2024 IS the counterfactual to 2009!

I was reading the latest ResiClub post that ends: “Big picture: U.S. home prices have been in a period of sideways movement following the 2022 mortgage rate shock. However, under the surface, some markets have seen some give up while others continue to climb at an elevated pace.”

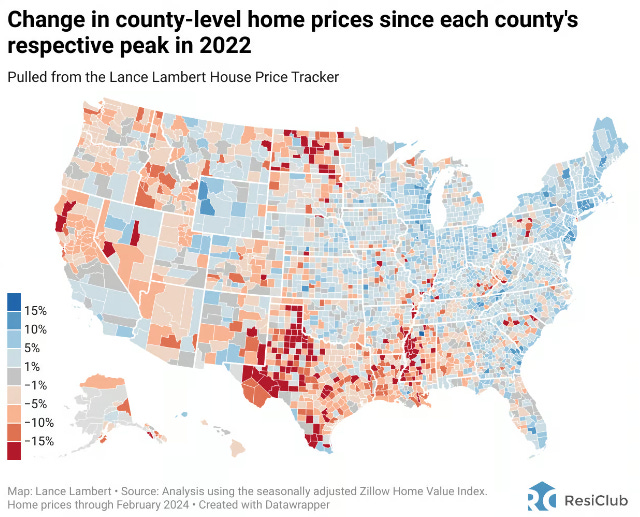

Lance shows this graphic of relative home prices since the 2022 peak. There is about a 30% range from the lowest to the highest price change. And, it hit me. This is what I’m talking about. This is what 2008 and 2009 should have looked like.

When I say that the entire $5 trillion wealth shock after 2007 was due to excessively tightened lending standards, this is the map I have in mind. I don’t mean that no city would have seen deep price cuts. That was probably inevitable in Phoenix and Orlando at some point. But prices in other places might have continued going up, netting to zero at the national level.

Just like now.

When I say that the entire $5 trillion wealth shock was due to excessively tightened lending standards, that absolutely doesn’t mean that no real estate speculator will ever take losses. Here we are in boring, flat 2024, and yet there are counties where home prices are down more than 15%. When I say that $5 trillion of losses could have been avoided, Phoenix real estate might still have taken a 15% bath (or more).

Comparing 2024 to 2009

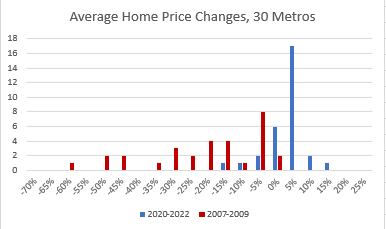

Using histograms and the 30 metropolitan areas from the Erdmann Housing Tracker, let’s compare 2024 to 2009. Specifically, I am comparing the 20 month periods of June 2022-February 2024 and December 2007-August 2009.

First, let’s look at metropolitan area averages. (These are on a natural log, or continually compounded, scale. So, think of a change of 50% as a fifty 1% changes. The changes compound on themselves. This is just how I calculate the numbers in the tracker because doing it this way means that a 50% loss followed by a 50% gain gets back to the starting point, so that changes are balanced over time.)

Figure 1 shows the mess of the Great Recession clearly. It probably sort of makes you wonder how I could say 2024 and 2009 could have been the same.

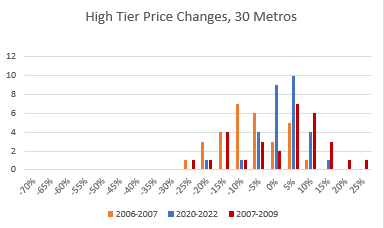

But, now, let’s look at high tier neighborhoods, in Figure 2. These are price trends in neighborhoods that, in the typical metro, would have average adjusted gross incomes today of about $200,000. The market for those neighborhoods doesn’t require generous lending standards for marginally prime borrowers. And price changes in those neighborhoods from 2007 to 2009 (red) were about the same as the changes from 2022 to 2024 (blue).

As Lance points out in the county data, the national number hides a lot of local variation, so there were cities where high tier prices declined by 25% from 2007 to 2009 and cities where high tier prices rose by 25%.

You might assume that it is obvious which cities were which. But it isn’t.

