Housing Permits and Displacement

In “Shut Out”, I wrote that at the top of the 2000s cycle, “The rate at which Nevada, Arizona, and Oregon were building homes just to accommodate refugees from San Francisco and Los Angeles was higher than the rate at which San Francisco and Los Angeles are even capable of building in total.” The same was basically true of Florida for Boston and New York City.

I think, because economists have been too enamored of their agglomeration and productivity stories, we have this weird norm where experts in urban economics have these conversations that strongly imply that our most stagnant cities are under pressure from unusually high demand. The general public accepts this as empirical truth even though it is far from it. Of course, New York and L.A. are expensive. It’s only natural. So many people want to live there. If they built more homes, they would just be expensive and crowded, because they’re so popular.

Below, I’m going to compare home building rates and domestic migration rates for a few cities. They may not be surprising for EHT readers, but I suspect they would surprise most layfolk and maybe even some economists.

First, Figure 1 shows annual permits, nationally, for the US. I have included the actual estimate of permits as a percentage of the occupied housing stock. But, I don’t have annual estimates of the housing stock for the metro areas. So, I am using a household size estimate of 2.6, which, as you can see here, is a good estimate for the entire period. There are some differences in household size between cities, but this will do for the purposes of this post.

Domestic migration nets to zero, nationally, so annual new homes reflects household formation, net foreign migration, change in vacancies, lost units, and change in household size.

Fewer permits because of less household formation and less migration reflect weak demand.

Fewer permits because of declining vacancies or rising household size reflect weak supply.

More permits because of lost units reflects very weak demand.

So the reasons for a rise in permits are a bit of a muddle.

Before the Great Recession, those categories led to demand for new homes of 1.5% annually, or a little more. Then, it dropped to about 0.5% annually after the crisis, and has risen back to a bit over 1% since then.

The relatively low amount of building after the Great Recession, nationally, has been generally a combination of weak demand (low migration and low household formation) and weak supply (declining vacancies and rising adults per household).

So, how do some metropolitan areas compare?

One thing I have done on the charts below is always show domestic migration as a positive. When net domestic migration is negative, it is red. When it is positive, it is green. So, for cities with positive domestic migration, the number of homes required to meet all the categories described above is the difference between the number of permits and the number of inmigrants. For cities with negative domestic migration, the number of homes required to meet all the categories described above is the sum of the number of permits and the number of outmigrants.

Sorry if that’s confusing, but in the Closed Access cities, I wanted to be able to easily compare the number of displaced families with the number of newly housed families.

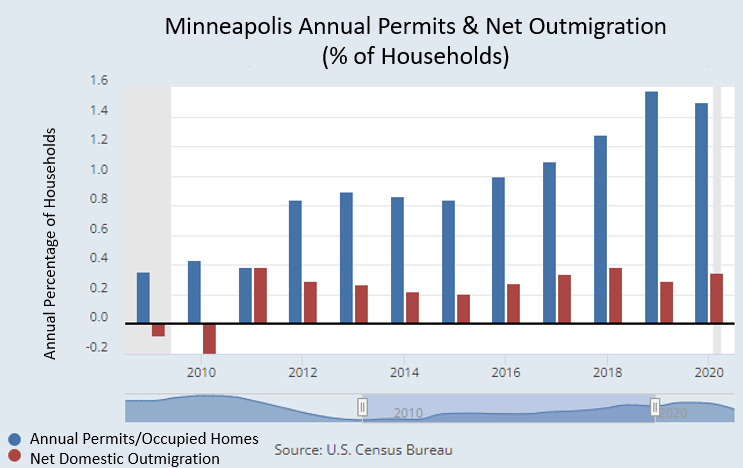

Minneapolis

The migration numbers aren’t really updated far enough to reflect any recent YIMBY actions there. I chose Minneapolis because I wanted to see a city that is neither a slow growth rust belt city nor a fast growth sunbelt city. As you can see, Minneapolis has slightly negative net domestic migration. It’s pretty close to neutral in every way over this period - both in terms of permits after migration and in terms of rent inflation. From 2011 to 2020, the US averaged permits of about 1% of occupied units. Cities tend to run a little higher than that because of the general tendency toward urbanization. Minneapolis permits after domestic migration averaged about 1.3% of the occupied stock annually during this period.

