Hsieh, Moretti, Shiller, and the Rest: Part 2

Robert Shiller, the free market fundamentalist

In Part 1, I wrote that the high incomes and high costs of some of our dense cities don’t really require an especially high level of productivity or agglomeration value. The conceptually complex analyses of agglomeration economies, urban productivity, and heterogenous migration are mostly a diversion into, at worst, trivialities with respect to the issue of rising housing costs, and at best, second and third order effects of housing obstruction.

The key piece of evidence about the costs of urban land use regulation should be the long term rise of rent inflation and decline of real housing consumption. Different relative real wages between cities is largely downstream of housing constraints.

Using CPI, rent inflation since the 1960s has accumulated to 60% (blue line), lowering incomes by more than 10% (red line), even after housing consumption has been pared back by 20% (black line).

The “superstar city”, “agglomeration economies” story is a story about permanently high housing costs. If high housing costs are permanent, then Figure 1 should be its narrative core. Economic rents, not productivity. That isn’t to deny that some expensive cities might be relatively productive. But productivity isn’t the important causal element.

There is also another very popular story about high housing costs - the bubble story. And, that story is a contradiction of the productivity story. That’s a story of temporarily high costs. However, it shares its most important error with the productivity story. It fails to focus on the economic rents that raise housing rents that are the key cause of high housing costs. The agglomeration researchers focus on productivity and the bubble researchers focus on price phenomena, but permanent, regressive rent inflation is the fundamental source of high aggregate residential real estate valuations.

The productivity story at least allows for high rents, even if I think it confuses the cause. The bubble story contradicts the evidence. Here, I will use Robert Shiller - maybe the bubble story’s most famous proponent - as the touchstone. I haven’t written much about some aspects of this for years. I think updating the analysis to post-Covid markets will be illuminating. I find the conceptual basis for Shiller’s famous real home price index surprising.

In 2015 (!) Shiller penned an article in the New York Times about the housing market, titled “The Housing Market Still Isn’t Rational”. And, his main complaint (in 2015!) was that housing prices can become cyclically inflated because there isn’t an easy way to short housing prices like you can short corporate equities or other traded securities. The article begins:

Home prices have been climbing. They have risen 27 percent nationally since 2012, even more in places like San Francisco. But why worry? If you accept the efficient markets theory — and believe that real estate is an efficient market — then these prices are based on “new information,” even if you don’t know what that information is.

The problem with this kind of thinking is that the efficient markets theory is at best a half-truth, as a voluminous literature on market anomalies shows.

Did I mention that this was in 2015 (!)? By the way, this is a great example of the behavioral bias of behavioral finance. Was there a single neuron in that Nobel Prize winning brain willing to consider that maybe home prices in 2012 had been unsustainably low? That prices in 2015 weren’t rising based on “new information”, but rather were returning to an equilibrium that had been upset by a credit shock?

Why was 2012 the benchmark?

Especially in housing, behavioral finance researchers and skeptics of efficient markets almost always benchmark to market lows to explain how biased markets or market participants are.

Figure 2 shows relative price/income levels in 2 hypothetical ZIP codes in Atlanta, one with average income of $40,000 and one with average income of $191,000. If the Nobel Prize winner for spotting market inefficiency can’t find the disequilibrium here - and treats its peak as a benchmark instead, no less - what hope do any of us have?

He writes:

Markets without the possibility of making these negative bets will be inefficient. That’s because if it is not possible to short, the smart money can do no more than avoid holding an overpriced asset. Canny traders are forced to sit on the sidelines, and watch in futility as prices decline as they expected. Without short-sellers, there is nothing to stop a group of ignorant investors — who get some ill-conceived idea that a certain investment is just terrific — from bidding up prices to extravagant levels. In the housing market, that poses an enormous problem.

Did I mention the date of the article?

The following paragraph exists. It was typed up, edited, printed and shipped.

