Fed followed those rates back down, but not fast enough to stabilize them.

After Covid, that yield curve in March 2022 is interesting. The curve was lower and flatter than the yield curve had been in June 2018. Yet, inflation in 2018 was about 2.5%, and inflation in March 2022 was 8.5%. By July (the next blue curve shown in the right panel after March), inflation was broken. Inflation (excluding shelter, of course) from June to July was around the 2% target, and it has remained that way since. And it is during the time that inflation subsided that long term rates (real rates) have moved to such highs. I have argued that rates aren’t high now because of Fed tightening. They are high because the Fed was blessedly patient and didn’t try to reverse inflation that ended up declining on its own.

One difference between these periods is that the slope of the curve has been much more volatile recently (Figure 2). Before Covid, there was a classic inversion. The Fed almost broke out of the inversion enough in 2019 to make me regret my bond position, but by the time Covid came, things were looking relatively recessionary again.

Since Covid, the slope has been all over the place. It steepened in the summer of 2022 when inflation had its last gasps, and it’s been up and down like a yo-yo since then. You can see, in the last couple of weeks it kicked way up and then snapped back down, though it is still relatively steep.

By the way, I think we are in an unusual period now. I’m the biggest fan of the inverted (downward sloping) yield curve recession indicator. But, someone using a broad indicator like the 10-year yield vs. the 3-month yield is missing a lot of nuance in this context. You really have to view the whole curve and get a sense of it.

Long-term rates have been all over the place (the right end of the chart). I’m not sure exactly what that means for the Fed target rate. I think we are way past time to move it back down to 4% or so. But, my terminal rate target keeps moving up, and I have learned to expect great things from JPow. Maybe the terminal rate will end up at 5%. That would be funny. And fantastic! Because it would be associated with an economic boomtime. But, if the curve starts to flatten and drop before we get there, I hope JPow is ready to move. I don’t want to have to buy bonds again.

Home Price Appreciation Over Time

It’s been a while since I checked in on average and variance of home price appreciation across metro areas. Figure 3 is the unweighted average of the approx. 50 largest metro areas.

Comments:

Before 2008, it was true, on average, that homes never lose value. But, it was also true almost all the time that a decent number of homes at any given time were. After the end of the post-2007 crash, for a decade, it actually did become true that home prices didn’t really lose value anywhere.

I would argue that you can see in this chart the phases of the 2000s bust that my model highlights. In 2005, average price appreciation was high, but it was also highly varied regionally. Some cities were going gangbusters while others were pretty normal. In 2006 and 2007, price appreciation moderated. So did the variance. Every market was moderating. That was fine. But, by 2008, we had crossed the Rubicon, and as the average price change dove below zero, variance between cities kicked way up. Then, when it was all over, regional differences became unimportant for the next decade, kicking back up a little bit with the Covid mini-boom and correction.

Look at 2011. There’s a period there - 5 God forsaken years after housing starts had steeply collapsed - where home prices changes were negative in every single major metro area. That’s about when Bernanke was excusing the lack of robust growth because, dern it, we’d just built too many homes back in ‘05, and so there was nothing for those workers to do. If I had a time machine, I’d go back to 2011 and just go door-to-door glove-slapping every cheek in the land. We’re America, dammit. What the hell got into us!? Just a pointless and unnecessary economic tragedy.

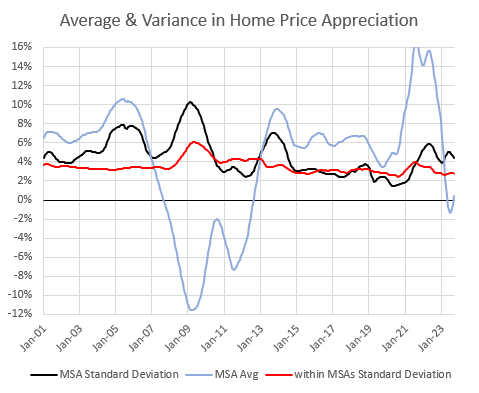

In Figure 4, I repeat the average 1 year price change and the standard deviation among metro areas and add the standard deviation of price changes among ZIP codes within each metro area (the average change of each metro area has been erased to highlight the variance of changes within metro areas). That’s the red line.

You can see that all the pre-2008 boom-time price changes were changes between metro areas. Prices were rising, and some metro areas were rising more than others. But, if you were in one ZIP code within a high flying metro area your home’s price was probably rising at about the same pace as home prices in ZIP codes on the other side of town.

By the way, all those countless academic papers trying to get to the bottom of what caused the so-called bubble? They generally erase the metro area differences, too! So, when they claim they find large price increases in neighborhoods with reckless lending or speculation, they are basically looking into the increase in the red line for the cause of the boom. Seriously.

Then, you can see here that once mortgage access was severely limited and home prices really started to collapse, then there were big differences within cities. And the difference (not obvious in this chart) was always that poor neighborhoods collapsed the most. At first, there was more variance between cities, too. But, by 2010, the differences between cities were as low as ever while the differences within them remained elevated. The academics that were looking into that red line in 2005 never look too closely at this. I don’t think I’ve ever seen a housing bubble paper carefully consider the massive change in lending standards that happened in 2008. But they always treat this period as a confirmation of whatever they thought they had found in that rising red line in 2005.