Chicago

Chicago is basically an example of a rust belt city - a city that isn’t building a lot of homes because demand is low. You could say of Chicago that other places are building more homes for Chicagoans than Chicago is, but it isn’t the lack of homes that is motivating those moves. Permits plus domestic outmigration averaged 1.4% of occupied units in Chicago.

Phoenix

How about Phoenix? (Here, I should mention that the migration numbers here are 5 year estimates. Those high numbers in 2009 and 2010 for Phoenix are just still reflecting the high rates of inmigration before 2008. You can see here how devastating the crash in domestic migration was, but keep in mind that the bars for 2009 and 2010 don’t reflect migration from 2009 and 2010.)

Before 2006, Phoenix permits ran at about 3% to 4% of occupied units annually, and domestic inmigration was much higher. After the Great Recession, permits fell to about 0.5%, and have only recently moved back above 2%.

From 2011 to 2020, Phoenix permits minus net domestic inmigration are an outlier. The annual average was only about 0.6% annually. This was mostly due to constrained local supply. Vacancies started the period very high and have ended quite low. And, rent inflation in Phoenix has been the highest of these metropolitan areas. Since Phoenix before the Great Recession was a particular outlet for middle class migration and affordability-motivated migration, the mortgage shock has had an especially negative effect on Phoenix housing supply.

You can see that in the last couple of years, the difference between new homes and inmigration has been more normal - around 1.2% or so. That is because the vacant units have been sucked up.

This is why Phoenix is one of the hottest markets for the newly ascendent build-to-rent market. There is a lot of pent up demand in Phoenix, and it requires corporate buyers. I expect that before the new build-to-rent supply can improve conditions much, there will be a lot of local opposition to try to squash it.

Austin

Since Austin has higher incomes than Phoenix, the mortgage shock didn’t collapse it as much. Construction remained higher than 1%, even in the depths of the crisis, and it has risen to more than 4%. Curiously, the rate of building in recent years in Austin appears to have moved quite a bit ahead of migration. Migration was strong into Austin after the Great Recession, so maybe the strong excess construction in recent years is just catch-up growth from the tough years after the Great Recession.

Rent inflation since 2015 in Austin has been lower than average, suggesting that it is catch-up growth, and that Austin is not only building enough to meet demand but even to heal some of the wounds of the post-Great Recession shock.

As always, Austin is the sole superstar.

Seattle

Seattle is above average. Domestic migration is still, just barely, positive. Seattle, just like all the other cities, has an annual permits minus migration rate of about 1.2%. You should be noticing a pattern here. There are no special cities (except Austin). None of these cities shows any particularly strong signs of unusually high foreign migration or any other source of demand. Some build a lot, and people move in. Some build a little, and people move away.

Seattle is a bit above average - just on the other side of “average” from Minneapolis. However, Seattle could be similar to Austin. If they permitted new homes like Austin, homes would be more affordable. Rent inflation since 2015 has been higher in Seattle than any other city in this post, except for Phoenix. Seattle is still in that middle ground. Housing is constrained enough to be expensive, but not quite so constrained that there is a perpetual flow of net displacement to other regions.

Now for the bad guys. The Crapitol cities.

San Francisco

Demand in San Francisco is tied to the tech sector, so its numbers are a bit all over the map from year to year. Whereas Seattle runs a bit above 1% housing growth after migration pretty regularly, San Francisco has run anywhere from about 0.6% to something more in the 1.5% range, averaging about 1.2%.

Recently, it has been back in the condition that it had been in before the Great Recession. There are more families displaced from San Francisco annually than there are new families housed there. And, unlike Chicago, this is because of a lack of housing and high costs.

Rent inflation in San Francisco, Los Angles, and New York City hasn’t been particularly high since 2015. That is because they are well past the Seattle phase of obstruction. There are thousands of locals on the edge of a precipice. Any marginal increase in rents will displace them. In Seattle, there are still more families with the capacity to choose poorer living standards to remain in Seattle one more year.

