Categories of Housing Contraction, Part 1

The Normal 20th Century

In my post reviewing July new home sales, I suggested using 4 categories for thinking about a contraction in housing:

Demand outstripping capacity. Sales high, homes under construction increasing.

Demand normalizing. Sales declining, homes under construction high but decreasing.

Demand overcorrecting. Sales declining, homes under construction declining.

Demand excessively overcorrecting. Sales bottoming, homes under construction declining, prices declining.

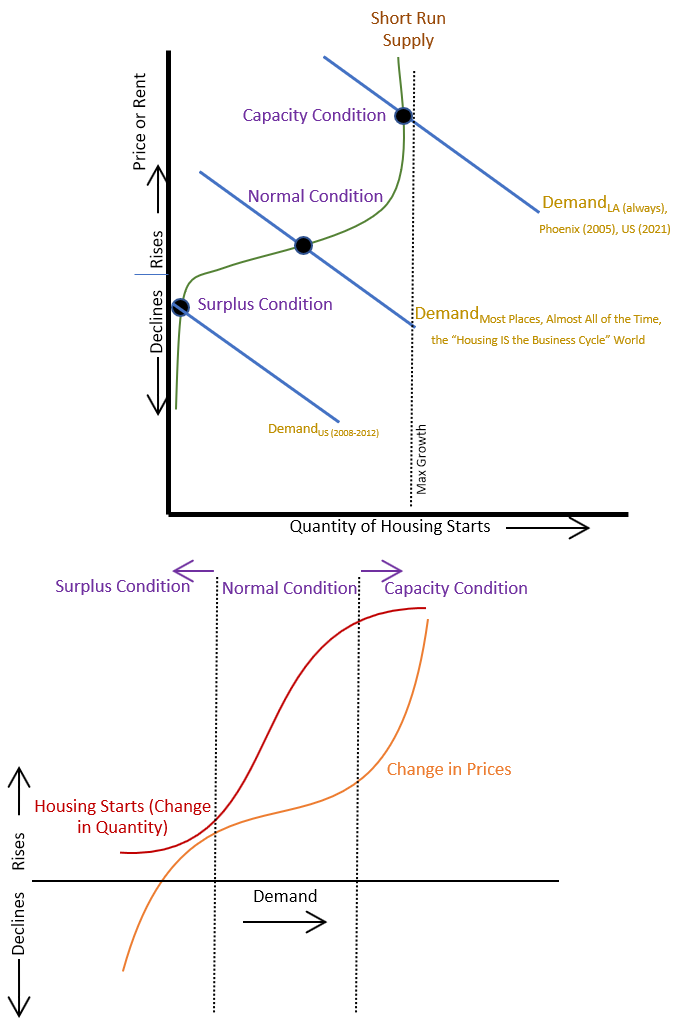

Below is a picture that I think can help think about this. I’m going to take a few posts to use this figure to think about transformations in the American housing market.

The top section is a basic supply and demand curve. One tricky thing with housing is that supply and demand elasticity are not uniform, and for supply, this diagram reflects that. The supply curve here is the short run supply curve for a given metro area’s housing. Every metro area has an inelastic base of supply, which is the existing stock of homes, some range of highly elastic supply when rates of growth are low, and a maximum rate of growth where supply becomes inelastic again. Making this even more complicated, US markets have developed so that the max growth level kicks in at about 1/2% annual growth in the Closed Access cities like New York, LA, and San Francisco. Then, there are cities like the Texas cities that can grow at 3 or 4% before supply becomes inelastic.

I have simplified the demand curves here, for the sake of this discussion, but demand also follows an s-curve. Demand is relatively elastic for households with high incomes. (Think of young engineers in San Francisco earning 6 figure incomes while sharing a bedroom with co-workers.) For households with moderate incomes in markets with inelastic supply, demand becomes highly inelastic. (Think of families with relatively low incomes throughout the Closed Access cities that spend 50%+ of their incomes on rent.) Those households eventually hit a maximum budget level where demand for housing again becomes highly elastic. (The families renting those $1,000 U-Hauls out of Los Angeles.) This is a topic of the next paper I’ll have coming out soon at Mercatus. Effectively, what is happening in the US, because of inelastic local housing supply conditions, is that Americans are sorting and segregating according to our individual housing demand elasticities. The results of that process create a predictable pattern in home prices, and that pattern is what the Erdmann Housing Tracker picks up. But, that discussion is for another time.

You could call the three regimes of supply elasticity, “Surplus Condition” where the existing stock is inelastic, “Normal Condition” where supply is elastic, and “Capacity Condition” where a city is unwilling to increase supply. (I would use the term “Shortage Condition” here, and I tend to toss the term “shortage” around a lot, but economists tend to be touchy about that term. To me, it seems perfectly reasonable to use the term where people are living in tents in public spaces who aren’t allowed to build anything more substantial than a tent, at any price, because city officials won’t allow it. Or, in California where one reason for objecting to new housing developments is that their price is too high. That seems like it meets even the pedantic standard for a shortage, but “Capacity” works just as well here.)

Aligned under the supply and demand chart is a chart showing the behavior of quantity and price across these regimes of supply elasticity. Trends in quantity and price have opposing shapes. Supply (as in housing starts) is very pliable in the Normal Condition and price is relatively stable. But in both the Surplus and Capacity conditions, supply is relatively fixed and price becomes unstable.

