"Price is the Medium Through Which Housing Filters Up or Down": Part 3

Price/Income as a supply indicator

In Part 1 and Part 2, I described a process through which the upward filtering of existing homes especially leads to rising prices on the poorest families in housing-constrained cities. Here, continuing the discussion of my new paper at Mercatus, I want to back up and just look at the basics. What does the price/income slope tell us.

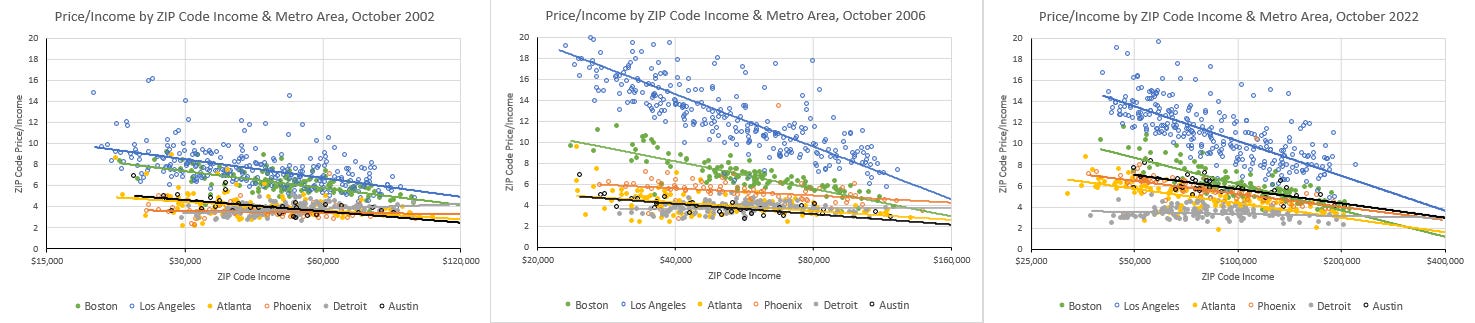

In posts 1 & 2, I shared a figure of price/income levels in Los Angeles and Atlanta. In Figure 1, I have added several other cities and compared 2002, 2006, and 2022. There is a difference between metro areas, there is a difference between different points in time in each metro area, and most of those differences are related to a change in the slope of the best-fit price/income lines.

Where housing is undersupplied, it creates much more of a rise in low-end housing costs than it does at the high end. This is a universal trait.

Yet, a scatterplot showing the median home price and income of different metro areas will have a positive slope - richer cities have higher price/income ratios. But, that is mostly because prices in the poorest neighborhoods of housing-deprived cities move up enough to force poorer residents to move away. The upward slope of the medians is mostly due to the compositional changes in regional incomes created by semi-voluntary displacement of poorer families to places where more new housing is legal.

That leads to this ironic evidence. Inadequate housing mainly increases the cost of being poor, but the medians make it look like inadequate housing mainly increases the cost of being rich. That leads to an overestimation of the demand for and value of living in housing-deprived cities and to wrong-headed takes like, “Well, of course LA is expensive. Nice things cost more.”

Housing is a tricky market to analyze because neither demand and supply elasticity are consistent. A 10% increase in rent will affect the housing consumption of a poor family, a middle-income family, and a rich family in different ways. And, likewise, it will affect the rate of construction of new housing in Phoenix, San Francisco, and Cleveland in different ways. And, it will affect the rate of construction in Phoenix in 2002, 2005, and 2010 in different ways.

I hope that the framework in my paper can be useful in this regard, because currently it is common for researchers to cite supply elasticity or rates of filtering that, necessarily, are constructed from observations that span years or decades. The price/income slope in my paper isn’t exactly a measure of supply elasticity or of filtering, but it can provide a pretty good proxy for supply conditions and their consequences, and it can provide real-time feedback about whether housing supply in a city is getting better or worse.

Since the effect of inadequate supply is to steepen the negative slope of price/income ratios across each metro area, the y-axis in Figure 2 could be labelled as the inverted slope of the price/income line from Figure 1, or more tersely, “Price or rent for residents with low incomes”. Most cities before 2008 were around point 1 in Figure 2. It is the anomalies that move to contexts where supply is inelastic (in other words, higher or lower prices have little effect on quantity and, so, more effect on price).

Actually, I think it is pretty obvious that both the short run and long run supply curves are downward sloping at points above point 2 in Figure 2. (Higher prices and higher demand are associated with lower production of new housing and definitely with lower capacity for residents within a metro area that moves up above the “point 2” context.) That is why we aren’t seeing expensive cities correct back to the norm. I’ll have to save that topic for a later date.

