May 2024 Erdmann Housing Tracker (with Inflation Update)

This month the long boring housing expansion continues, and the GDP and inflation trends continue to be pretty boring too.

Zillow continues to show moderately rising price and rent trends.

On the inflation front, I guess, 23 months in to a stable 2% trend in non-shelter inflation, we’re still going to keep pretending that the Fed “has more work to do”. This month the short term noise was downward, so that seems to have taken the pressure off and increased the expectation of lower Fed target interest rates going forward.

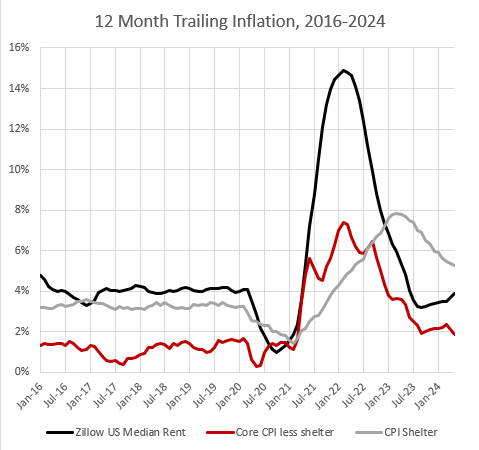

In Figure 1, I compare the Zillow US rent estimate, the CPI shelter component, and the core CPI price index (excluding the shelter component). (The Zillow rent estimate tends to run about 0.8% higher than the CPI shelter index.) You can see how when inflation surged, methodology in the CPI shelter component make it mechanically lag actual market rent changes.

I suppose you can see how the general notion of a hot inflation trend remains. I would always exclude shelter from the CPI. Not just because of the current issue with lags, but also because rising rents are mostly just a transfer of rents on land and, and they are mostly imputed rental value on owned homes, so they don’t really affect monetary flows in the short term.

Before 2020, non-shelter core CPI regularly ran below 2% and CPI shelter ran a bit over 3%. They averaged out to 2%. I think that was below a true 2% target for actual cash expenditures. The price index the Fed actually targets (PCE) has a smaller housing component. It tended to run below 2% before 2020, and as the final lags get worked out of the rent measure, it does appear that it will sidle up closer to the 2% target.

For now, CPI excluding shelter has been running very near the 2% target on a monthly basis since July 2022. Using Zillow’s estimate as a proxy, shelter inflation had recently been a bit below the pre-Covid trend.

Figure 2 shows the cumulative excess rent inflation since January 2015. After a few wiggles during the Covid period, it has glided right up to the pre-Covid cumulative trend - rent inflation about 2% higher than non-shelter inflation annually.

In Figure 3, I compare the Zillow US rent estimate (ZORI) with Core CPI excluding shelter (with 3% added annually to account for the 0.8% compositional drift in the Zillow measure and the ~2% annual excess shelter inflation). And, I have included the CPI shelter measure. The CPI shelter measure appears to have about 3% of catch-up inflation left in order to finally capture all the lagged rent inflation.

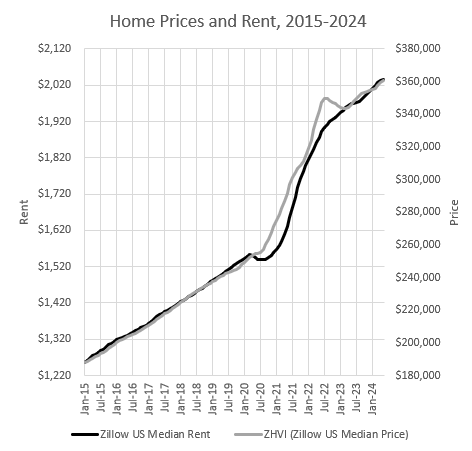

In Figure 4, I compare the Zillow US rent estimate (ZORI) and the Zillow US home price estimate (ZHVI). Again, matching them with pre-Covid trends, as I say each month, rent inflation is completely explained by regular inflation plus the persistent excess rent inflation. And, home prices are completely explained by rent inflation. Prices and rents continue to moderately rise together this month along the same parallel path they followed from 2015 to 2019.

This is all very simple. You don’t need interest rates or anything else here to explain the current level of home prices.

The rest is below the paywall.