February 2024 Residential Sales

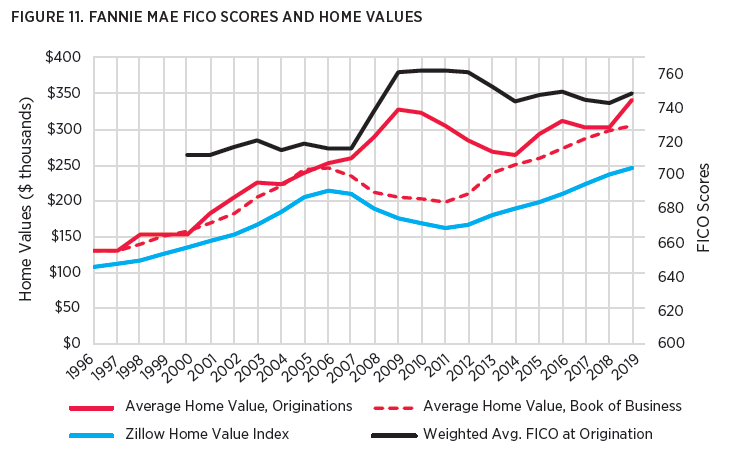

Before I get into this month’s residential sales update, I’d like to point out something that I think is pretty extraordinary. I have written about this a bit before. Figure 1 is from my paper revisiting the factors that changed home prices from 2002 to 2010. The point of this chart is that Fannie Mae had been originating mortgages to the same people (FICO scores were flat) in the same homes (the value of homes funded with new mortgages was the same as the value of homes that had previously been funded) from 1996 to 2007. The homes were getting more expensive, but the homes and the borrowers were the same. Then, from 2007 to 2009, they abandoned the bottom half of their borrowers (FICO scores jumped and loans only went to higher priced homes while homes with existing mortgages declined in value.)

I have become convinced over time that the entire $5 trillion wealth shock that came from the collapse in home values was due to that change in lending norms. We just collectively pushed working class homeowners heads under water until they stopped flailing. Meanwhile, Rick Santelli railed against the homeowners whose homes had no buyers anymore in 2009 and Occupy Wall Street railed against bankers in 2011 who hadn’t been able to offer loans to those buyers for 3 years.

The quarterly residential sales reports have some similar data for new homes. Figure 2 compares the average price of a new home getting an FHA mortgage (green), the median home price, estimated by Zillow (blue), the average price of a new home getting a conventional mortgage (red), and the Case-Shiller estimated home price (black, scaled to match the conventional home price in 2005).

These figures tell a similar story. It’s a similar story that you can see by comparing home prices in poor neighborhoods to home prices in rich neighborhoods. Rich neighborhoods flattened out in 2008. Poor neighborhoods collapsed.

Here, of course, the two measures of existing home prices collapsed by more than 20% from 2007 to 2012. The value of homes getting mortgages did not. In fact, FHA, much like Fannie Mae in Figure 1, moved up-market. The average value of a home getting an FHA mortgage after 2007 was much higher than the average value of a home getting an FHA mortgage before 2007.

Basically, you can see what would have happened to home prices if we hadn’t retracted mortgage credit. Prices of new homes that still received mortgage credit were flat. Prices of homes that didn’t, collapsed. Much more than 20% in many cases.

And, following that, for a decade, existing homes were cheaper than new homes, especially in affordable neighborhoods, so builders didn’t build any. Buyers (which were mainly landlords) who wanted low-tier homes bought existing ones. This has just recently changed because existing homes finally caught back up to new homes. So, landlords are starting to buy new homes.

Also, if the housing bubble could be accurately described as a period where loose lending led borrowers to take on mortgages that were too large to overpay for homes with unsustainably high prices, isn’t it weird that there was no decline in the value of homes being funded with mortgages? Just a massive decline in the number of mortgages issued.

One could argue that these measures are hard to interpret because there was such a large compositional effect. The average borrower in 2008 was very different than the average borrower in 2005. So, maybe the specific borrowers who were still borrowing in 2008 were buying cheaper homes than they would have bought on in 2005 while small borrowers disappeared. There is something to that, but the compositional shift is the problem.

February updates below the fold.

Keep reading with a 7-day free trial

Subscribe to Erdmann Housing Tracker to keep reading this post and get 7 days of free access to the full post archives.