The four categories of housing contraction are basically descriptions of these regimes. Category 1 is in the Capacity Condition and getting further from Normal. Category 2 is in the Capacity Condition but getting better. Category 3 is in the Normal Condition. And Category 4 is in the Surplus Condition.

Here is a chart of housing starts plus manufactured home shipments, since 1966, along with percentage changes in rent (compared to core inflation ) and percentage changes in price/rent ratios.

You can decently approximate the need for new housing to accommodate population growth with stable housing standards with the thin blue line just under 5 units/thousand residents until surprisingly recently. (I address this in one of the upcoming Mercatus papers, but this flat estimate is close enough for my purposes here.) So, deviations in housing production above and below that line are basically cyclical changes in housing plus permanent per capita increases in housing consumption over time.

In the 20th Century, at least since the end of the Great Depression, we were in “Normal Condition”. That meant that cyclicality in housing was mostly expressed as changing construction activity. Rent inflation was somewhat volatile, but since housing quantities so easily rose and fell to reflect changing demand, price ratios weren’t any more volatile than rents were. Prices in the Normal Condition are moderated by the cost of construction and expected future rents. Adequate construction activity will keep rents near long-term norms, and so prices reflect an expectation of normalcy.

You might notice that there was never a down cycle in housing between 1966 and 2008. Housing production was always at a higher rate than was necessary to meet a stable level of housing consumption for a growing population.

One reason for that was that household size was declining at the time. There were some cultural and generational reasons for that. But, there are a lot of reasons to expect housing cycles to net out to a positive average. Living longer, staying active longer, staying single or in school longer, having fewer children, greater wealth and income for vacations in intermittently used homes, second homes, seasonal homes, etc. All of these are perfectly reasonable and predictable reasons for any functional, successful economy to be associated with consumption of housing above the level needed for a growing population to subsist at previous norms.

The decline in household size leveled off in the 1990s, and at the same time the signs of a “Normal Condition” disappeared. Now, housing production is never far above subsistence. Rent inflation is less volatile but tends to remain perpetually above core inflation. And, now, during cyclical highs prices are volatile instead of construction activity. During cyclical lows, prices and construction have both been unusually low. In the 21st Century, we are swinging wildly from the Capacity to the Surplus Condition. That’s not easy to do. The reason the 20th Century remained so dependably in Normal territory is because you have to engage a lot of coordinated nonsense to move out of it.

An irony of the Capacity Condition is that every alternative use for a home is stress inducing, so people frequently complain about how short term rentals, pied-à-terre, institutional investors, etc., etc. are taking away homes from people that need them. This is not a problem in the Normal Condition. If we were in the Normal Condition, it is likely that household size would have continued to decline, there would be more vacant units, more second homes, etc., and there would not have been many complaints about any of them. The motivation to complain is a result of the Capacity Condition, not of an excess of demand. If I was making a list of “Rules of Housing”, that would be one of them. “Complaints about vacant homes are negatively correlated with their prevalence.”

There is nothing unsustainable about housing construction, even when it is for various forms of vacant homes, and I would argue, it is implausible that it could be. Maybe in some distant future we will be persistently in a condition of Surplus. (Even if we ever are, nobody will have to convince builders to slow down.) In the America of the 20th Century and so far in the 21st Century, we dependably grow into our housing stock. That housing stock may grow irregularly through up and down cycles, but, at most, at the peak of up cycles, rent inflation might moderate a bit. Mostly, we just consume more homes - households form, families buy extra homes, homelessness declines, etc. Fourteen new homes per 1,000 residents in 1972 wasn’t too many to find something to do with. Certainly 7 in 2005 wasn’t.

If the only short-term solution to the Capacity Condition in 2005 was reducing demand, that solution would have been to reduce demand to just below the Capacity threshold. There was no reason to go all the way to a Surplus condition. There was nothing to reverse. Exactly what reversal was supposed to happen? Was demand for housing ever going to get so low that the millions of households who had moved out of constrained cities like LA and New York City were going to move back? Of course not! They were mostly moving away from grossly unsustainable costs. The only way that migration could reverse is if those metro areas move their Capacity thresholds far higher by permitting more new homes, like they used to, for a long time. So what was the housing collapse that is treated as an inevitability in every popular description of the time supposed to accomplish in 2008? The collapse was the result of not fully recognizing the Capacity Condition, so that the explanations of what had happened had to be constructed from puzzle pieces that could not form a coherent whole - a condition which had never existed before, and in fact didn’t even exist at the time: too many homes at too high a price.

In Part 2, I will discuss further how the calamity of 2008 relates to this process.

In Part 3, I will discuss today’s market using this framework.

On Twitter you made a comment about the decimation of skilled trades as a consequence of the Great Recession. It's as if the Fed decreed that carpenters, electricians, and plumbers were an obsolete category of the economy and deserving of decades long punishment for the supposed excesses of the "housing bubble."

What's most tragic is that despite the relatively good times of the past few years, many trades are aging out, exhausted, and permanently scarred by the generational destruction of the housing markets. And, in defiance of economic principles, their scarcity has not translated into the sustained wage growth that would attract new talent---combined with immigration policies that discourage participation and expansion of talent. The housing supply deficit may be permanent---or at best a two decade phenomenon---because of the comprehensive labor shortage.

Rant over. Keep up the good work Kevin.