Follow Up to Multiple Binding Constraints Make Housing Analysis Hard

I have one additional chart that might help explain my point from the previous post.

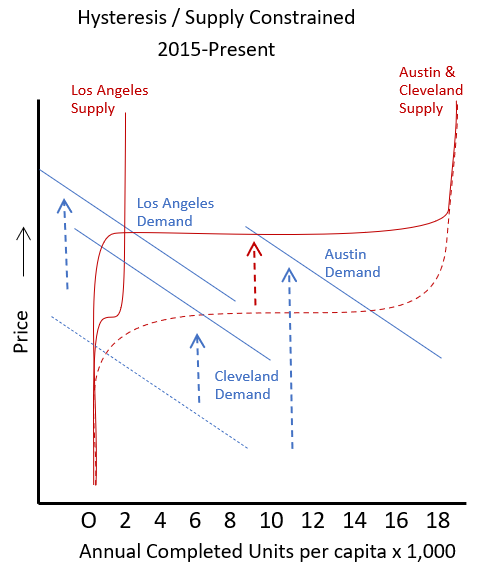

Figure 1 is from the post.

I wrote:

Over time, demand for household formation pushed rents higher until demand for purchasing homes moved back up to the flat part of the supply curve. But, as I discussed in a recent post, I think that the American housing construction market has been in an almost constant state of hysteresis (a limit to how quickly production can recover) for the past 30 years - production this year can only rise so far from production last year - briefly interrupted by the collapse after 2008.

The quantity of new home completions has been unsustainably low for that entire time, so that rent inflation has been elevated. But, the sector could only increase construction capacity by about 0.1 completions per 1,000 residents annually. So, nationally, the demand curve is at the vertical right end of the supply curve.

But, the way that plays out at the metropolitan area level is that rents inflate, and home prices inflate, motivating builders to pay more for land and materials. This pushes the flat part of the supply curve within every metropolitan area higher. Input inflation directs materials to the fastest growing cities, and the quantity constructed is correlated with local demand, much like it is during normal times.

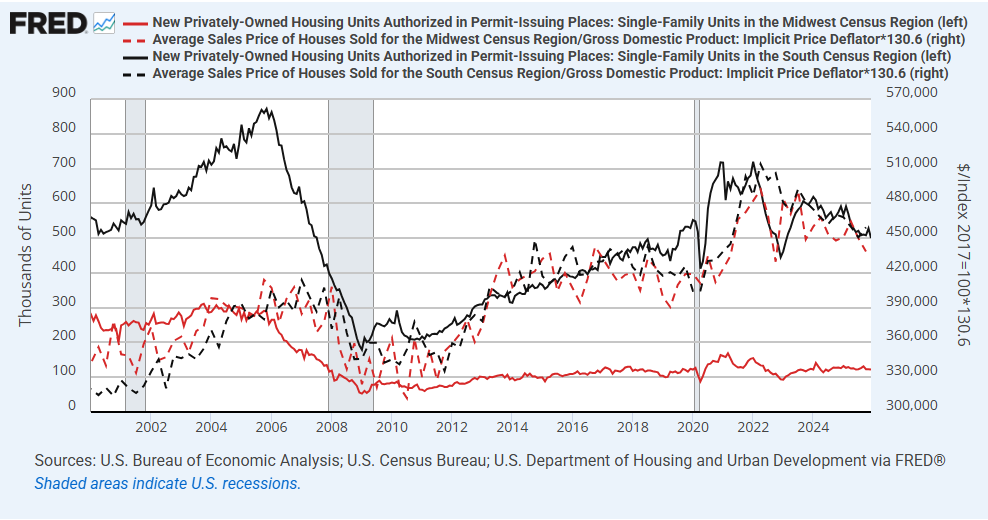

Figure 2 compares the prices of new homes (dashed lines) and the number of permits for single family homes (solid lines) in the South (black) and the Midwest (red).

Generally, economists discuss supply elasticity. And, using conventional supply and demand models, it looks very much like supply in the Midwest has become extremely inelastic. (It has! Look at Cleveland in Figure 1!)

On the other hand, builders in the Midwest will say, “No you don’t understand. It’s the costs. Regulations add cost and inputs have become more expensive. I would build homes like crazy, but they don’t pencil, because costs are too high.” (They are!)

Both groups are correct, but they are arguing from a confused perspective, which Figure 1 is meant to clarify.

