Another Funny Chart

I saw this explanation of the power of large scale investors on Twitter:

Blackstone does not need to buy every house in a city to drive up prices and price out families.

How can one buyer move an entire market?

Auction theory tells us the “marginal bidder” sets the price. In housing, that bidder is the one who just barely wins—or even loses—a deal, and their price becomes the new benchmark going forward.

Who used to be the marginal bidder?

For decades, it was a young couple stretching their savings to buy their first home. Their bids set the clearing price in neighborhoods across America.

Who is the marginal bidder now?

Now it’s private equity firms like Blackstone, stepping into neighborhoods with billions in capital—much of it raised from overseas investors, including China—and boosted by artificially low tax rates through the carried interest loophole. They can bid high because of their (1) huge pool of overseas capital and (2) unfair tax advantage. If either (or both) ended, they couldn’t bid as often and as much as they do.

How does one high home price ripple into higher home prices elsewhere?

We’ve all heard real estate agents talk about “comps” (comparable sales). When a home goes on the market, agents look at recent sales in the area to set the listing price. If Blackstone pushes one house from $320,000 to $340,000, that becomes the new comp. The next seller sets at at least $340,000 even if Blackstone isn’t even bidding on that property. This price increase ripples across town and nearby ones as well. Therefore Blackstone could push prices up for 100 single-family homes in a city by literally only driving up the price on one home.

What’s the result for working families?

Prices climb, mortgage payments grow, and young couples are locked out of homeownership. Couples delay growing (or even starting a family), less labor mobility, less long-term wealth creation, more dependence on government benefits.

The bottom line: Blackstone is having a massive negative impact on the single-family home market even if they technically only purchase a low single digit percentage of homes.

Seems legit, doesn’t it? Compelling?

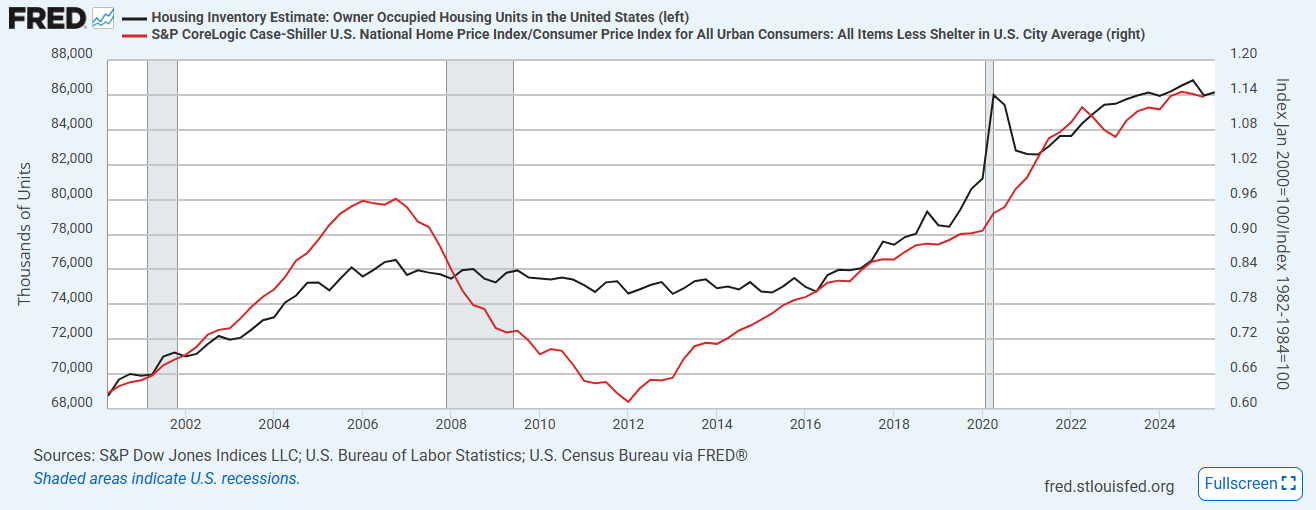

Here’s a chart comparing the number of homes that are owner-occupied since 2000 and the real Case-Shiller US home price index.

It is possible to take what seems like economic logic, empirical experience, and experimental findings and to use them to tell wholesale tall tales.

The story above, which is popular, and whose popularity might eventually be the final nail in American housing’s coffin, is really a sort of “one drop rule” story. If large investors buy even one home, it is more important than 99 homes bought by families. One drop of poison turns the whole thing to poison. One drop of the wrong blood makes you an untouchable.

Ironically, at the same time, Lance Lambert at ResiClub is reporting that in regions where sales to homeowners have slowed, homebuilders are looking to sell new homes in bulk, at a discount, to investors, to keep revenues stable.

Wait, aren’t the investors the ones pushing prices higher? Since investors set the marginal prices, wouldn’t homebuilders see a slowdown in sales to investors, so they would be hoping to sell those homes at a discount to families? Weird.

I think there is a further irony here. Many observers will interpret the turn by builders to investor buyers as a desperation move signaling the end to another bubble cycle.

But, is that what happened in 2008? Did homebuilders turn in desperation to investors to keep revenues stable?

No. There was no large-scale investor market. In 2006 and early 2007, a lot of the subprime mortgages were being used by small-scale investors, but they were mostly buying existing homes - fixer-uppers. But there weren’t well capitalized large firms regularly buying up whole new neighborhoods or managing thousands of homes as rentals.

The fact that builders are looking at this source of revenue isn’t really bearish. It might reflect some softness in sales in some regions. But, in the broader sense, it’s a reflection of how much safer the homebuilder market is today. They have an option they never had before. Because of the mortgage crackdown, rents are much higher today. There is a lot of demand from renters. And, now, there is a burgeoning market of investors and firms looking to supply the homes to meet that demand.

They actually tend to have a price point that is a bit lower than owner-occupiers, which is why Figure 1 looks like it does. Home prices have been going up because homeowners are outbidding the corporations. Of course they are. They also outbid the corporations at all times before 2008. That’s why this market didn’t exist at all before 2008. History couldn’t have constructed a brighter, louder sign notifying us that under normal circumstances, large corporations do not outbid families for single family homes.

They still don’t, but families who now can’t legally get access to mortgages need somebody to own a home for them. And, so there is a practically insatiable demand for homes at prices a bit below the prices owner-occupiers pay.

Homebuilders looking to sell homes in bulk to investors isn’t a signal that another 2008 is around the corner. It is a signal that 2008 won’t happen again.

In fact, I expect the new home market for several years to grow in quantity while prices remain stable or even slightly decline. Homebuilders will be doing fine. Margins will remain comfortable. And most of the growth in units sold will be to investors. I wonder how many years that will go on before the bears recalibrate their expectations? We are now 3 years into higher interest rates. Has anyone changed their mind yet about high interest rates crashing the homebuilder market?

In the meantime, don’t hold your breath for any articles in the New Republic noting that the new large scale investors may be helping to stabilize new housing supply and home prices.

I respect The Economist, but their recent issue had a rather uninformed piece on U.S. housing. They cited price declines in a few areas as an indication of the potential for broader softening in the market. The most laughable example they gave was some recent price drops on Martha's Vineyard and Nantucket. While it is true that these two islands have had some struggles since the collapse of the whaling industry, home prices still point to supply constraints. Feel free to browse some current real estate listings in both places for bargains. (Have some smelling salts handy....)