You see, as seasoned Erdmann Housing Tracker subscribers know, the tracker data clearly delineates between the two periods. There was a true cyclical boom and bust from 2002 to 2007, of about 20%. But that boom had reversed before the recession started at the end of 2007. I have added a third group of bars here - the 20 months leading up to December 2007. That is when the housing boom reversed. And since it was a true cyclical boom, it affected the high tier neighborhoods as well as the low tier neighborhoods. The high tier home price in the average city dropped by about 10% over that time, before adjusting for inflation. That period is different than 2022-2024. The high home price appreciation before 2022 was mostly related to the general rise of transitory inflation, and so it isn’t going to reverse. Before 2006, there had been a large boom specific to housing - boosted by the subprime boom - which did reverse. But that period was over by 2007.

Then, since borrowers and lenders hadn’t paid enough for their sins, and the country was in the throes of a moral panic, policymakers kept turning the screws and they cut off access to about a third of the traditional mortgage borrowers’ market over the course of 2008.

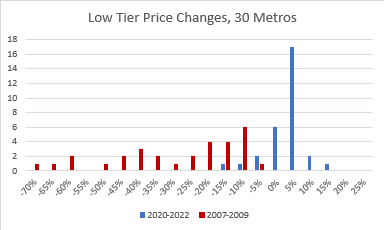

Just as Lance points out in the county data that the level national number hides a lot of local variation, metropolitan area numbers hide a lot of local variation across neighborhoods. And, since the crisis of 2008 was caused by a mortgage moral panic, those variations were highly systematic. Figure 3 shows price changes in neighborhoods that would have average adjusted gross income of about $60,000 today.

In Figure 3, 2007-2009 looks nothing like 2022-2024.

The post-2007 changes weren’t the reversal of a bubble. In fact, they were a novel new bust. It wasn’t a regional bust. It was a regressive bust on poor neighborhoods across the country. The bust was what was out of equilibrium, and it had to inevitably reverse because new homes would not be built until prices recovered. So, over the 15 years since then, rents in the poorest neighborhoods of all of those cities have risen while builders were forced to the sidelines and investors came in and bought up the deals in the existing stock of homes.

Don’t we all know novice real estate investors who started buying up cheap properties during that time? It was a feast just waiting to be lapped up because there is no way that small time investors could buy up all the discounted properties. There just isn’t enough small-scale capital. Slowly, large-scale institutional capital eventually came into the space, and now, finally, prices have risen high enough that the large-scale buyers are purchasing new homes from the builders.

So, basically, imagine all those red bars attached to a rubber band. We tossed them in Figure 3 to the left as hard as we could. Truly, the intention was to harm. Of course, in a moral panic, who deserves to be harmed and who gets harmed are all bound up in such confusion that the outcomes bear little resemblance to the projections.

By 2009, we had thrown those red bars about as far as they could go, and then they all rebounded back to the right and finally are settling back at neutral valuations that might induce new entry-level construction and moderate future price appreciation.

Figure 4 gives just a slightly different way of looking at it. Here, I have subtracted the price changes in the $200,000 income neighborhoods from the $60,000 income neighborhoods. This is the difference in price changes within each metro area between poor neighborhoods and rich neighborhoods.

In the fog of the moral panic, it was easy to look at the outcomes of Figure 1 and conclude that outcomes were based on metropolitan area differences. Some metro areas had it coming. They were bubble markets. They had attracted reckless capital that would inevitably be disciplined by failure.

But, really, what happened is that we imposed a mass tragedy on the poorest neighborhoods and working class homeowners in every city in the country. In some cities, local conditions amplified those harms more than they did in other cities. The difference in the median outcomes of each metropolitan area had little to do with differences of the cities themselves. The differences in the medians were just a partial measure of how bad the poorest neighborhoods got hit by the mortgage crackdown.

What happened was that the poorest neighborhoods across the country took it in the chin. And, to this day, the average dude or gal at the financial analyst or macroeconomics conference or political convention feels a sense of superiority about enforcing that outcome.

Leveraged malinvestment is foolish, and so the damage was just deserts. You and I, of course, know better. If only all that dumb money could have been more disciplined so we wouldn’t have had to force the discipline on them.

“You would lend those fools mortgages again?! That’s your answer to the housing problem? Look at what happened last time we did that?!” (This fails to distinguish between the subprime boom that ended by early 2007 and the post-2007 crackdown on mortgage lending due to the moral panic. Two almost completely unrelated events.)

Figures 3-7, 3-8, and 3-9 from “Shut Out” lay out the picture of what happened according to city type - Closed Access (cities like LA and NYC that were underhoused well before the Great Recession), Contagion (places like Florida and Arizona that were inundated with housing refugees before the Great Recession and then thrown into deep recessions when that migration collapsed), and, other places, which I divided at the time between “Open Access” and “Uncategorized”

Figure 3-7 shows what happened up to 2006. As I have demonstrated here at the substack, and as 15 years of hindsight makes clear, inadequate supply is regressive. When you don’t build enough homes, rents and prices of homes poor people live in go up faster than homes rich people live in. The “Closed Access” cities don’t build enough housing, and so that’s what happened - housing costs increased for poor residents the most.

