Upside Down Capital Asset Pricing Model, Part 1

In this post, I will lay out some background for my mental model of how interest rates relate to returns on assets outside the fixed-income class. I find the hyperfocus on interest rates as a causal factor changing prices across assets to be misplaced, especially when it is treated as a tool that the Federal Reserve can turn up or down like a switch.

This goes back to an intuition I have used for years to think about the Capital Asset Pricing Model (CAPM). The basic CAPM equation is:

ERi = Rf + βi (ERm−Rf) where:

ERi=expected return of investment

Rf=risk-free rate

βi=beta of the investment

(ERm−Rf)=market risk premium

The way this is used with equities is that the risk free rate is the Treasury rate. Long term bond rates are the correct rates to use to consider returns on stocks. The equity risk premium is the additional returns that investors expect above the returns on Treasury bonds. The beta of a broad index of equities is 1.

Let’s say Treasuries pay 5%, and the S&P 500 appears to be priced to earn 8%. Then, the risk premium is 3%.

Let’s say there are 2 stocks. One is the equity of a leveraged firm in a cyclical industry that will fall twice as much as the average stock in a recession and recover twice as fast. The other is a non-cyclical stock with no leverage that fluctuates half as much as the average stock. The first stock has a beta of 2 and the second stock has a beta of 0.5. Since there is extra cyclical risk with the first stock it will require an 11% return to justify holding it (5% + 3% x 2). The other stock will only require 6.5% (5% + 3% x .5). (I’m ignoring messy technical details with compounding, exponential growth, etc.)

When interest rates change, in practice those changes are treated as “all else equal” changes. So, if interest rates rise by 1%, then pundits usually act as if stock prices will fall. The yield on stocks is earnings/price, and if earnings are a part of “all else equal”, then price has to fall for the yield on stocks to go up.

I think it makes more sense to start from the top down.

ERi - βi (ERm−Rf) = Rf

The risk free interest rate is determined by the risk premium. The risk premium is determined by growth expectations, risk aversion, etc. When investors require more of a premium to take risk, that means they have to take more of a discount to avoid risk. The risk free rate is a discounted return from expected diversified at-risk returns.

I think it also, then, makes sense to think of at-risk investors to be suppliers of capital for growth, innovation, etc. and risk free savers to be deferred consumers. Assets naturally earn a rate of return (ERi), and risk free savers earn less than that because they pay a premium to avoid the risks of innovation, uncertainty, etc., to assure themselves of future income.

The risk free rate is an effect, not a cause.

And, furthermore, the expected return on a diversified basket of at-risk assets (approximated by the traded equity of public corporations) is roughly fixed over time.

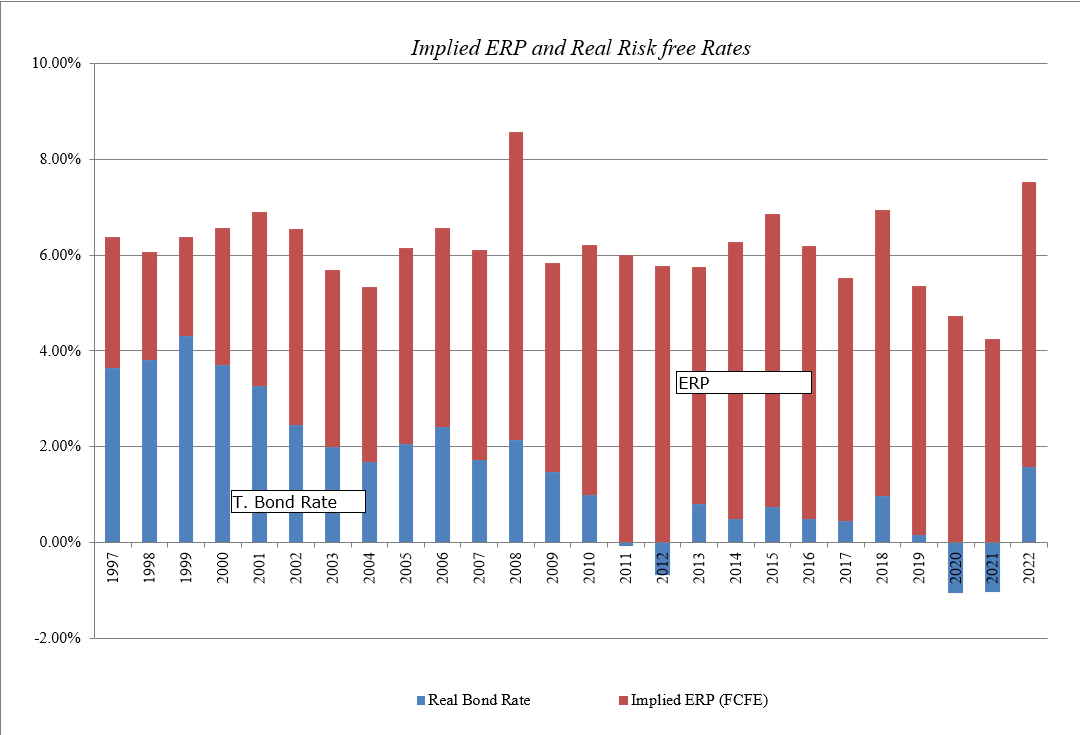

This is a hard claim to make because we can only guess at what the expected return (ERi) is. NYU finance professor Aswath Damodaran has been trying to quantify the equity risk premium (ERP) for years, and has created a long-term database about how it behaves. Figure 1 shows the long term behavior of expected returns (which is the sum of the risk free rate and the ERP).