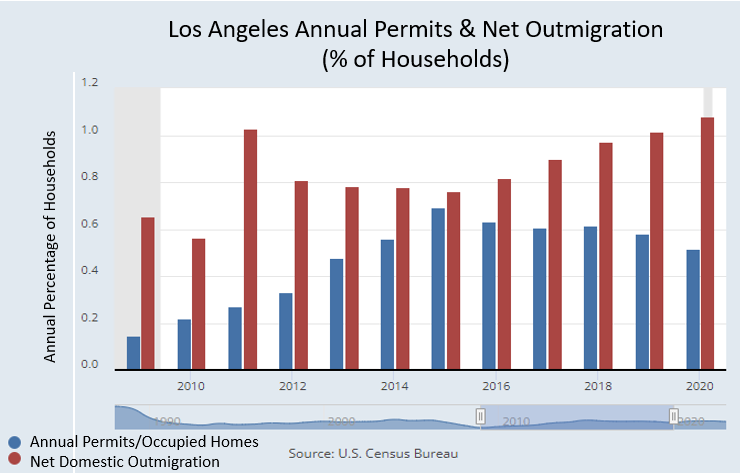

Los Angeles

Los Angeles, on the other hand, is forever in the condition of puking out more displaced families each year than it houses. The total of permits plus outmigrants each year averages about 1.4% of existing households. Again, about the same as the other cities, suggesting that there isn’t much of a difference in demand among the cities in categories like foreign migration.

It could very well be the case that if L.A. built at the rate Seattle does, it would have neutral or slightly positive net domestic migration. Really, the primary reason to think otherwise is the set of biases that comes from the path dependence of economists having the agglomeration story at the ready to explain Los Angeles’ high costs when a lack of supply became the overbearing driver of these trends.

New York City

New York is our modern-day Johnny Appleseed - the Big Apple that gets replanted in Florida a little bit more each year. Like L.A., it is in a constant state of displacement. Every year, on net, more New Yorkers get new homes in Florida than in New York.

New York comes in a bit high on the annual permits plus outmigration number, at about 1.8% annually. Maybe it has a bit more foreign migration than the others, but rent inflation from 2015 until Covid in New York City was the lowest of these cities. That suggests that it isn’t because of higher demand. Maybe it is, and, just as in L.A., the pre-existing stress is so high that it just doesn’t take much more rent inflation to trigger outmigration. In any case, the difference is, again, minor - fractions of a percentage point in terms of annual flows.

Conclusion

The long and the short of it is that, if San Francisco, New York City, and Los Angeles built as much as, even, Minneapolis or Seattle, they would not have negative domestic migration. Of course, the question remains, whether that would be the result of more inmigration or less outmigration.

According to the American Community Survey, in their current condition, they do not have unusually high inmigration. They have unusually high outmigration.

Furthermore, think about the demand elasticities on the margin. The displaced residents currently tend to have lower incomes that the remaining families. Homelessness is increasing because for some of them the cost of being regionally displaced is so high that they are willing to go without shelter to avoid it. As I have described it, they are paying for the idiosyncratic endowments of a personally valuable location (jobs, history, grandparents and children, social services, etc.). They are highly motivated to stay. The newcomers outbidding them for homes are operating on the margin. They value those cities aspirationally, and in order to arrive there, they are giving up some square footage, taking on a longer commute, etc.

The differences in demand elasticity on the margin leading to 1% net annual outmigration are likely significant. I think it makes sense to assume, lacking further information, that the vast majority of new homes in the Closed Access cities would be associated with less displacement.

In other words, if 1% net outmigration from L.A. this year is the net of 2% inmigration and 3% outmigration, the difference between flat rents and 5% rent inflation probably doesn’t matter much to those newcomers, but it is devastating for the leavers. Out of the whole country, about 250,000 residents will move into L.A. this year. That number isn’t going to change much because of 5% rent inflation. As I said, they will drive a little further, live a little leaner. They will have marginal choices. The 375,000 families moving away are generally moving away because they have bent all that they are willing to bend, and that 5% broke them. They choose regional displacement because they are out of marginal choices.

The migration into and out of Chicago does not share this dichotomy of conditions.

Great reality check.