No, builders don't pull back until rents inflate

20th Century real estate markets were all about location, location, location. Prices in different cities appreciated at similar rates over the long-term. (That’s why the real Case-Shiller price index was flat for a century. There weren’t outliers.) Property values within each market shifted up and down with idiosyncratic changes in very local amenities. And, families sorted themselves across each market based on whether they could or would pay for those amenities.

Housing markets are a great example of the mysterious connection - the invisible hand - between micro- and macro- level economic activity. In the 20th century, household formation was highly cyclical. When things were going well, more households formed, and when they weren’t, fewer households formed. Developers kept an eye on regional trends, but they were mostly acting on local knowledge to match projects, locations, and idiosyncratic tenant demand. And, they were mostly vulnerable to either regional or shared cyclical downturns.

The qualitative questions about idiosyncratic project success and the unforecastable nature of cyclical risk made those the overwhelming factors driving unforeseen development outcomes and risks.

Yet, all that activity and all those distinct forms of risk added up to a marketplace where enough new homes were constructed over time to match demand for household formation, and no more.

In an average year, the housing stock grew by a bit more than 1%, with a lot of cyclical fluctuation, and the cycles tended to be shared across markets. Very local idiosyncratic changes can affect very local rent trends, but shared rent trends within a metropolitan area require a large supply impulse.

A 1% supply increase will generally be associated with a decline of rents around 2%. Before the Great Recession, a market like Phoenix was growing the housing stock by about 3%, annually. Builders weren’t metering new projects based on rent trends they expected because of supply trends. Oh, they always think there is too much supply and that it will bring down rents, but they think, “I have a great product for a great location, and all these other bozos are overbuilding a bunch of crap, and it’s going to screw up the market.” And, whenever markets contract for cyclical reasons, that is the reason they have teed up to blame for it. But, ex ante, none of them say, “Since everyone is putting up a bunch of crap, I should put off building my banger of a development.” They go forward with it because RE is always about location, location, location.

The slow-moving changes in market conditions that come from supply getting ahead of demand play out subtly and marginally in small deviations in returns over time that are dwarfed by other, faster-moving, higher scale factors.

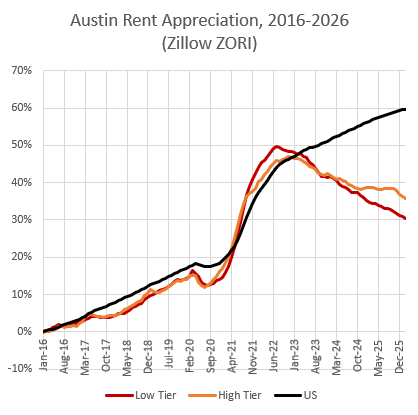

Austin is currently a great example of all of these pieces to the puzzle. A lot of YIMBYs are holding it up as a supply victory. And it absolutely is. Austin has been regularly growing its housing stock by more than 2-3% annually for more than a decade, and in the years 2020-2022, permits were issued amounting to about 4% annual growth.

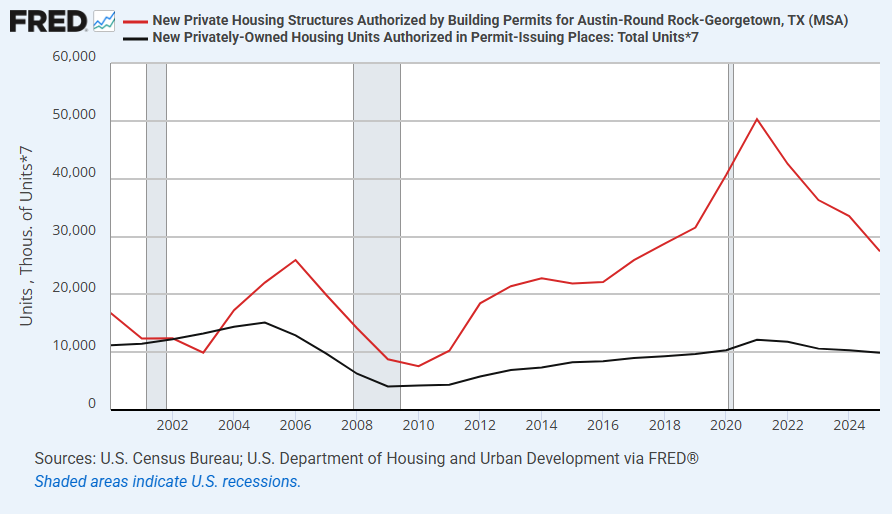

As Figure 2 shows, Austin permits have declined from those high peaks, but they are still permitting new units that amount to about 2-3% of the housing stock. That is still among the highest permitting rates in the country.

