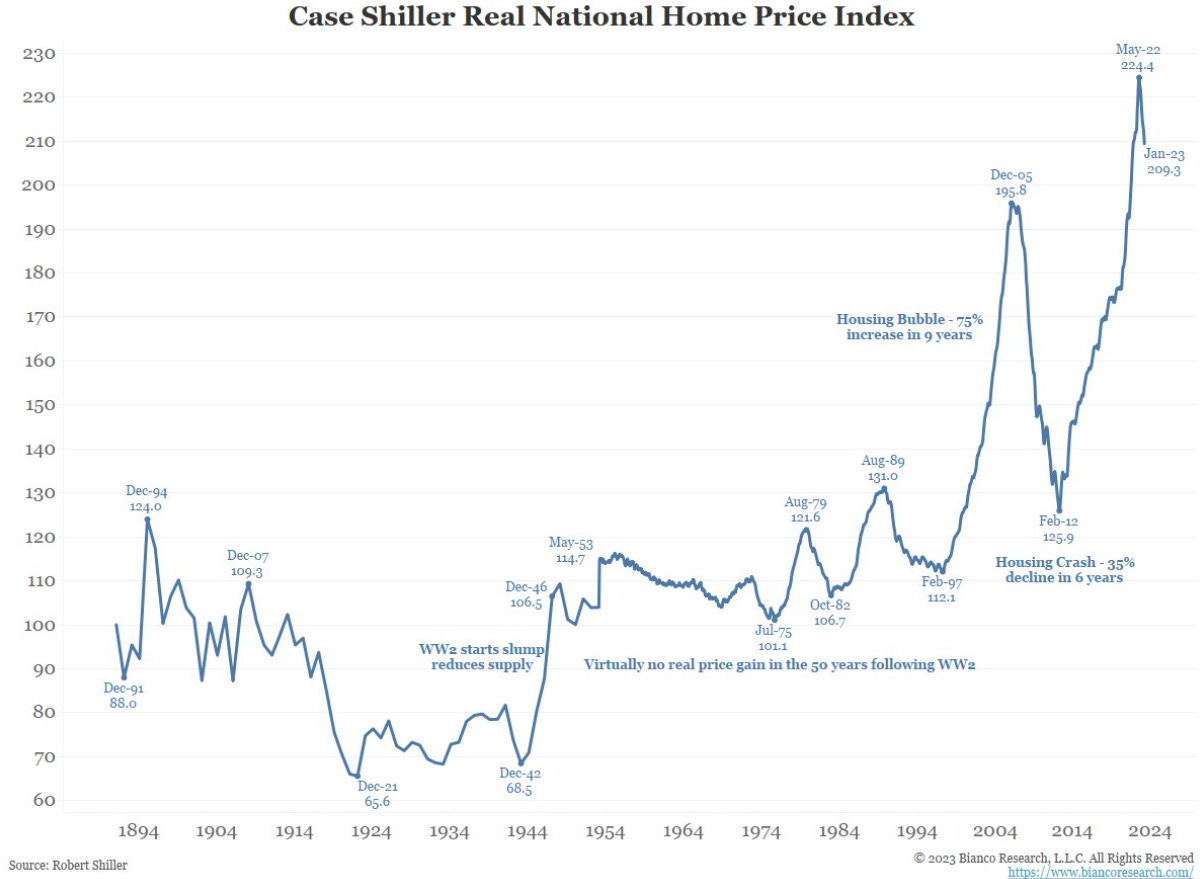

Case-Shiller and Filtering

Case-Shiller has a home price index going back more than a century. If you deflate the index with general CPI inflation, it looks like Figure 1.

Back in the 2000s, this chart was very popular. It was meant to show a bubble that was bound to revert back to the century old level.

Prices never returned to what was normal, and now, it’s higher than ever.

It turned out, it wasn’t really the story of a bubble. It was a chart about a housing shortage. It was Figure 2, in real life.

I suppose one could be forgiven for thinking in 2005 that it was a picture of history’s craziest housing bubble. But, that interpretation will be increasingly difficult as each each iteration of new “bubbles” keeps turning on higher and higher highs and lows.

Unfortunately, in spite of its decreasing credibility, that interpretation will continue to be popular, because it is a reality that reveals itself over the course of decades. So, that, by the time it has made itself blindingly obvious, the pool of observers who need to correct their point of view have had decades of personal error to walk back.

There is a pool of influential economists who normally add a lot of value by focusing on the supply-side. They defend the point that everybody is better off when we are capable of making stuff. But, unfortunately, there is a big overlap in the Venn Diagram of those economists and economists that were on record in 2008 cheerleading liquidation, mass unemployment, and financial duress because they were certain we had seen history’s biggest housing bubble.

It would be hard to walk that back. Individuals might, but it would be hard for entire schools of thought to do that. So, we will need a whole new pool of supply-side economists in order to reclaim an academy that can get housing right. That will take decades.

Properly Deflating Case-Shiller

One problem with Figure 1 is that Shiller deflates home prices with general inflation. His reasoning, which is about 3 decades into being forthrightly debunked, is that when rents rise, home prices rise. That should trigger new construction, which lowers rent inflation and home prices as new supply comes onto the market.

