Rough Estimate of the Cost of the Housing Shortage

The mortgage crackdown in 2008 was the most damaging political development against American housing abundance and real income growth. That all happened at the federal level. It would and could all be reversed at the federal level. The easiest way to get most of the way there without bringing up a bunch of issues that create public opposition would be to simply return the FHA, Fannie and Freddie back to pre-2008 lending standards. I think it would be difficult and counterproductive to try to reverse engineer all the problems with the current system. Just go back.

And, a similar change should be applied to banks that hold mortgages on their own balance sheets and internalize the risk of underwriting. Make sure they are appropriately capitalized and then let them take the risks.

And, when we’ve gone about that business for a while and everything’s fine, and we’ve had time to unbunch our collective panties and clean up the mess we made in them, maybe there would be ways to safely reintroduce private securitization markets, if anyone wants to try it. Or not.

Unfortunately, this most important aspect of our housing crisis shan’t be spoken aloud, so there is no need to worry that it might be fixed anytime soon.

Below is a broad estimate of what it costs us.

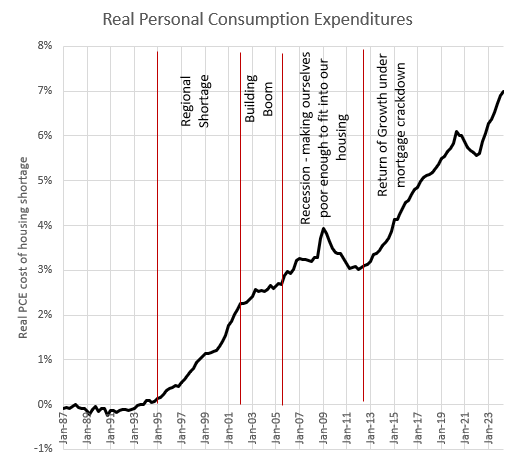

In Figure 1, the black line is real personal consumption per capita. The red line is what personal consumption would be without the excess rent inflation.

Now, this is a bit tricky, because the lack of housing doesn’t necessarily lower real incomes. If we don’t build a house, we’re going to do something else with the capital. And it’s hard to know if that something else would have been a better or worse investment for future consumption growth. Maybe instead of houses we’re getting taco trucks.

If a landlord raises rent, the tenant’s real income declines, but the landlord’s nominal and real income increases by the same amount. So, the way the government accounts for the increased rent is that nominal growth is higher but real growth is the same. That’s in the aggregate. Of course, that is the average of the landlord’s real gain and the tenant’s real loss. The difference in growth comes from the difference between what the landlord does with that cash versus what the tenant would have done with it.

One way to think about it is that the black line is our average real consumption, the gray line is the tenant’s real consumption, and the red line is the landlord’s real consumption. Homeowners, being both, are on the black line.

Before 2008, maybe you could argue that, if we didn’t have binding local land use regulations, that we would have followed the red line. The houses were still produced. They just were produced in places that required economic displacement from places where they weren’t built. So, there wasn’t any capital left to invest in non-housing consumption. It’s just that (1) there was a tenant-to-landlord transfer in the cities were homes weren’t being adequately built and (2) the homes that were built weren’t as productive and were associated with idiosyncratic personal harms related to displacement.

From 2006 to 2012, the loss in real incomes was related to the moral panic and the crisis. Incomes declined. Investment declined. Millions were stuck in long-term unemployment. Certainly the counterfactual without the moral panic and with more mortgage access would have been associated with higher real consumption, though the pieces of that story are complicated.

During the 2002-2005 building boom, rent inflation was slowing down because the building was ameliorating rising rents. Then, from 2006 to 2012, rent inflation was moderate because we made ourselves poor. You can see that more clearly in Figure 2, which shows the difference between the red line and the black line.

Eventually, the broad vow of stagnation couldn’t continue and income growth returned. By this time, the mortgage crackdown meant that the shortage wasn’t just regional. Houses weren’t just being built in different places. Now, millions really weren’t built at all. So, since 2012, it is hard to know how the shift out of residential investment into other forms of spending changed the trajectory of growth. Maybe real growth would have followed the black line after 2012, and it’s all just a distributional issue.

The economy moves on. Workers get less. Owners get more. The lower your income, the more your rent has likely risen and the larger percentage of your nominal expenses it takes. That multiplies the distributional effects, and so which gray line you happen to fall on in Figure 1 is negatively correlated with income. The poorer you are, the lower your growth has been.

I think the coming explosion of build-to-rent housing will stop the divergence from increasing, but it will take mortgage deregulation to reverse it and pull those lines back together.

Those decades of excess rents are capitalized into the value of residential real estate. Total residential real estate is now worth nearly $60 trillion. It is undervalued because of mortgage suppression. It would be worth more than $70 trillion if traditionally served families could get mortgages to buy homes. Actually, no. If those mortgages had been available, then millions of homes would have been built. The excess rent inflation since 2008 wouldn’t have accumulated, and the homes would be worth less than $60 trillion. And everyone would be running along the black line instead of sorting into the red and gray.

There is deep and firmly-held bipartisan support for mortgage suppression. It would hurt your reputation to mention it. So, there isn’t going to be a convergence of those lines anytime soon. They might at least run parallel until build-to-rent is banned. When the calls to ban it gain a plurality of support, who is going to be so vulgar as to defend corporate landlords? Ick. So, I am tentatively preparing for deep and firmly-held bipartisan support for our final housing indignity. After that, on the policy side, all that will be left is debating the mass deportations and the homeless sweeps that will be necessary to keep the peace.

I suppose we will need to commit more thoroughly at that point to the goal of keeping ourselves poor enough to fit in our housing. Deportations will serve that goal. And, the lower interest rates that come along with that will help to revive the counter-thesis that high housing costs have just been Fed stimulus all along.

I thought you might enjoy this meme:

https://substack.com/redirect/51f2ae2b-efbb-4fc3-a86e-8bc5059ab07c?j=eyJ1IjoiazMwdWgifQ.e0r5M9XGlZdo2mKVNCjm4sCpQvY3r8dGd_Sqi471q7E

>The mortgage crackdown in 2008

This needs to be a link! What is the mortgage crackdown, how did it happen, what were the effects, etc.