Variance of price changes both between and within metro areas remained low for the next decade. We were all in the same boat. Some variability came along with the Covid bump.

And, now, looking back at Figure 3, both the average and the variance in price changes between cities is pretty similar to what it was back in 1983. By 1983, inflation was permanently back under 5%, so the subsequent positive trends in home prices weren’t particularly boosted by excess inflation. That’s pretty interesting, because mortgage rates were nearly double what they are now and remained around 10% for the rest of the 1980s.

Of course, you and I already know that mortgage rates don’t seem to matter much for home price trends.

The scale of Multi-Unit Construction and Rental Vacancies

Finally, here is multi-unit completions (annualized rate) versus rental vacancies. (I think much of the shift in vacancies in the mid-80s is from measurement changes, so I would treat the 1986-2000 vacancy rate as the baseline.) I have shared other vacancy vs. construction charts. But, I thought focusing on multi-unit / rentals might add a little color.

A few comments I would make:

The 8% rate is a baseline, but keep in mind that all pre-2008 national data is a mixture, since we had a handful of cities with perpetually low vacancy rates. Vacancy rates in the Closed Access cities (NYC, LA, SF) tend to remain at 4-6% with little change.

So, the 10% vacancy rate from 2003 to 2007 was a combination of Closed Access vacancies, stuck at 6%, and vacancies in the sunbelt and rust belt that bumped up to 12%. In one of my Mercatus papers, I showed that, across metro areas at the time, high vacancy rates didn’t follow increased construction or high prices. So, I think the range of “baseline” sustainable rental vacancy rates in this history of experience includes rates of 10%, and possibly as high as 12%. The cities where declining prices and construction triggered the crisis in 2007 and 2008 were cities with relatively low vacancy rates in 2006. The “Contagion” cities in Figure 5 are cities in Arizona, Florida, etc.

The final spike in vacancies in 2008 and 2009 was specific to the Contagion cities because decades-long migration patterns suddenly collapsed. It was a demand shock, not a supply shock that created those vacancies. This happened well after construction had dried up.

Since the 20th century, the scale of vacancies has become much larger than the scale of new construction, mostly because we haven’t had a multi-unit building boom for decades. This leads to two important implications today.

We simply cannot build too much right now, nationally. Vacancies are an important component in rent trends, and new multi-unit construction requires a sea change to get to a scale that compares to the level or changes in vacancy.

The way that healthy housing markets generally work is that there is a lot of discretionary use on the margin. 10% of the stock is empty, and tenants engage in various forms of use, including creating new households, within that big blob of capacity. Discretionary choices are what determines usage on the margin. Now, we are in a state of deprivation. Desperate choices are now what determines usage on the margin. There should be more than a million additional empty apartments acting as an available buffer for marginal housing decisions. The regime shift back to abundance is what’s important for macro-level housing supply and demand. The industry doesn’t even have the capacity to create that under current conditions. imho, low interest rates can’t solve that problem and headwinds like high interest rates won’t significantly lower effective capacity, since demand has been well above capacity for years. It may look to insiders like activity is dead, but I suspect part of what is going on is that the individual projects that proceed will change. So, individuals working on individual projects will see a lot of disruption. But, projects that “pencil” on different margins will now be the projects that fill in the pitifully low capacity allowed by municipalities. The aggregate numbers will be less volatile than the sentiment and experience of each insider struggling to keep their own projects afloat.

With a low flat line of multi-unit construction rates for decades, we first had a period with rising vacancies and then a period with declining vacancies. Even though these are vacancies that are generally in apartments, the two trends were created by the rise and then decline in single-family construction, not by multi-unit building. This chart is one way to visualize one big issue with American housing. The obstruction of infill multi-unit construction has been the problem across the country for at least 30 years, and for the first half of those 30 years, much of the country papered over that problem by making up for it with single-family construction in the exurbs. A lot of places could still do that today. The continued strict regulation of mortgage access has blocked it for the last 15 years. Institutional build-to-rent buyers have recently stepped in to be the intermediaries to facilitate that new construction. That is still just papering over the primary problem. But papering over the problem is better than doing nothing. You can see two symptoms of our housing pathology here.

Many macro-econ observers, analysts, investors, insiders, etc. worry that there are more multi-family units under construction than we can absorb without experiencing market dislocations. Or some claim there isn’t a supply problem because more units are under construction. Etc. This is benchmarking to an unsustainably dysfunctional market.

Some housing supply skeptics and even some worthy pro-housing advocates complain about private equity bidding up home prices and crowding out homeowners. After 15 years of our vacancy trend together with the flat trend in multi-family construction, if your reaction is that we need to further limit who can buy or build housing, you are the actual problem. Please reconsider, at a deep level, how helpful your intuition is to creating a better country for everyone. If you are among the local political influencers and policymakers who has some part of your hand on the levers of local political control, please consider that when it comes to adding more “you can’ts” to the long list that currently inflict us, caution is the better part of valor.

What the Fed missed in the price run-up in housing in the early 2000's was the increasing contribution of land values to sale prices in certain Metro areas. Same address sale figures had become distorted because zoning restrictions had effectively stopped more efficient uses of property. The Case-Schiller index should have been named "Residential Building Lot Prices Induced by Local Control Factors."