It didn’t happen anywhere else. In Florida and Arizona (the “Contagion” cities), all prices went up because they were being inundated with a population surge they couldn’t keep up with. (We saw that with Austin during the Covid boom.) The only trend shown in Figure 3-7 that was probably unsustainable was the 30% or so additional rise in Contagion city prices compared to other cities. The high prices of the poor neighborhoods in the Closed Access cities were not a cyclical phenomenon.

The moral panic was set off like a bull in a china shop. The goal of the mortgage crackdown was to reverse the price trends that really only were happening in the Closed Access cities. And, to the confused panickers, the crackdown worked.

In Figure 3-8, you can see that prices in poor neighborhoods collapsed from 2006 to 2013 in every type of city. This is basically what Figure 3 and 4 show above. Unfortunately, it happened everywhere, even though the phenomenon it was reversing had only happened in the Closed Access cities.

Also, you can see that the Contagion cities had an additional loss of 30% or so that applied to the whole metropolitan area. (We have seen that sort of trend in Austin recently.) That is basically the orange bars in Figure 2 above. And, as I mentioned, the Contagion city correction happened before the recession, and the mortgage moral panic dislocation that affected poor neighborhoods in every city happened during and after the recession.

Paid subscribers to the EHT can see this in the tracker components at the time. First, the cyclical component turned down (and the supply component continued to rise after 2005 while housing starts collapsed and worsened supply conditions). Then the credit shock hit. Really, two separate busts occurring with no overlap.

The Covid boom was different, but not just because the cyclical boom was smaller. It was also different because there hasn’t been, and really can’t be, an additional credit shock.

Finally, Figure 3-9 shows the combined result of the mismatched boom and bust - the total change in prices from 1998 to 2013. The Closed Access cities had become much more expensive across the board. And in every other city, high tier homes had basically appreciated a normal amount for a 15 year span, and low tier homes were now deeply discounted.

In every single city, this was a disequilibrium. In the Closed Access cities where housing is deeply undersupplied, prices in equilibrium should rise more in the poor neighborhoods. So, low tier homes in every city, including the Closed Access cities had to rise after 2013 to get back to a neutral valuation, and it took more than a decade for enough non-owner-occupier capital to flow in to fill the gap and pull those prices back up.

Actually, now every city looks a little bit more like a Closed Access city, because building has been so stifled for 15 years, and so poor neighborhoods everywhere are now more expensive than they used to be.

Conclusion

To reiterate the earlier point, 2024 is actually what 2007-2009 could have and should have looked like. If you want to know how America could have avoided a $5 trillion highly regressive wealth shock without the moral hazard of constantly bailing out dumb money, the answers are all tragic and ironic.

It was 2008 that required bailouts. Nobody’s asking to bailout Austin real estate investors in 2024. The moral panic created the demand and need for bailouts. If the mortgage crackdown hadn’t happened, and if the Fed had aimed for a recovery in construction and home values, there would have been a real estate bust in the Contagion cities, for better or worse. Some real estate speculators there would have taken a bath, and there would never have been trillion dollar rescue packages.

If you’re pro-mortgage crackdown, then, in practice, you’re pro-bailout. Don’t pat yourself on the back for complaining helplessly about the bailouts your favored policies necessitated.

Of course, the people that were hurt the worst, not of their own actions, didn’t get bailouts. Hurting them was the point, or was the unintended result of whatever the point was supposed to be, because the collapse in the prices of their homes was the goal. You could take the Rick Santelli tea party stand and say “screw them” or you could take the Occupy Wall Street stand and say, “It’s the bankers’ fault” and take the self-satisfied incoherent position that we should somehow simultaneously enforce 50% declines in valuation by locking families out of mortgage access while also subsidizing those families for the $5 trillion loss.(1)

We don’t face the same conundrum today, because mortgage access was never reinstated for millions of American families, so there is no room for a credit shock. So, the bull-in-a-china-shop position today is to call for a ban on large-scale corporate buyers of single-family homes.

