The Housing Shortage Is Larger Than You Think: Part 2

Lance Lambert reported on a couple of different pieces of housing analytics that make for an interesting pairing, when you put on the EHT-colored glasses and consider all the implications of what they are saying.

First, he reported on Bank of America analysis:

Bank of America housing analysts believe that “underbuilding” of U.S. homes over the past decade has not only “absorbed the 2 to 3 million home glut from pre-financial crisis overbuilding” but has also created a "deficit of 4 million" U.S. homes.

Simply put, Bank of America thinks we went from an overbuilt nation to an underbuilt nation over the past decade.

Then he reported that home prices spiked by 41% during the Covid boom and that San Francisco Federal Reserve Bank research attributes 60% of that rise to the work-from-home wave.

There was excess household formation amounting to 2.2 million households from 2020 to 2022. Other Federal Reserve researchers concluded that new housing supply would have needed to increase by 300% to match that.

I think these assorted assertions outline the basic conventional wisdom on housing. Before 2008, we built too many. Prices went up then because of unsustainable demand, and then inevitably declined. Then, after 2008, we didn’t build enough. Then from 2020 to 2022, there was a natural surge in housing demand related to “work-from-home” trends that was just too great for new supply to match to keep prices from rising.

As is my wont, I’m going to poke and prod at these assertions a bit.

How do we know there were 2 to 3 million excess homes before 2008?

I’m not sure what the source or justification is for the Bank of America claim that there were 2 or 3 million excess homes before 2008. The presumption that there was a glut of housing before 2008 is such an important cornerstone of so many explanations of what has happened and what should have happened over the past 20 years, and there are basically no formal studies of it.

The closest thing I have seen is a relatively unsophisticated paper from Federal Reserve Bank of New York staff, published in 2012. The 2 to 3 million excess units assertion aligns with that paper. The first issue the paper intended to consider was, “how much excess housing production occurred during the boom phase of the cycle and how far along is the correction?”

This was a remarkable sentence to publish in October 2012 for a number of reasons:

Generation-defining policy decisions depending on the answer to this question had already been implemented years ago.

The authors claim to know the sign of the answer, just not the scale, in spite of the lack of previous literature on the question.

The question also appears to beg the question regarding the scale of the excess supply, in asking, as of October 2012, “how far along is the correction”?

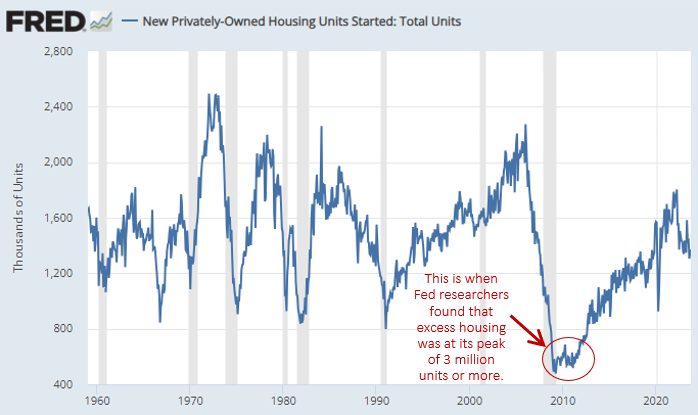

I have previously addressed some of the evidence in that paper, in my Mercatus paper, “Build More Houses”. The Fed researchers find 3 to 3.5 million excess units based on housing construction and vacancies, relative to trend. Their homebuilding-based estimate peaked in the first quarter of 2009 and their vacancy estimate peaked in 2010. They mention that household formation trends peaked in 2005 and had receded by about 2 million households by 2009. But, as noted above, the question they were asking was “how much excess”, not “was there excess”, so a full consideration of whether those excess units in 2009 and 2010 were due to a massive demand shock rather than from overbuilding was outside the scope of the paper.

Figure 1 notes the point in time where they identify peak oversupply. I will leave it as an exercise for the reader whether a negative demand shock or a positive supply shock are the most likely source of the 3 million unit supply mismatch.