In San Francisco, for example, we found that while the median expectation for annual home price increases over the next 10 years was only 5 percent, a quarter of the respondents said they thought prices would increase each year by 10 percent or more. That would mean a net 150 percent increase in a decade. These people are apparently not thinking about the supply response that so big a price increase would generate.

One thing that doesn’t appear in that article, and also doesn’t appear in many of the academic papers about the “housing bubble” of the 2000s is the word “rent”. And, when you think about it, it would actually be very difficult to construct a model that found housing markets to be efficient and rational without ever uttering that word.

By the way, I was flipping through Shiller’s book about the housing bust, called “The Subprime Solution”, for mentions of rent. (I don’t see any.) And came across this astonishing sentence about home prices after 2007. “The rocket has fallen—and the bust after the peak was not explainable by any significant change in the other variables.” The variables he tracks are building costs, population, and interest rates. Of course, mortgage originations to borrowers with credit scores below 760 were in the process of permanently dropping to a quarter of their long-standing market share as he wrote that. It seems like a variable someone writing a book with “subprime” in the title should notice.

This is a common problem with “bubble” literature that usually purports to identify inefficient or irrational markets through a process of elimination of rational or efficient causes of price trends. It is possible - in fact, it is so common as to be cliche - to engage in “process of elimination” conclusions about home prices without having thought to consider the possible importance of a permanent 40 point change in the median credit score on originated mortgages after 2007.

Sorry. A second digression. In an earlier article at the New York Times, Shiller made this comment. It’s not an unheard of sentiment, but it is stunning to see it come from a leading economist. “(S)ince 1890, the average appreciation of inflation-corrected home prices in the United States has been only a third of 1 percent a year. That’s why housing hasn’t been a great investment.”

You can see how deeply his neglect of rent goes here. The market he describes is the description of a functioning housing market. Home prices shouldn’t rise much more than general inflation. How could an asset not be, as a general rule, a great, or at least a good, investment in that scenario? This seems to suggest that barriers to entry are required in order to induce rational investment into housing. This is economic illiteracy.

Rational investors in the provision of a basic human need will not fail to find a market equilibrium price for profitably meeting that need. That will be hard to understand if “rent” is not in your dictionary.

The return on housing investment in that scenario is entirely a product of rental value. Prices in a unemcumbered market will be tethered to the cost of construction. Rental value must settle in that scenario at the level required to make housing investment marginally reasonable. Rent is the thing that makes the market. Without considering that, you can say nothing about the relative returns on housing investment in a functional market. N.O.T.H.I.N.G.

It would be like saying you should never invest in new bonds because you invest $100, and when they mature, they just pay you back $100. I try to rein in my exasperation in these posts. I really do, though I fail at it. I recognize that being exasperated isn’t a winning style. Shiller is sometimes exasperated in his writings, and of course, I don’t think it reflects well on him, because he’s wrong. But, folks. I’m exasperated.

Anyway, since rent isn’t in his field of vision, he tends to talk about how new supply will bring prices back down to the cost of construction rather than bringing rents back down. If we lived in that world, where high prices lead to new supply, that would be fine.

That’s basically his problem. We don’t live in that world. Since rent isn’t in his field of vision, he literally can’t imagine the world we actually live in where rent keeps going up.

It’s ironic that he has been crowned as the antidote to Eugene Fama’s market fundamentalism. Shiller’s housing model basically starts with Fama, removes any empirical reference to earnings, then claims there is no rational basis for price fluctuations.