It basically follows a flat line over time, with a bump during and after the inflationary 1970s. These are nominal returns using the nominal Treasury bond rate. Before the late 1990s, that’s all we had. But, now, we have TIPS bonds, which allow us to infer what part of interest rates are real and which parts are just the extra return required to make up for inflation.

We don’t necessarily need TIPS rates to consider whether the expected return on equities is stable. Inflation expectations have been stable for over 20 years now (excepting the brief Covid spike), and so, even in Figure 1, you can see that total returns on equities have been settled at roughly 8%, give or take a bit, through the gung-ho 90s, the internet boom and bust, the Great Recession, and its long slow recovery.

But, as I said, this is a guess. The expected return on a diversified basket of equities is a cumulative expectation for all corporations:

Expected Return = (Earnings / Price) + expected earnings growth

We can only guess at what the aggregate expected growth rate is. Damodaran goes to a lot of effort to estimate it.

Figure 2 is a reproduction of Damodaran’s chart, but using real bond yields instead of nominal yields. Total expected returns on equities are the real Treasury bond yield plus the equity risk premium. To a first approximation, that is about 6%, before inflation.

There has been a fluctuation during Covid, which I suspect is mostly related to untracked changes in growth expectations. (Or, it could be that equities were unusually overpriced in 2021 and are unusually underpriced now.) I expect that going forward, total real expected returns will track 6%.

I think this is heterodox thinking. But, it’s not really out of left field. Or, at least it shouldn’t be. For instance, Fed researchers found that hurdle rates on corporate investments tend to be much higher and more stable than risk free interest rates. As they report, the evidence on interest rate sensitivity of corporate investments is mixed.

When real interest rates rise, instead of expecting this change, in isolation, to lower stock prices, you should see it as a decline in risk aversion, a decline in the demand for deferred consumption, and probably an increase in at-risk investment.

Before modern central banks stabilized expected inflation, most of the changes in risk free rates were related to changes in expected inflation. As in Figure 1, that wasn’t associated with lower equity premiums. It was associated with higher nominal expected returns, which were all inflationary. When rates are changing because of inflation, they don’t reflect changing risk aversion, so they weren’t associated with a changing risk premium.

Since central banks have stabilized expected inflation, it has clarified this relationship. When real interest rates rise, equity risk premiums decline. Total expected returns remain basically the same: 6% plus inflation.

Higher real long term interest rates are associated with higher growth expectations. That observation fits well with this model. It doesn’t fit well with the conventional approach of treating interest rates as a tool of stimulus or austerity.

It’s really unfortunate, because the long-term decline in real rates has been mostly associated with lower growth expectations and more demand for deferred consumption. Since low rates have not been associated with higher growth, there are so many unfortunate souls who are trying to save for their retirements, and they suffer under the misapprehension that the economy is built on stilts - that we lack robust growth even after decades of Fed stimulus. They are constantly in fear that it’s all going to crumble and their savings will be lost. It’s a shame that the conventional models have created so much distress for so many lay investors.

As a first principle, I think one way to think about capital markets is that all capital markets are some combination of these two forms of ownership:

At risk ownership, which, in aggregate, earns a stable expected return of 6% plus inflation, but is highly variable from year to year because of unanticipated real shocks.

Deferred consumption, which earns a return that fluctuates over time depending on the equity risk premium. But, once a security is created, the return on that security is guaranteed.

These are two ends of a pole. Capital must choose one or the other, or some engineered combination of the two, and so their prices are inversely related. It either earns a fixed expected return that is imperfectly realized, or a fluctuating expected return that is perfectly realized.

These are substitutes. There are no other options. Only combinations of these two poles. And so their relative returns are inversely related as demand shifts between the two.

The reason they are inversely related is because growth expectations (Damodaran’s estimates are shown in Figure 4) are positively correlated with real interest rates. Conceptually, It think that’s a two-way street. Less risk-averse savers accept a lower equity premium and their investments create more growth. Growth expectations lead to more at-risk investments.

When more savers are risk averse and simply interested in preserving assets, equity risk premiums tend to be higher. So rates tend to be lower and growth tends to be lower. When savers are seeking to take risks, to innovate, to own the future rather than simply hold on to past gains, risk premiums are lower, and that is associated with higher growth and higher interest rates.

More on that in future posts.