The flow of funds data for the first quarter of 2023 was released today, and I thought it might be a good time for a quick review.

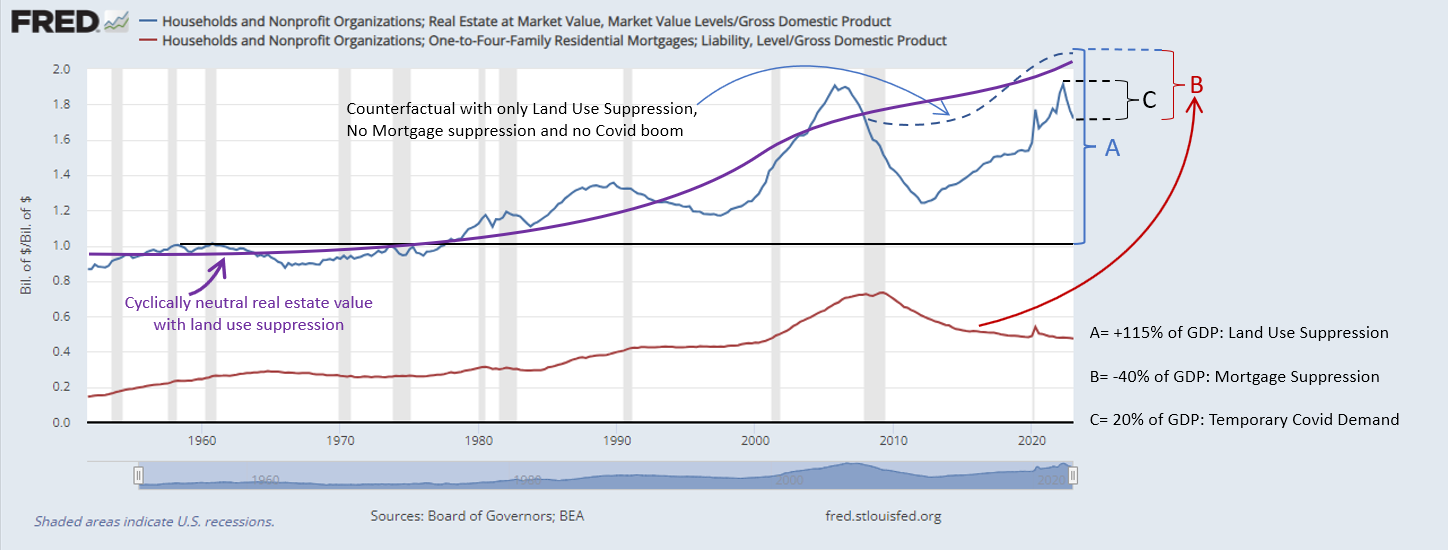

Figure 1 shows total owner-occupied real estate value as a percentage of GDP (blue) and mortgages outstanding on those homes as a percentage of GDP (red).

As I denote on the figure, I would attribute about 115 percentage points of the increase since the 1970s to supply constraints. Then, after 2007, extreme mortgage overregulation was associated with a lower total value of real estate of about 40% of GDP. And, then, at this point it seems quite clear on the chart that the burst of Covid demand against the Covid supply constraints created a unique temporary bump in real estate values equal to about 20% of GDP, which has now generally unwound, pulling sharply back to the pre-Covid trend, which will likely hold until there is a major building boom.

Some basic points, working backward.

The overestimation of (1) the influence of mortgage rates on home prices, (2) the Fed’s influence on long-term real rates, and (3) the importance of low rates on the 50 year rise in home values, leads to much more criticism toward the Fed (regarding housing), and over that temporary Covid bump, than is called for. It is the smallest of the three major factors in that chart. And, I don’t think it had much more to do with monetary policy than, say, the used car price spike did. I mean, surely, we could have prevented it, if we took strong enough measures, but there would be little justification for the likely damage of measures strong enough to have avoided it.

All those overestimations lead some analysts to assume that a downtrend in home prices will be more persistent and deep than will be the case. Really, that little bump, and its odd appearance in nearly a century of data trends, is easily identifiable as a Capacity Condition, in my three categories of market conditions.