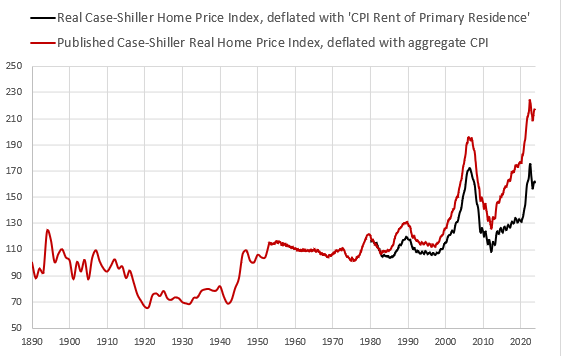

So, when he deflates his real home price index, he doesn’t deflate it with rents! He deflates it with general CPI prices. Because in the spherical cow world his window opens up to, higher prices always draw in new construction and return to neutral. The same applies to rents, if we must speak of such things. So, the accumulation of 60% rent inflation over a 50 year period isn’t something Shiller thinks he needs to adjust for! It doesn’t exist, as far as he’s concerned.

The Case-Shiller real home price index makes no accounting for an accumulated 60% in excess rent inflation!

Figure 3 compares the published real Case-Shiller index with the real Case-Shiller index if it was deflated with rent inflation instead of general prices.

By the way, I haven’t corrected the CPI rent number here for the recent problems of lagging market rents. That spike in the rent deflated measure in 2022 is mostly a product of that data lag. Once the CPI measure catches up, the number will probably settle at around 150.

This is only half the story. I’ll save more for the next part in the series.

How long do we need to wait for that price-moderating supply to land in San Francisco? Does Shiller think that’s what happened in 2008? While he’s chiding those rubes who haven’t considered all that supply that’s going to hit the San Francisco market, city supervisors are sprinting down to the planning department to declare, “We don’t need market rate housing! We only need affordable housing! Get thee out! Oh, and also the shadows. No shadows!”

The differences between cities is an important part of the rest of the story, to follow in the next post.

In San Francisco, for example, we found that while the median expectation for annual home price increases over the next 10 years was only 5 percent, a quarter of the respondents said they thought prices would increase each year by 10 percent or more. That would mean a net 150 percent increase in a decade. These people are apparently not thinking about the supply response that so big a price increase would generate.--Shiller

This is an astonishing comment to make.

Oh, maybe those city residents knew exactly what the supply response would be. You see, they were there, on the ground in SF, while Shiller was pontificating from New Haven.

I sometimes think the words "structural impediments" have been banished from the macroeconomics profession. Theory is so much more fun.

The nice thing about macroeconomic theoretical debates is no one is ever wrong.

Interesting stuff!

Being in land development I always start there and try to move out. Austin where I live and do some business seems like a reasonable example. This is simple, but indicative:

+ Revenue

Units X $/Unit

- Construction costs

- Operating Costs

- Financing Costs

Equity

Debt

- Land

= Profit

If developer profit goes up, you can be sure that landowners and contractors grab a share. Using a little algebra one can move the items to one side of the = sign or the other.

All theory aside what happened in Austin is construction costs were low from the Great Recession, density (the number of units per project) increased, rent per unit increased, financing costs decreased, and exit cap rates decreased. The intermediate result was developer profits soared.

Next land prices and construction prices rose, cap rates stayed the same, financing costs stayed the same, developers could still push rents, and profits continued to be high. Basically, rents covered the new costs.

Land prices and construction costs continued to rise, cap rates stayed low, and the ability to push rents kept profits up. Land and construction could not continue to rise unless cap rates stayed low and rents rose. Construction would have stopped.

The interesting, maybe crazy, thing is that in the city limits Austin added 60,000 additional households making over $150,000, roughly twice the previous median, in the 5-year period from the of 2017 through 2022. The median income increased by $20,000 during that period. The ability to push rents based on the incomes of the additional households played a big part in what happened.

I don't think it was agglomeration or productivity. It seems like development fundamentals, demographics, and the Fed. I guess agglomeration could have caused the 60,000 households to show up, but that seems like reaching. The Pandemic is more likely.

My hunch and it's only a hunch is all of this is now baked into the cost structure (and rent structure) here and without a major economic event it will not change. It may move a few points, but Austin will stay high-cost which means it will stay high-rent.

Kinda seems like a chicken and egg thing.