More detail on "The end of location..." for subscribers

Last week, I posted about how real estate investments used to be almost purely an idiosyncratic, localized process. “Location, location, location”. But the deep and, now, relatively wide-spread importance of constrained supply has turned it into a more macro-driven marketplace.

In summary, real estate has always been about location, location, location, but now it’s about incomes, incomes (as it relates to the migration of families into existing neighborhoods in search of scarce housing), location.

This change sort of rhymes with how macro-level factors, themselves, have changed with regard to housing. There may have been a time where macro-level factors could have been described as “interest rates, interest rates, interest rates”. Now it’s more, “rents, rents (as it relates to expectations of supply constraints and the discount rate applied to those expectations), rates”. And, here, even where rates could be important, they have recently been much less important than changes in access to capital at any rate.

Rents and incomes, now dominate, rather than location and interest rates. This isn’t because location and interest rates became less important, in absolute terms. It’s because we have created a context where rents and incomes are associated with unprecedented volatility. The market has changed because, increasingly, the marginal cost of housing now is an extraction of political rents rather than an application of capital into physical structures.

Most of the references to the old Case-Shiller real home price index try to explain today’s market as if the factors that were important back when real home prices were stable have somehow become unstable. But, if those old factors (location and rates) were still dominant, home values would still be as stable as they used to be. Real home values have become volatile because those old factors have been overtaken by constrained supply conditions. Rents and incomes are important in a way that they never were before, and never should be.

Understanding this as a policy maker can help heal wounds that we have created in our economy. Understanding this as a trader and investor can earn you profits while other capital allocators remain confused.

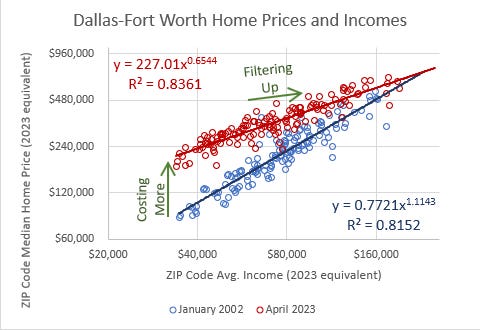

I used Figure 2 in the earlier post to visualize the importance of income in the new, supply-constrained market. I used Dallas as an example. The exponent on the x variable is the important signal here. Where housing is amply supplied, home prices tend to be proportional to household incomes (the exponent = 1). An exponent above, say, 0.8 is a signal of reasonably ample housing supply. Few cities continue to exhibit such levels of affordability. Where homes are hard to build, a bidding war on the existing stock put families with lower incomes at a disadvantage, and prices tend to rise in an income-sensitive pattern. Figure 2 isn’t really an advance from my earlier posts on this. It’s just a different way to visualize it.

By the way, essentially all of the spike in the real Case-Shiller price index since 2002, from Figure 1, is from these peculiar income-sensitive price trends.

One response I sometimes get from people who attribute volatile and high home prices to low rates, federal subsidies, etc. is that I have not established a causality from higher rents to higher prices. The correlation could be from higher prices to higher rents (for instance, because low rates allow marginal home buyers to buy homes with higher values).

In the “normal times” when rates and location mattered more than income and supply, and when price volatility and regional variance were much lower, a causation in the other direction might have been plausible. I suppose it is understandable that someone working with that model of causality would react in such a way. I think it’s a good example of still trying to apply the old logic to a new context.

I’m not going to attempt to establish the causality here. I think the details of that causal story populate all of my recent research papers. If you’re interested, you can look there. But, I think, in this case, disproving the price-to-rent causality may be a more direct path. Looking at Dallas in Figure 2, and considering the extreme tightening in mortgage access from 2002 to 2023, the decline in housing construction, the decline in homeownership rates, the income-sensitive increase in rents and rent/income, the decline in migration rates into growing cities, trends in real housing consumption per capita, etc. The price-to-rent causal narrative is untenable.

Rents in Dallas ZIP codes with less than $50,000 incomes aren’t rising to unprecedented portions of resident incomes because those residents are piling into big new houses with cheap, easy credit. Being able to come to an understanding of this through your own volition is a pre-requisite to having a serious conversation about housing. It may have been plausible for rising prices to be causally related to a few % of rent inflation in the 1970s. It is less plausible that that is the case today, and it is certainly implausible that it is causally related to a cross-sectional 40% divergence in local rents in some cities.

Aaaanyway, I thought readers might be interested in seeing the data displayed in this way in other metropolitan areas besides Dallas. Since this uses Erdmann Housing Tracker data, the rest of the post is below the pay wall for paid subscribers. “Founding” subscribers get time series data on all of these metropolitan areas each month.

Keep reading with a 7-day free trial

Subscribe to Erdmann Housing Tracker to keep reading this post and get 7 days of free access to the full post archives.