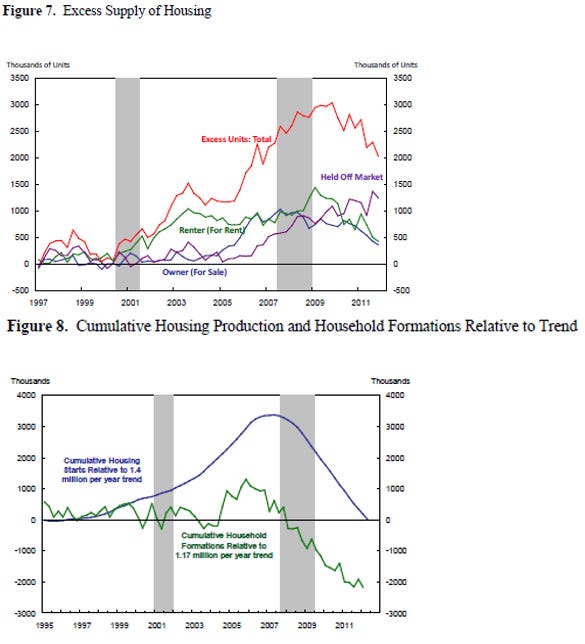

Figure 2 (consisting of Figures 7 & 8 from the Fed paper) shows the basic estimates of excess vacancies and excess homebuilding beyond household formation. An awful lot rides on the choice of trend. Could the 2005 vacancy rate have been actually the neutral trend level, rather than more than a million units into excess? Yes. Could the true neutral trend of homebuilding been roughly in line with household formation as late as 2005? Yes.

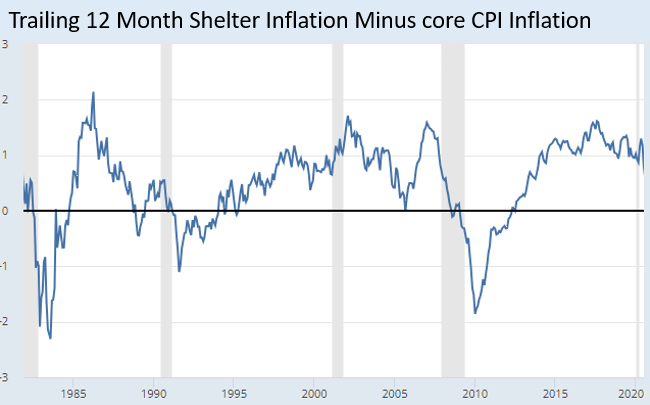

Figure 3 shows relative shelter inflation. There was a brief respite from excess rent inflation after vacancies shot up. At all other times during the period estimated in the paper, shelter (rent) inflation was elevated. For a moment in 2005, before housing starts peaked, it wasn’t. Excess rent inflation suggests undersupply, not over supply.

What if vacancies and homebuilding were at their neutral trend levels at the building peak? What if the rise in household formation in 2004 and 2005 was the expression of a decade of pent up demand because finally America was building enough housing (even if it required a massive migration event to get the households to where the houses were.) What if the entire increase in homes/household was due to the crash in households? What if the entire “excess vacancies” was due to a regulatory mortgage shock?

Does that make more sense, or does it make more sense that a building boom that abruptly ended in 2006 created 3 million vacancies in 2010 from excess supply?

Finally, on this question, in “Build More Houses”, I disaggregated housing production among the largest 48 metro areas. I found 2 million “excess” units there, relative to population growth in 2006. But, 500,000 of the “excess” units were in the Closed Access cities (NYC, LA, San Francisco, Boston, San Diego, and San Jose). The 500,000 gap was from the combination of above-trend building and below-trend population growth. There was a mass outflow of domestic migration from those cities in the 2000s.

Using the same 1990s trend lines, those cities again had excess housing of 500,000 by 2018. And, again, it was due to declining population trends and domestic outmigration.

This relates to the point I made in part 1 of this post. We are deep into a long-term housing shortage. Practically any naive trend line of housing production is going to be calibrated to unsustainably low production that is associated with rent inflation.