Well, it’s not so much debunked. That is the way the economy does work wherever there isn’t some constable standing athwart history in the name of state capacity to keep it from working. It’s just not the way our housing market has been working.

That is still the way Case-Shiller is deflated, even though rent has accumulated something like 40% of excess inflation. The old guard will not be transitioning from Figure 1 to Figure 2.

Figure 3 shows what the real Case-Shiller index looks like if you deflate it with rents instead of general CPI. There is still a bit of an upward drift, which I have asserted is due to the difference between price/rent on structures vs. land. Inflation caused by constrained supply is not caused by nicer buildings. It is caused by the lack of buildings. It all flows to land value. So, Case-Shiller in 2024 is still elevated, even when deflated with rent inflation, because high rents cause prices to rise even more.

Mechanically, most of the rise in prices is proportional to rising rents. I would agree that there was a decent cyclical component to the high real Case-Shiller index in 2006. Even after fully adjusting for rents, average home prices might have been as much as 20% above a cyclically neutral price. Today, I think we are near a cyclically neutral level. We’re just further along on Figure 2. Cyclically neutral is a lot higher than it was in 2006.

So, even though the Case-Shiller index, deflated with rents, is still about 40% higher than the 20th century norm, that is entirely because each 1% rise in rents is associated with more than a 1% rise in prices.

Case-Shiller and Filtering

The Case-Shiller index attempts to track the value of the average home over time, adjusted for improvements in quality, etc. beyond basic maintenance. Adjusting for inflation is just adjusting for the value of the dollar. That’s why the Case-Shiller index should be and was flat throughout the 20th century. It’s just measuring the value of a structure. The land value shouldn’t be changing much. If the index is meant to estimate the value of homes that stay the same, the index should stay the same.

But, note, that doesn’t necessarily tell us about housing affordability. Over the 20th century, population and the stock of homes quadrupled. Real per capita income septupled.

Think of the proverbial Case-Shiller benchmark house in 1900. If it was maintained to remain basically the same for a century, at the end of that century, it was a much different reference item. If it had truly remained unchanged, and, say a family with a $30,000 (2024 $) income lived in it in 1900 and a family with $30,000 income still lives in it in 2024, those are very different families.

Over the long term, the Case-Shiller index can tell us a lot about filtering.

Instead of deflating the Case-Shiller index with inflation, what if we compare the nominal Case-Shiller index with incomes?

Figure 4 shows what this looks like, since 1953. The dark red line is the ratio of the Case-Shiller index over per capita income.

It’s hard to see it the way the Case-Shiller index is normally displayed, but when the real Case-Shiller index was flat, there was some hella filtering going on.

In Figure 4, I also show the average price of new homes, per square foot, again as a ratio with per capita income in the denominator. The downward trend has generally continued in new homes, even though it has stopped in existing homes measured by Case-Shiller.

And, this is actually an understatement. The 2008 mortgage crackdown created a huge compositional shift. Since then, new homes have been constructed at about 1/2 the rate they used to be. And, it has been pretty strictly due to the collapse of low-tier new homes. The bottom half of the new home market was dropped and the top half remains. So the average new home price is higher than it would be if new homes were being built at the rate that they used to be before 2008.

The shortage of new homes has increased the prices of existing homes. And, that is because it increased the price of the land under the existing homes. Filtering stopped. Land values have been rising as fast as real incomes. In housing, we’re nearing a point where grandchildren are no better off than their grandparents were.

That infamous real Case-Shiller chart does contain some cyclical fluctuations. But what the millions of folks who have been sharing those charts on e-mail chains and social apps for 20 years didn’t know is that the real Case-Shiller index chart was showing the end of downward filtering.

It’s sort of ironic that builders will complain about costs. Many will say that they can’t build more homes because they don’t “pencil”. And if they don’t “pencil”, then surely the costs are too high. That’s not wrong, in a literal sense. But, isn’t it a bit strange that homes built with much cheaper materials and labor (because they were built 20 or 40 years ago) have gotten more expensive than new homes have?

Here is a chart of the slope of the red line in Figure 5.

Call this a poor man’s estimate of the filtering rate over time.

According to the Erdmann Housing Tracker, home prices were cyclically neutral in 2002 and also recently. There has been a lot of cyclical and credit-oriented volatility since 2002. The slope has been up and down, measuring prices, but it has averaged about 1% annually over that time. Call that the 21st century filtering rate. About the same as the late 20th century filtering rate, but now it’s the wrong sign.

In Figure 6, in data since 1965, I have adjusted for household size.

In Figure 4, the downward filtering rate in the mid-20th century was probably overstated by using per capita income, because household size was shrinking (fewer people in the average household). Figure 6 adjusts for that, but household size hasn’t really changed much since the 1990s (in part, because we don’t have houses for the extra households). So, the recent story remains basically the same.

How does the case shiller index account for true depreciation? What I mean is that when house X is 50 years old the walls and roof might be just as valuable as they were (assuming they were maintained) but some things just aren't. Electrical outlets for example. Floor plans? A layout that is great for a family with 4 kids is less than optimal for a family with 1.