The average rent in Austin is down about 10% from its peak - about 16% adjusted for inflation. That implies an improvement in supply of about 8%. About 2/3 of that could be said to be from the spike in construction and about 1/3 is from a decline in population growth trends.

Austin is currently growing at about 2% annually. To reclaim that 16% in real rent deflation, Austin would need permitting to come to a standstill for 4 years, or move back down below 20,000 units annually for a decade. I will eat my hat if years’ worth of sub-20,000 unit permitting in Austin is associated with a return to previous real rent levels.

There are 2 versions of this story that I see. One is that builders definitely did not do this before 2008. They massively overbuilt, bankrupting the sector. And, they learned their lesson, and because corporations can just magically exercise market control whenever they feel greedy, they have essentially colluded since then to keep production low.

Obviously, the entire raison d’etre of my accidental career change into housing advocacy was discovering that even the premise of that claim is wholly wrong.

The other version of that claim is to imagine that it is a longstanding state of nature. The people that present it this way tend to accept the wrong conventional wisdom about 2008, and I don’t think I’ve ever heard anyone explain the contradiction. I don’t think builders overbuilt before 2008, but I don’t think the purveyors of these claims are exactly Building from the Ground Up disciples.

In either case, they start from a motte that is irrefutable and reasonable. Developers only build when they can earn a profit. And they argue from a bailey that is layers of nonsense - that developers know precisely the returns they will earn on new projects; those returns are mostly determined by the market-wide rent trends which are determined by market-wide supply activity; rent inflation is required to justify the marginal project; and they communally meter that supply so that rent inflation is maintained.

It just shows how distant we are from functional housing markets that are operating from a stable equilibrium condition that some people could convince themselves today that metro area rent expectations are driven by supply and that suppliers meter their production to keep that trend rising.

It’s completely irrelevant to the process. Back when Levittowns were filling up the country, rent was regularly declining relative to the prices of other goods and services. But, today, everywhere from Detroit to Dallas has been accumulating rent inflation, so it seems plausible.

Ironies

As I see this story being told, the building cycle is a product of this collusion. Builders slow down when they see that rising supply would lower rent trends.

You could concoct a story from 20th century construction patterns that could make that seem true on a superficial level. Construction really did move up and down with a lot of volatility. But, it didn’t fluctuate idiosyncratically with local population and construction trends. Everywhere fluctuated together as the national economy rose and fell.

It would be amazing enough if builders were colluding at the city level. For them to collude at the national level would really be quite something.