However, in today’s context, we are at a bit of a tipping point. Those buyers represent an exceedingly small portion of total ownership - less than 1% of the stock of single-family homes. But, they are the only potential marginal buyers going forward that can continue to increase housing starts until they are sustainably high enough to allow rents to finally moderate. So, banning them likely won’t lead to a price bust like we saw from 2008 to 2012. It will just keep us in the status quo, where housing production remains unsustainably low and rents grind higher every year, especially in neighborhoods with lower incomes.

I suppose the only populist position that will be left if corporate buyers are banned will be banning landlords themselves. Will we ban them? And the homeless, themselves, will probably be increasingly blamed. I hope we don’t get to that, but to be honest, the populist strength of the “ban corporations” movement seems especially hard to counter. It just seems so obvious to the naive observer that corporations are out-bidding families for homes. If these proposed bans succeed, I don’t think it will hurt homeowners that much, and it will benefit small scale landlords, investors, etc. But, I really shutter in fear of what will happen culturally. How could the misdirected anger be redirected? There will be many crackdowns - crackdowns on the homeless, on immigrants, on landlords, on short-term rentals, on gentrifiers, on and on. I can’t imagine the trigger that could stop our national self-immolation if we take the next step in housing obstruction.

(1) Why do I say, the collapse in the prices of their homes was the goal? Essentially all of the literature, both academic and popular, treats the end result - the final price levels resulting in Figure 3-9 above - as the baseline - the return to normalcy. In a previous post, I highlighted an example of this problem. This quote is from a “The New Republic” article about an urban studies professor from Georgia Tech. This is about poor neighborhoods in Atlanta that lost more than half their value after 2007.

In 2012, as the market began to recover, the same neighborhoods became “strike zones” for private equity firms. With home values badly damaged, Immergluck argues, the city could have reserved foreclosed properties for long-term affordable housing or sold them to Black households at low prices.

As I pointed out in the post, the professor takes the 2012 values as the baseline. The professor and the author of the post don’t apply a single neuron to the question, “Should home values have dropped 60%?” They incorrectly treat it as an inevitable result of the subprime boom and bust. Even today, they are fully committed to that outcome. The new bottom is the baseline for them to imagine the social justice response for that neighborhood. Of course, there is no coherent social justice position that one can take, if it starts with the presumption that property values in a neighborhood should be less than half of any previous precedent. For values to be that low, and for these misguided blokes to benchmark to them, those neighborhoods had to be strangled and suffocated. Stopping the private equity investors that made those neighborhoods “strike zones” is a particularly self-righteous and popular form of suffocation.

The only socially just question to ask about those neighborhoods is “What did we do to them to suck more than half the value from their homes?”

To answer that question requires accepting two observations. (1) Residents of those neighborhoods had agency and were capable of competently arranging their financial lives. And (2) Part of that competency involves symbiotic relationships with the financial sector to fund capital, such as housing. Many people can never accept both of those observations, and in 2009 or 2012, effectively, nobody could. So literally nobody could even ask the only socially just question that those residents needed them to ask.

Why are the houses so cheap? Because we drove the bankers away.

Even today, looking back critically, they look back to 2012 for solutions. It’s like imagining what you would do if a genie granted you one wish to help Nagasaki, and you asked for a Time Machine to 1946.

How can we get the houses so cheap again? Drive out private equity.

At some point the inability or unwillingness to address a problem - especially when the unwillingness is universal and systemic - becomes complicity in the outcome. Munchausens by Proxy, for neighborhoods.

Thanks Kevin. I’ll be away for a few days. We can continue when I’m back. Ken

This is a little off topic, maybe, but your statement that "It was a feast just waiting to be lapped up because there is no way that small time investors could buy up all the discounted properties. There just isn’t enough small-scale capital. Slowly, large-scale institutional capital eventually came into the space, and now, finally, prices have risen high enough that the large-scale buyers are purchasing new homes from the builders." reminded me of something I've always wanted to look at.

I was looking at a graph of housing starts going back to the mid 60's broken out into single-family and multifamily. The compressed graph emphasized how flat the MF start line became beginning in the late 80's which coincides with changes to the tax laws. Those changes impacted depreciation schedules and limited passive losses.

Before those changes most of the small apartment buildings and 4-duplexes, the missing middle, were mainly built as tax shelters and owned by small partnerships, mostly local. I remember reading that MF starts fell over 50% in years shortly after those changes.

My hunch is just like your statement about larger scale capital in the SF space, the same occurred in the MF space as a result. My hunch is also that it's not just zoning that limits the missing middle; it's lack of capital. Also, because of scale it's hard for a new 4-plex to compete with a new 200 unit apartment complex with full amenities.

It's a different world today.