Trends in mortgages outstanding also fail to support such focus on rates. It would be difficult to pick out periods of high or low interest rates by looking at the trends in mortgages outstanding. Rates did decline in the early 2000s as both equity and mortgages outstanding increased. However, mortgages outstanding continued to decline when rates were low in the 2010s, even though home prices were rising strongly again. And, even with that brief spike in borrowing at the start of Covid, mortgages outstanding wasn’t any higher as a percent of GDP when rates started to rise in 2022 than it had been before Covid. If the Fed stimulates home buying through the cost of debt, it sure has a funny way of showing it. But, being in love with a causal interest rate story means never having to say your sorry that there is little trace of such a thing in the data.

On the other hand, it is quite easy to see where there was a 40 point increase in the median credit score on new mortgages, when mortgage access tightened up. The scale of the effect on mortgages outstanding from that change in access simply dwarfs any verifiable effect of rates.

Using a different model, the Erdmann Housing Tracker estimates a 20% drop in real estate values (which at today’s values amounts to 40% of GDP), and that concurs with the lazy layman’s chart reading that Figure 1 suggests.

One way to think about it is that for someone blocked from borrowing, the mortgage rate is effectively infinite. The scale of that should dwarf the effect of rates. Eventually, prices had to find a floor in the investor market, and, in the aggregate, it appears that floor is about 20% below the equilibrium price of a funded owner-occupier, at the given scale of credit suppression.

The dashed blue line shows what real estate values might have done with the supply conditions we have suffered, but without the mortgage suppression or the Covid bump. This is a bit of a weak claim, because supply would have been stronger without the suppressed mortgage market, so real estate values may have levelled off in its absence. There isn’t a realistic “all else equal” scenario there. But, I think it is still a useful visual.

So, in summary:

Fed stimulus and low interest rates are overrated.

Worries about mortgage effects on prices may even have the sign wrong.

The decades-long supply obstruction is the whale of a problem compared to those other factors. The negative cycle we created after 2007 makes the last few decades look much more cyclically driven than they were. It’s just been a long, hard slog of supply constraints, with a one-time, non-repeatable credit shock.

Finally, just to take one more swipe at interest rates, here’s a figure I shared on Twitter. It appears that home prices will be flattening out here. I have marked on this chart the Zillow US home value index at the last point before interest rates started to rise sharply.

Home prices will never be lower than they were when mortgages were 3%, unless there is some terrible real economic shock around the corner. (And, if there is, mortgage rates will likely be low again when it happens.)

I may have written this in another post, but if you live in a society of astrologers, you can give yourself a big head start by simply ignoring the position of Mercury in the sky. I think mortgage rates and home prices might be analogous. Though certainly changing rates can effect gross trading and refinancing activity.

PS: Just because you were dying to see Figure 1 be even more busy, I have added a cyclically neutral real estate value trend line, to help visualize how uncyclical housing has been when you just erase the one-time credit shock from the long-term trends.

For subscribers, the Erdmann Housing Tracker basically already does this. The movement of the Cyclical component hasn’t been any less tethered to the neutral trend than my eyeball estimates here. The Tracker is a more rigorous version of this loose estimate. The big take-away here is that recognizing the effects of the mortage shock (which should be obvious, in both time and scale in the flow of funds data) can fundamentally transform your estimate of the trends and risks of the real estate market right now.

x2 on what Ben Cole said. And the period of time from the 1970's to the early 2000's demonstrates how the comprehensive worsening of zoning regulations contributed to the problems we're dealing with now. Figure 1 shows what a slow and steady grind that was, which I think many analysts missed in the price run-ups of the 90's and early aughts.

One hope I have for the years ahead is that more newly constructed multifamily units will ease rent burdens for the huge tranche of Americans who don't have pristine credit. With enough rental supply we could even see improved filtering in the single family market for some metro areas.

Excellent.

Yes there are three things that count in US real estate: Supply, supply and supply.