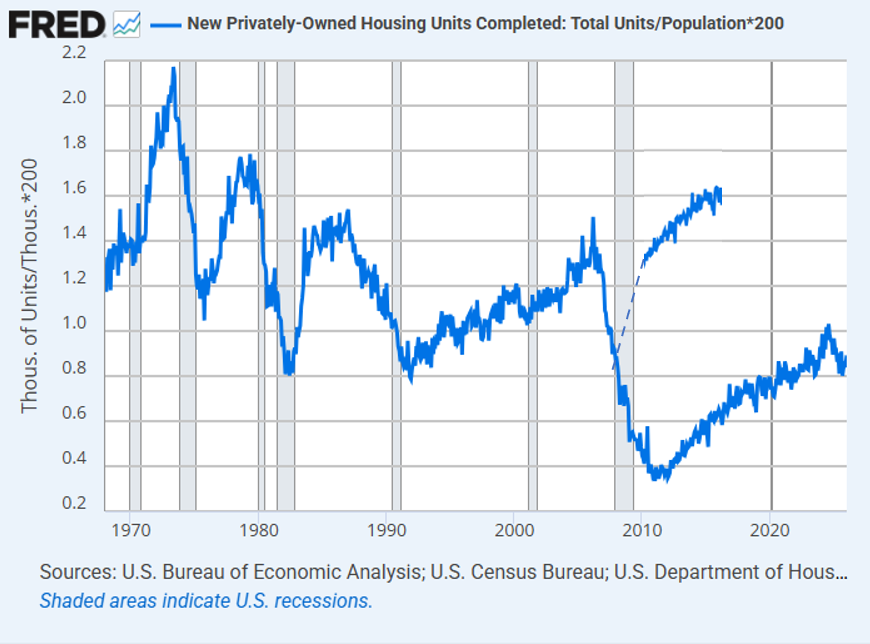

But, more importantly, when construction was volatile, rents were moderate. Those big cycles weren’t a disciplined industry rent inflation scheme. Rent inflation wasn’t a problem. Housing was filtering down nicely. A lot of new homes were built. Older homes were systematically transitioning to new residents with lower incomes than the previous residents. Household formation was greatly outpacing population growth. And rents were as low or lower than general inflation.

But, we haven’t had a building cycle for 40 years. The 1990 downturn was associated with the Savings and Loan crisis. Instead of a cyclical recovery, there was a relatively permanent loss of construction activity that slowly recovered over the following decade.

I suppose you could say that the first 2 years of the 2000s housing downturn was a normal 20th century building cycle. I have penciled in what a housing cycle would have looked like. And, heck, maybe if we had had a normal housing cycle in 2008, we would have had another one by now.

But, what happened in 2008 wasn’t a cycle. And, if you really look at it carefully, it doesn’t even look anything like the 20th century cycles. “Line go down” in a simple, naive sense is a part of a normal cycle, but cycles recover. Now, of course, all the mistakes and mythologies about the causes and consequences of “Line go down” have created a conventional wisdom where calling it a cycle is normal. But, it was a one-time shock to construction supply.

And, when we started recovering from it, we had lost the capacity to build a sustainable number of new homes.

And, this points to another irony about these “producer discipline” claims. For 35 years, the American residential construction market has been on a very linear, regular line with a slight upslope, with one gigantic gash in the middle of it. A Sisyphus market. Regularly, completed homes in a given year are predictably within about 100,000 units of how many were completed the year before, because the industry is slowly regaining capacity.

There is no 20th century-style volatility, today. If we assume steady demand conditions, an additional 100,000 homes should lower trend rent inflation by 0.1%. Millennials have never experienced a single time when the supply of new homes had shifted enough to change anyone’s expectation of rent trends at any scale that any developer would bother to add to a scenario analysis. Supply conditions have been constrained permanently for decades. This isn’t market discipline. These are scars. We are recovering from deep shocks.

And, there is one final irony. While the 20th century data could fool you into thinking that the building cycle was a “producer discipline” cycle, 21st century data will not. First, because we don’t have building cycles anymore. And, furthermore, while rents were flat in the 20th century, there is no reason to expect them to be flat today.

In cities across the country, land prices are inflated. They are inflated, and there is no mechanism that can keep them inflated when construction capacity does finally reach a level to bring rents down.

In the 20th century, the 16% drop in real rents in Austin would have reversed, because, as a consequence, potentially developable land on the edge of Austin would have been worthless. But, today, the 16% drop is sustainable because the land on the edge of Austin was inflated and is only less inflated now.

Since the rent inflation was imposed on builders by the consequences of the massive policy failures of 2008, it has accumulated while supply has been inadequate, in spite of their preference to have built millions more homes over the past 20 years. Now that there are regions where construction can reach a level to reverse that rent inflation, builders will keep building and rents will decline until land value isn’t inflated any more.

Of course, that only applies to cities like Austin, where building more homes is legal.

The colluding builders thesis is about to meet reality. It already has in Austin.

You say that "Millennials have never experienced a single time when the supply of new homes had shifted enough to change anyone’s expectation of rent trends at any scale that any developer would bother to add to a scenario analysis" but you also describe how rents have fallen in Austin and how the situation will not automatically reverse. So, wouldn't a developer we wise to add this supply scenario analysis to their underwriting?