What homes are missing?

There are 3 major obstructions to appropriate American housing.

A lack of multi-family, missing middle, and infill housing in every American metropolitan area.

A lack of single-family housing in the suburbs and exurbs of metropolitan areas in the northeast, where zoning has created artificial capacity limits throughout New England and greater New York City. And, in the coastal California metropolitan areas because of both natural and chosen geographic limitations to sprawl.

A lack of single-family housing everywhere since mortgage access was shut off for millions of households in 2008.

Before 2008

Before 2008, the main constraint in American housing was obstruction to city-building. So, millions of families moved out of the large, expensive coastal metropolises, where marginal growth would have been infill and multi-unit. And, when they moved to other cities, they moved into single-family neighborhoods in the exurbs. And, within all the other cities, existing residents and new residents from surrounding rural areas were also moving into the exurbs instead growing the interiors of cities as cities had traditionally grown.

From 1990 to 2010, shown in Figure 1, this was associated with an increased proportion of households living in single-family homes and a lower proportion living in multi-family. Both rented and owned single-family increased over that period.

There were a combination of factors. Older families tend to be owners and tend to live in single-family homes. Cities block multi-family construction. There was an increase over that period in homeownership, even after adjusting for age demographics. Considering that increase, the rise in rented single-family units is especially telling. Even with rising homeownership, households were being sorted more into single-family units. Multi-family obstructions likely had a lot to do with that.

But, until the Great Recession, those obstructions were mostly changing the composition of the housing stock and the location. It was only after 2008 that the gross quantity of new homes shifted down sharply. Both single family and multi-family housing have been undersupplied since 2008.

This stopped the change in composition. Now, both single-family and multi-family housing were obstructed in similar proportions. There is a natural division between single-family and multi-family, all else equal, that single-family is favored by owners and multi-family is favored by landlords. Where there is a lot of overlap, it can be a sign of market disruptions.

After 2008, there was more sorting along those lines. More of the single-family stock was used by owners and more of the multi-family stock was used by renters. Keep this in mind when you see claims that private equity landlords have been driving up the cost of single-family homes. It is homeowners that have been claiming the stock of single-family homes. Households that had formerly been single-family renters became multi-family renters.

That should have always been the case, because there should have been more options in multi-family housing. But, in our case, this was because first multi-family was obstructed by local regulations, and then single-family housing was obstructed by mortgage suppression. Those who could get mortgages bought up discounted existing homes and those who couldn’t get mortgages were left with a dwindling number of single-family homes for rent and the always-limited number of multi-family homes.

The end result has been that rent inflation has been high enough to get households to forgo housing, either by downsizing, taking on roommates, moving away from expensive cities, not moving to formerly growing cities, or becoming unhoused.

Future Trends

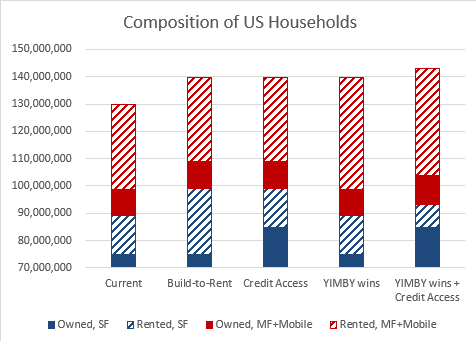

As shown in Figure 2, there are now about 130 million occupied homes. (This is 2022 data.) Here, I want to walk through what is likely to happen in the American housing market under different scenarios. This is meant to be very general and broad. If we could snap our fingers today and create various different outcomes, where the results played out immediately. At current population levels, how would housing change? Of course, in reality, changes will take years to play out, and population and housing production will rise somewhat over time as that happens.

Keep in mind, y-axis starts at 70 million because, baseline, there are more than 70 million households that own single-family homes. So, I have cut off the y-axis to see marginal changes more clearly.

We are currently at least 15 million units short of supply that would be associated with a reversal of excess rent inflation. That would include at least 10 million additional occupied units and 5 million vacant units. Those numbers would be associated with a neutral vacancy rate that would be associated with moderate rent inflation and additional occupied units that would absorb the new households that have been stunted by the housing shortage.

Since Figure 2 is the quantity of occupied units, I am going to discuss this in terms of a 10 million unit increase.

Current

The leftmost bar is the current condition.(*) With no policy changes, in our current condition, new build-to-rent single-family will fill that gap. There is little we could do to stop this, short of banning it. This is simply because it is the only legal means for meeting demand for housing on the margin. Rents will rise to the level needed to induce new building of this type. Eventually, at something north of 10 million units, rents should stop rising, and the housing stock might settle in to a new normal, rising from there in proportion to natural household formation patterns under our current constrained norms.

Build-to-Rent Single-Family

A build-to-rent build out could stop the continuation of excess rents and homelessness, but the reversal of those issues would be slow and long-term. Cross-sectionally, families will slowly settle in to new norms where renters with low incomes would live in housing that is relatively worse than housing that homeowners live in. Eventually, that will settle into consumption norms and families will stop running just to stay still in markets where rents are rising faster than their incomes can keep up.

If that could happen with a snap-of-the-finger, we’ll end up with 140 million occupied homes, the additional units would be roughly 10 million single-family rentals. But, there is a significant chance that the problems which this new market will actually be helping to heal (rising rents, worse housing) will be blamed on the providers, and it will not be allowed to function.

New Credit Access

If credit access was returned to pre-2008 norms, (If you’re new to my work, I am not referring to a return to the subprime private securitization boom. I am referring to a return to standards for all other types of mortgages to late-20th century norms.) we would roughly have the same outcome. There would be 10 million additional single-family homes. But, they would be owned instead of rented.