The reason there hasn’t been a supply response in the Midwest to a 20%+ rise in home prices is that builders in the South bid up the prices of inputs until those inputs are directed to markets in the South. That moves the flat part of the supply curve higher in the Midwest until markets in the Midwest are stuck at the left vertical end of the supply curve.

According to my Metro Area Analysis packages, some cities in the Midwest are even getting to a place where home prices and rents justify paying a premium for land. If builders aren’t increasing production because costs are too high for projects to pencil, then how could home prices be signaling higher land prices?

The reason is that builders in the South are bidding up the cost of inputs until the cost of new homes are too high to build, even if the prices of existing homes are elevated enough to justify higher land costs.

I think, for developers who understand this, and who pick the right markets, there are probably markets where this confusion and the lack of activity being created by these conditions, are keeping land values low. Agricultural land on the edges of these cities is probably selling at a low premium, and when input prices normalize, that land will be worth tens-of-thousands of dollars per home because, at normal costs, the prices of new homes on those lots will be inflated by the 20 year supply bust. Production in those cities will rise, and those who put themselves in a position to build on land they own will be printing money. And the boom will last until it reverses 20 years of inactivity.

That’s the market side of this.

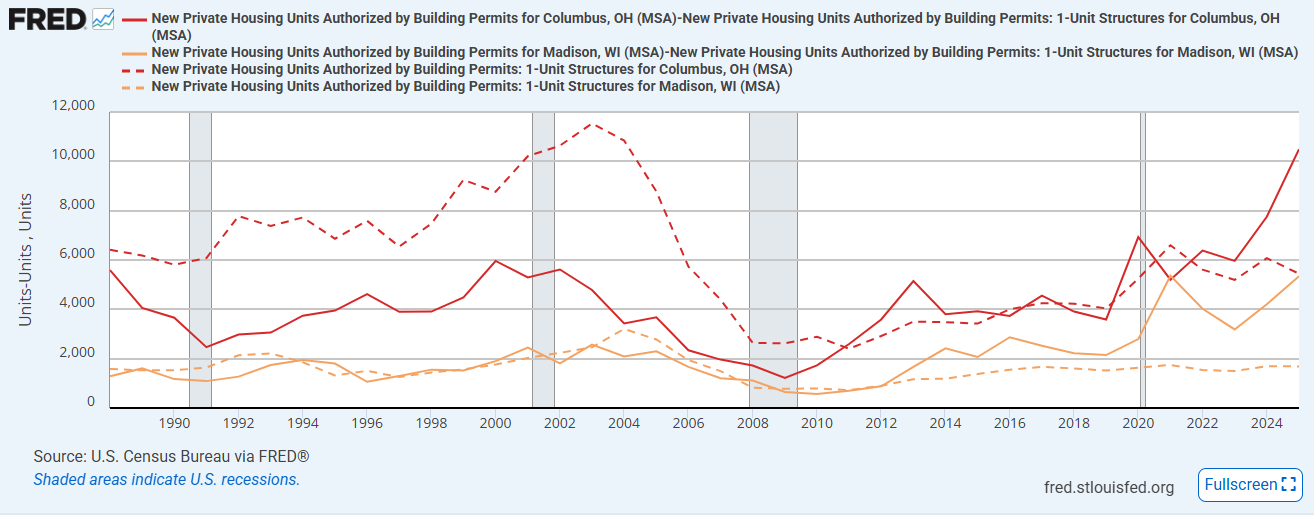

On the policy side, it means that both the “high costs” group and the “inelastic supply” group are arguing from reasonable facts with a confused framework of what is happening. Cities in the Midwest could have increased supply through upzoning. There are lots in most cities where apartments could be built profitably if the law allowed. In Figure 3, Columbus, OH (red) and Madison, WI (orange) have been able to increase multi-unit (solid) construction to make up for flat single-family (dashed) construction.

Ann Arbor has recently seen an uptick in permitted apartments, too. I’m sure it’s no coincidence that they are all college towns. In Arizona, you can build mobile home parks and apartment buildings for retirees. It’s hard to build them for other people because the point of zoning was to socio-economically segregate municipalities. The Midwest has the same problem that Los Angeles and New York City have. It’s a collective action problem. Everyone is housing poor together because every city opposes housing in order to keep away families that are relatively poorer than the existing residents are. Zoning was the method for accomplishing it that survived legal appeals, to all of our detriment.