Demand for homes before 2008 versus 2020.

This brings me to my next question. Before 2006, there was a rise in household formation - about a million households according to the Fed paper above. From 2020 to 2022, there was a rise in household formation of about 2.2 million.

The rise in household formation was due to the Covid “work from home” shifts. We have decided that this is a thing. It’s a category. It’s legit.

The million extra households in 2006? Unsustainable. Probably a bunch of mortgage speculators that had no business being households. Really, more of a part of the oversupply than what you could legitimately call “demand”.

How did we come to this understanding? How did we decide which demand was legit and which was fake? When we decided, did we do robustness checks? Did we correct our standard errors? Did we apply all the right control variables, and calibrate them correctly? How many dozens of academic articles did it take to reach a consensus?

The rise in household formation from 2020 to 2022 would have required a 300% increase in supply, according to the Federal Reserve researchers noted above. Have they applied this approach to the pre-2008 period? Was there enough new supply to meet the rise in demand for households then? Could it be that there wasn’t enough supply then? Did they even wonder about it? Or, did they assume that there was no need for more supply then, because the rise in demand was unsustainable, and thus, the supply created to meet it would have simply been part of a bubble?

If we could have increased supply after 2020 by 300%, that presumably would have moderated prices. Would more houses from 2000 to 2005 have moderated prices? Surely not, if we had excess supply of 3 million units already.

Yet, that period was no different than the recent period. Prices were highest where vacancies were lowest. But, remember, according to household formation trends, the Closed Access cities (up at the top left in Figure 5) had 500,000 excess homes. Why were there were so few vacancies in cities with hundreds of thousands of excess homes?

The problem is that these simple truths are still true. They have always been true. Homes are more expensive where there aren’t enough of them, and everything else is a rounding error.

The bubble story obfuscates this truth. A truckload of empirical garbage has been dumped on the academy. None of the analysts noted at the beginning of the post can address this. If your boss at Bank of America asks you to estimate housing supply deviations, you can’t come back with a report that says, “Actually, we need to burn down the libraries and start over.” No individual researcher can do that. And so you have to try to build a model which sits on a foundation that insists that Figure 5 is what an oversupply of housing looks like. Your model can’t possibly be coherent, and yet if you recognize that, how could you possibly address it? You can’t.

But, what if those 3 million “excess” units during the global financial crisis were due to a negative demand shock rather than a positive supply shock? Instead of counting 3 million of accumulated overbuilding in 2010, we go back to 2006. In 2006, there was a sharp migration out of cities with high rents and home prices. At the rate we were building, we were in arrears on housing supply. Housing construction peaked, and so did household formation.

According to Figure 2, by 2012, household formation had declined by about 3 million households. Homebuilding declined over that same period by about 3 million units. In spite of that decline, the researchers measured about 2 million excess units, according to vacancy data and homebuilding data.

If there is any level of unsustainable demand trends, don’t you think it might be at the end of a massive foreclosure crisis? The most unsustainable demand trend was the negative one. Production had caved by 3 million units since 2006. We didn’t have 2-3 million excess homes in 2012. We had a shortage of at least 3 million homes, which was matched with an even greater collapse in demand that surely must eventually reverse.

The demand shock was so severe, it temporarily relieved Closed Access housing victims of their perennial pace of regional displacement, and for a few years, population in the Closed Access cities returned to low rates of growth.

In Figure 4, you can see that the housing-triggered outmigration was already returning by 2016 - well before Covid hit. If the Bank of America estimate of a deficit of 4 million homes is based on a homes per capita benchmark, then, as you can see in Figure 4, that benchmark probably would attribute more than 500,000 of excess units today to the Closed Access cities, while the rest of the country is in a deeper deficit. So, the 4 million unit number is probably understated, and we should add 3 million units to it to account for the shortage coming out of the Great Recession. And, as I discussed in the previous post, that is still surely an undercount.

Vacancies are Supply

Finally, I want to address the assertion that supply would have had to have increased by 300% to meet Covid era demand. I think these numbers are debatable, but let’s take it at face value.