The main difference between this outcome and the status quo outcome with build-to-rent is that rents would be much lower.

Think of it this way, the long-run housing supply curve is either flat or vertical. It is vertical in Los Angeles. Los Angeles isn’t going to permit more homes than a rust belt city would, even if the average new unit goes for $2 million. The supply curve is flat in Dallas. If households are willing to pay enough to cover the cost of construction inputs, there will be some lot out at the far edges of the city where a new single-family neighborhood will be constructed with minimal land cost.

It is the binary shape of the supply curve that leads me to expect binary outcomes in the supply responses.

Since the imposition of mortgage suppression in 2008, entry-level single-family home prices were pushed too low for that exurban Dallas market. Families that can get mortgages buy up some of the single-family housing stock each year in Dallas, plus they buy about 5 new homes per 1,000 residents. Their demand is sated. Multi-family maxes out at about 3 new units per 1,000 residents because of NIMBYs. So, it is unable to fill the gap. (Figure 3)

Almost every city with elastic supply basically looks like Dallas. The supply curve of single-family homes has been vertical because of mortgage suppression. The supply of apartments has been vertical because of NIMBYs. Rents have risen high enough that the supply curve will turn horizontal again for single-family homes even under current credit conditions. More access to credit will mostly just make those new homes owned homes instead of rented homes.

Maybe, if you’re being a stickler, the top of the “Credit Access” bar in Figure 2 should be a smidge higher than the “build-to-rent” bar. But, I think at this peculiar point in American housing markets, it will mainly lower rents for renters who remain in the rental market. Newly funded owner-occupiers will outbid landlords. That will raise the price/rent ratio on new homes. But, the prices of the marginal new single-family homes out on the edge of the city will be mostly determined by the cost of inputs. So, when funded owner-occupiers bid up the price/rent ratio on single-family homes, the net effect will be lower rents.

YIMBY Wins

What if credit remains tight, but YIMBYs accumulate a lot of wins on local land use regulations. Then, the outcome will be a mixture of the “build-to-rent” outcome and the “credit access” outcome. There will be 10 million new occupied units. But, they will be apartments and multiplexes instead of single-family homes. This would make the supply curve of multi-family units more flat instead of vertical, so, on the margin, this would also bring rents down. Rents have to rise to make a single-family build-to-rent market (which has never existed naturally, at scale, under previous conditions) develop. Rents wouldn’t have to rise to make multi-family economical, if cities allowed them to exist. This would effectively be a build-out of the units that should have been built over the previous 40 years.

Obviously, zoning is a big part of NIMBY obstruction, but there are also many other related processes in place to inflate costs. So, YIMBY wins would need to include some change on all of those margins.

YIMBY Wins and Credit Access

I think the point that came across for me, thinking these issues through in this way, is that either credit access or YIMBY wins could bring down rents. Lacking either, metropolitan areas will continue to sprawl through the growth of build-to-rent single-family expansion. YIMBY wins are the only sustainable way to bring back traditional city building and to slow down sprawl-centered growth.

There are two separate issues. Rising costs are a more acute issue of human suffering and stress. They could be solved by either YIMBY wins or improved credit access. More appropriate urban development that would allow more infill housing production addresses a longer-term issue about development patterns and economic options for American families. There is an affordability issue there. In the few dense urban centers we built before we made them illegal, urban density is generally an inferior good. Families with low incomes value the amenities that come with urban density, and so making that option available again would be a progressive economic benefit.

If we achieve both credit access and YIMBY wins, I think the end result would be marginally better than the outcome of either on their own. There would be fewer single-family homes and more apartments than there would be with better credit access alone. There might be a few more single-family homes than there would be with YIMBY wins alone, but mostly, rents would be lower for all families. There would be more owned single-family homes, but mostly that would be paired with fewer rented single-family homes. There would be more apartments, and apartments would be a better option for renters, in general, because they are preferred by landlords.

Just like in the housing stock in 1990 and before, owners would choose single-family and renters would choose multi-family, with less overlap than there is today.

Footnote

(*)The leftmost bar is the current condition. If we banned new single-family build-to-rent today, this is where we would remain. Rent inflation would continue to rise. Homelessness would continue to increase. There would be no upward bound on housing costs. Housing costs, going forward would be moderated through individual diminishment of the quantity of housing demanded - more roommates, more homelessness, etc. I suppose over time, that would include a continuation of the patterns of the last decade. The proportion of the owned single-family housing stock would continue to grow, while renters would continue to squeeze into a smaller portion of the stock of homes - increasingly into apartments rather than single-family homes.

Think of it this way. There is a discontinuity from the underwriting standards used to suppress mortgage access. The marginal household that can get a mortgage under today’s standards will have lower costs than renters who are denied mortgages. So, with broad supply bans across housing types, homeowners will continue to claim a larger portion of the stock of available homes while renters are forced to pay rising rents on a dwindling portion of the remaining housing stock.

Based on some of your comments on Twitter, would you consider some posts on the current shape of the legal environment for YIMBY vs. NIMBY and also mortgage access? YIMBY moves are facing resistance from some courts, but I wonder if this will start to generate more discussion about how we got the Zoning regulations we have now. (Spoiler: It was racism)

Also, the history you outline in this post explains the rise of the Sunbelt and some shifts in the political map. California and New England export young couples to places like Texas, Florida, Nevada, and Arizona. When they get settled there they vote Republican it seems.

Okay, this answers most of my previous question. NIMBY and mortgage qualification changes post 2008 reduced the availability product for SF buyers.