Upzoning wouldn’t have solved our national hysteresis problem. Those new apartments in Madison came at the expense of some single-family homes in the Phoenix suburbs. But, again, the way to think about all these factors is with Figure 1. Upzoning in Madison increased demand in Madison which pushed demand against the right end of the national supply curve, which raised the flat part of the supply curve in every local market until total quantity demanded was held at the national capacity.

There are several local and national binding constraints that basically put local supply into binary elastic or inelastic conditions.

Before 2008, zoning was the constraining factor for new homes in the Midwest, but it wasn’t binding. A vertical multi-family supply curve and a flat single-family supply curve added up to a flat supply curve in general. There were families that could have used apartments in some cities, but enough single-family homes could be built on the edge of the cities to keep affordability in check.

After 2008, the mortgage crackdown and hysteresis made both single- and multi-family supply in the Midwest inelastic (vertical in the charts). Single-family was at the left side vertical supply curve and multi-family was at each market’s vertical limit on the right side. So, the total supply curve became vertical.

Today, under conditions of hysteresis, increasing the supply of inputs that are at a binding capacity will move the national supply curve to the right and the local supply curves down.

Upzoning and regulatory reforms would greatly increase construction in Los Angeles. Lowering the price of lumber probably would not. And, under current conditions of hysteresis, the new homes in Los Angeles would raise the supply curve in other cities.

If mortgage rates decline, the demand curves in each city will move to the right, but under current conditions, that will just raise the supply curve in each city to settle at a higher priced equilibrium. The same is true, currently, of loosening lending standards. But that is only temporary. In fact, in the long run, more and cheaper borrowing moves Los Angeles up its vertical supply curve, but it moves practically every other city to the right along its flat supply curve. During our recent housing “bubbles” the problem was that the outflow of families from cities like Los Angeles pushed some other growing cities far enough to the right that they hit their vertical supply curves.

In the long run, mortgage access increases the quantity supplied at the given market price, so it lowers rents.

So, it’s a bit of a policy minefield. There are good reforms that might temporarily look ineffective. I think we should still push for those reforms, but it will be important to know where evidence for or against any market or policy changes are dispositive or misleading, based on whether short-term or long-term supply curves are flat or vertical.

One important implication here is that we are still recovering back to a market equilibrium. Analyzing the housing market of the last 20 years as if it is at a stable equilibrium will give you garbage output. And, ironically, 20 years after a policy debacle meant to kill the homebuilder market in a few high-growth hot spots succeeded beyond our wildest nightmares, the housing markets of the Midwest will be the last victims to see recovery.

Recovery will be inevitable but the race to use new policy like banning the large scale landlord market to stop the recovery is on.

I like that this points to a healthy, friendly synthesis between our two viewpoints:

Regardless of what the underlying demand is for any given development style, increasing mortgage access can spur production and affordability in basically all market segments. AND, densification in the markets *I* prefer will enable healthy greendfield growth in the places where it’d be appropriate.

LA, for instance, is completely out of greenfield space. That’s why people moved to the Inland Empire. Ever-undaunted by the traffic congestion that horrifies and offends my every sensibility, they sprawled up against the literal mountains and hills, and cannot easily build new greenfield anywhere except on the other side of them.

But undoing the mortgage crackdown means more condos and missing middle get built in LA.

STL by contrast, and likely Cleveland from all I can tell, has mostly sprawled out to the mythical “1 hour commute” limit. The mortgage crackdown killed off most exurban development in STL (which I don’t personally mind), and rising prices forced an apartment boom in STL’s relatively permissive regulatory environment. That boom has run up to its regulatory limits, and housing is now going vertical. Thus, undoing the mortgage crackdown will enable a whole bunch of remaining densification that STL has left to do — and there’s a LOT of it left — which will in turn gently expand the practical 1-hour commute boundary, since there will be more dense and profitable uses of land further out from the city center.

NYC is an example of what happens when this process is allowed to go on long enough: the sheer density in the city forced its 1-hour radius to be incredibly dense as well, which means that its sprawl goes out WELL past a mere hour from Times Square. In fact, the sprawl limit is basically extended out to “an hour from any commuter rail station”, since those stations are built wherever there’s enough density to be profitable.

Either way, a lot of housing gets built because BOTH theories are correct: the mortgage crackdown is inhibiting a lot of demand in the middle and bottom of the market, and most suburbs (anywhere) are not currently dense enough to enable expansion beyond the current sprawl limits.