I think the main issue here is that vacancies are a form of supply. You can’t take for granted that 5 million vacancies have dissipated over the past 15 years. The Fed researchers write, “Simulations of the estimated model show that housing demand drives short-run fluctuations in home sales and prices, while variation in supply plays only a limited role.”

Actually, as I paste that, I wonder if the authors consider their paper to be a refutation of the “excess supply” narrative. They discuss the 2008 bust in the paper as an example of how demand shifts were the key driver.

They limit themselves to a consideration of only the short term, and they mention the ability of supply to accumulate over time, but then I wonder what is the point? They write, “One implication of this result is that policies targeted at increasing supply, for example construction subsidies or zoning reforms, would have done little to cool the pandemic house price boom in the short-run.”

Well, sure, instituting zoning reforms in August 2020 was probably not going to maintain price stability. Zoning reforms in 2012? Of course! The authors acknowledge this, and extensively address it in the paper’s conclusion. So, considering the trend in vacancy rates in Figure 6, why write in the abstract, “First, we show that reduction of supply was a minor factor relative to increased demand in the tightening of housing markets during COVID-19.”? Why not write, “First, we show that the reduction of supply in the years after the Great Recession was an important factor relative to increased demand in the tightening of housing markets during Covid-19.”?

Add up the missing vacancies between 2007 and today, and it looks like it comes to about…300% of current production.

I have used these non-linear supply and demand charts before to think about housing. Basically each metro area has inelastic (vertical) supply when demand is less than the existing stock of homes or more than the willingness of the metro to approve new homes. And, in between those extremes, supply is pretty elastic. That’s one reason we get these big boom and bust price cycles in our supply constrained environment.

Vacancies are a big part of the shape of those supply curves. In cities that don’t approve enough housing, so that the supply curve is narrow, the vacant units have generally been bought up. In cities that approve enough housing, the wide supply curve is due, in part, to the high number of units that can be constructed each year, but also to a large number of units for sale or for rent that are available to soak up temporary shifts in demand.

In the 2000s, the supply curve depended a lot on what city you were in. That’s why the supply estimates are wonky. There were wide regional differences - so wide that they were driving migration patterns. There was no city that exemplified the narrative told by the aggregate national numbers. Today, the whole country has a supply problem and low vacancies. The supply curve has been narrowed everywhere, which is why an increase in demand had such large effects on prices.

If a demand surge has driven up prices, you’ve got yourself a supply problem. One way I would describe a lot of economic discourse over the past 25 years is “We have the housing supply of a population that is poorer than we are, so we need to make ourselves poorer to match our housing.” I’d say, “First, we show that reduction of supply was a minor factor relative to increased demand in the tightening of housing markets during COVID-19… Second, we estimate that housing demand is very sensitive to changes in mortgage rates, even more so than comparable estimates for home sales. This suggests that policies that affect housing demand through mortgage rates can influence housing market dynamics.” is an example of that discourse.

As I've been reading this series my initial thought has been "what a bunch of idiots...." but, mea culpa, I was one of those idiots for the better part of the past two decades. From 2008 and through the recession I fixated on the Case-Schiller graph, read Dean Baker, and bought into a narrative of a "housing bubble." I conflated the price gains in the metro Boston area with some set of immoveable forces and never made the connection to the supply constraints that had been building up the pressure for so many years. Granted, there were some price corrections during the Great Recession (which I benefitted from personally) but the trends driven by the chronic shortage reasserted by 2012. Now, like many people in this region I'm both "house rich" and "house poor"---a paradox consistent with a broken filtering process.

I think Kevin is unique in describing the constraints on mortgage lending as a major part of the current problem. It policies were rationalized, however, we would be unleashing new buyers into supply constrained markets in many metro regions. The best case scenario is more migration from super closed-access cities to lower tier urban areas that could rebalance some of the settlement inequalities. The worst case scenario is price run-ups for low quality dwellings that aren't sustainable for the new purchasing cohorts followed by a higher rates of default and foreclosure.