In this post, I just want to highlight how the slope of the price/income line can convey both cyclical changes and long-term cross-sectional differences between cities. Since the supply curve for each city is characterized by these two sharp curves - vertical at the top and bottom and flat in the middle - changes in demand can change supply conditions.

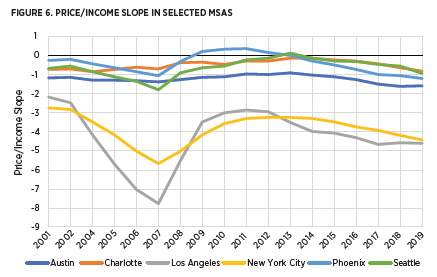

Figure 6 from the paper highlights this. This is a chart that shows the slope of the lines from Figure 1 above for various metro areas from 2001 to 2019. You can see that it was common for the price/income slope to steepen from 2002 to 2007. (The increase in housing demand - the trigger for the housing boom - was pushing most cities further to the right on the curved supply curve.) But, where the slope steepened the most was in the cities with a very narrow supply curve, where it turns vertical at very low levels of growth, so that an increase in demand could only have one result: prices had to rise even more sharply on the poorest residents so they would move away and make their former homes available for the others.

So, the rise in home prices was triggered by a change in demand, and the change in demand has dominated the focus of analysis about what happened. But, it was the pain required to initiate migration away from supply-deprived cities that drove the bulk of the valuation changes.

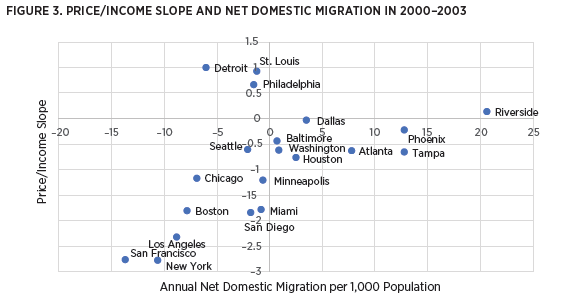

Two other figures from the paper point to this relationship. Figure 3 from the paper compares the price/income slope (Remember, more negative means more expensive for poor families.) to net domestic migration from 2000 to 2003. The cities with very wide supply curves, that don’t go vertical unless growth is very high, are to the far right. Net migration is positive. Many families can move to those cities, and they are still near point 1 on the supply and demand graph - elastic supply and a relatively flat price/income line. Then, there are a group of cities down and to the left. These are the housing deprived cities. The more deprived they are, the steeper the price/income slope has to get to move 5 or 10 or 15 families per thousand away to make room for those who will remain in the limited stock of housing. The more limited your stock of housing, the more families have to move away, the more painful it will need to get for poor residents as they lose the bidding war for shelter so that they move away.

Figure 5 from the paper shows how the price/income slope changed during the 2002-2006 housing boom. The x-axis measures the relative change in population growth from 2002-2006 compared to 1998-2002. The y-axis measures the change in the slope of the price/income line from 2002-2006.

If the typical family was consuming more housing (maybe through fewer members per household, larger units, consolidating units, tearing down and rebuilding units, more second homes, etc.) then that meant that there was room for fewer families in the housing-deprived cities. So, cities that were up around point 2 in Figure 2 had to depopulate. That happens through the process of the price/income slope steepening until housing costs are unsustainable for some families. So the left end (depopulation) of Figure 5 was associated with sharply steepening price/income slopes. (It also has a couple of cities - Austin and Denver - who for idiosyncratic reasons experienced a downtrend in population growth, so they didn’t experience bubble conditions and home prices remained moderate.) At the right end (increased population growth), were the cities commonly referred to as the “bubble” cities, where the increase in housing demand (which includes all the forms of increased demand that led to depopulation of the housing-deprived cities, plus the added demand of the housing refugees that had to move out of those cities) pushed them a bit to the right on their supply curves, and also steepened their price/income slopes. But, they steepened much less than the housing-deprived cities did.

In the paper, I discuss how in a normal market, with some supply elasticity, home prices are generally bounded by the cost of construction, rent, and discount rates on future rents. It is a static analysis. If prices rise above the cost of construction, new homes are built until rents decline to bring the market back into balance.

In cities with vertical supply, it is not a static analysis. The market is determined by flows. How quickly will residents migrate and segregate. The local housing market doesn’t find equilibrium because rents decline to a relatively stable cost of construction. It finds equilibrium because the incomes of the tenants increase as families segregate under duress.

That’s enough for this post. In the next post, I’ll go into migration and filtering a bit more.