Notes on Inflation and Rent

Inflation is in an interesting spot. It’s run a little hot for the past few months. This has led to concerns that the excessive inflation of 2021 and 2022 is around the corner. That’s highly unlikely for a number of reasons. First, the final surge of inflation in early 2022 was the result of a supply shock related to Covid and Ukraine. (Remember the “2 quarters in a row of negative real growth is a recession” debate?) Nominal GDP growth had been high in 2021, but it fell sharply in early 2022. The last spike in prices was clearly transitory and a supply shock, which I have discussed here before.

It’s disappointing that macroeconomics is such an undeveloped field that the median macroeconomist appears to be taking the “rate hikes fixed inflation” position, which, again, as I have discussed frequently, is absurd.

In fact, the idea that the target interest rate of 1.75% (which was below negative 10% in real terms using non-shelter inflation) cured inflation but excess inflation could return while we have a 5.5% target interest rate (which is positive 3% in real terms) is a pretty damning indictment of the whole concept of inflation targeting through interest rate control. I’m not saying that the Fed doesn’t have some control over nominal spending. Just that short term changes in its target interest rate are a terrible way to think about it.

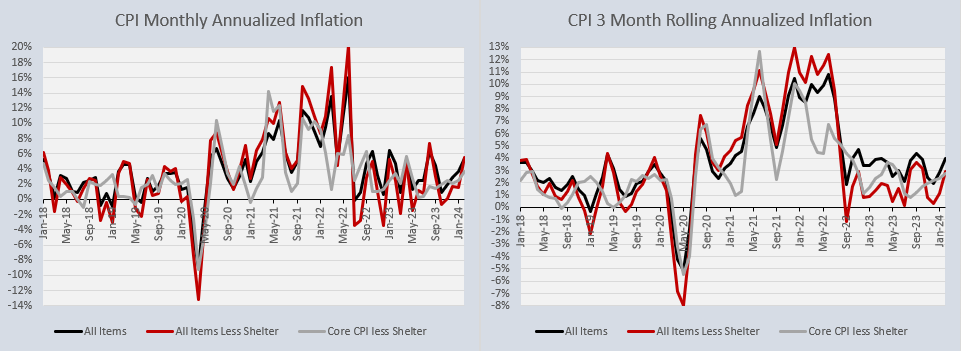

I’m pretty confident what we are seeing now is de facto 2% inflation with noise on both sides. The 3-month rolling inflation rate excluding shelter is nearing 3%, but we are still within the well-established 20-month horizontal range, as you can see in Figure 1.

Figure 2 shows cumulative inflation measures, relative to a 2% trend. Here, again, it is easy to see that shelter is persistently above general inflation, it drags up the CPI measure for all items. And, the two measures that don’t include shelter (core CPI without shelter and all items without shelter) have been flat for 20 months.

I have a post planned in which I will discuss some more and deepen and extend my framework about why shelter should not be included in inflation measures that inform monetary policy.

One thing you will notice in the measures that exclude shelter is that they had a negative trend from 2012 to 2020, while the measure that includes shelter was flat. Excess rent inflation from our housing crisis has been causing the Fed to undershoot its targets. And, one of the wins for J-Pow! has been that he has changed those trends, so far. Since the end of the transitory inflation period, non-shelter inflation has been flat along the 2% trend and CPI inflation that includes shelter has been above trend.

That is actually on target.

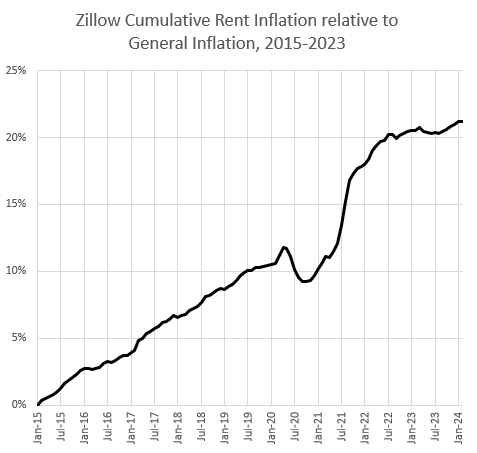

Figure 4 updates my estimates of rent and non-shelter inflation. Comparing the Zillow measure with the CPI Shelter measure, you can see that in normal times, they run together. (The Zillow measure runs about 0.8% higher than true, all-things-equal, rent inflation.) Then when prices became volatile, you can see that the CPI shelter inflation component is just mechanically muted and lagged. Eventually, the cumulative rent inflation will add up to the same total, and they will return to a flat trend with Zillow running about 0.8% higher. Until then, the CPI shelter component is just useless and only adds confusion for inflation hawks that don’t account for all of this.

J-Pow! does understand it, and sometimes talks about it, but I don’t think he drives the point home enough. It’s sort of ridiculous that there is still so much discussion about how the Fed “still has work to do”, which J-Pow! indulges, when we are 20 months into a 2% inflation trend, when you measure rents properly.

We are at an interesting crossroads here. You can see in Figure 3 that there was a clear, flat pattern before 2020 of excess rent inflation and a dearth of non-rent inflation. They averaged out to 2%, so that is where the Fed kept them.

Now, we have turned to flat trends, but now, J-Pow! has managed to put non-shelter CPI at 2% and rents are slightly higher. But rent inflation isn’t as high as they were before 2020. And, you can see in Figure 4 that for almost 2 years there has not been much cumulative rise in rents! This is very good! This is a result of housing construction continuing to be strong through the Covid shock!

And, the Residential Construction report looked very good this month! Construction lead times are shortening. Completions are finally rising above the Covid era capacity constraints. Zillow rents are settling in at a pace that would be associated with CPI shelter inflation of about 2.7. It’s not yet nothing, but it’s about a half a point better than the pre-2020 period. If residential construction can grow from here, maybe it can get lower than that.

And, because of the natural tendency for the Fed to compensate for rent inflation, this will give them more room to actually maintain a healthy nominal growth rate.

If we can get to a run-rate where both shelter and non-shelter inflation are at 2%, then it will be a tailwind we haven’t seen in decades. And if rent inflation can fall below 2% (which will take a lot more construction), then look out world, America just hit the turbo button.

I have a long annoying comment that's related only casually to this post; in fact it's in response to a recent Slow Boring post where Yglesias discusses short term rentals in the context of the U.S. housing market. He has a fascinating diagram that he uses to frame supply and demand for housing. It has four combinations:

-More Supply + More Demand=Boomtown; Florida, 19th century cities, Austin, etc...

-More Demand + Constrained Supply=Displacement; Kevin's life's work, the general hellscape of American housing, etc....

-Less Demand + Constrained Supply=Doom Loop; much or rural America, most cities in the 1960s, Detroit, etc...

-More Supply + Less Demand=???

That last scenario is fascinating to me, because although it describes some of the speculative real estate development in China I can't think of potential example here in the U.S. when it comes to housing. Some commercial office and retail architecture is experiencing this condition, but there's a potential for self correction through conversions, fire sales, and general population growth. I need to be careful with trying to provide a definitive answer because I'll end up repeating some version of Say's Law.

Given the general scarcity of all building types because of the persistence of scaled construction, the only way you could have a broad condition of More Supply + Less Demand is a Thanos type snap or Zombie apocalypse. There would be an inflationary surge from a monetary perspective, but a kind of "super-filtering" for all building types. It's amusing as a thought experiment, but such a rare (hopefully) scenario that it's not relevant to policy making. Just struck me, is that it does describe some darker periods of the Great Recession, though....

I don't know where you live, but my rent has risen by 42% in the last 3 years.