July 2022 Tracker Update

Well, this is a very interesting month. At first glance, it looks like we have definitely entered into the first phase of a correction period - benign reversal of cyclical inflation. But, upon further reflection, maybe not.

In fact, what this month might be evidence of is the effect of changing interest rates. I am sure I will write about this more in future posts. I am skeptical of interest rate focused analysis. The reality is, housing markets have big, obvious trends, and they just don’t line up well with interest rates. I am sure there are many ways that interest rates indirectly affect home prices. And, to the extent that there is a measurable shift in interest rates above and below a neutral level, reflecting Federal Reserve policy, it is certainly associated with a rise and fall in new home sales and construction activity. But, the idea that mortgage rates are pushed to and fro by Fed policy decisions, and those rates directly push home prices up and down, is highly overestimated (imho).

However…..this month might present an interesting example. It may be an example of a context where the effect of interest rates and be isolated, and that the effect of interest rates is only related to broader housing trends in a tertiary way. In other words, I would caution against using the conventional approach to the housing cycle: “The Fed pushed up mortgage rates, which is killing the latest housing bubble, and now prices will drop because credit constrained buyers can’t afford the houses they were buying before at lower rates.” I still think that is mostly a tempting but incorrect way to prepare for changes in the housing market. If this month has anything to say about it, it is saying, “The previous trends are, more or less, still in place, and, by the way, a sharp spike in mortgage rates may have created an unrelated shift down in some prices.”

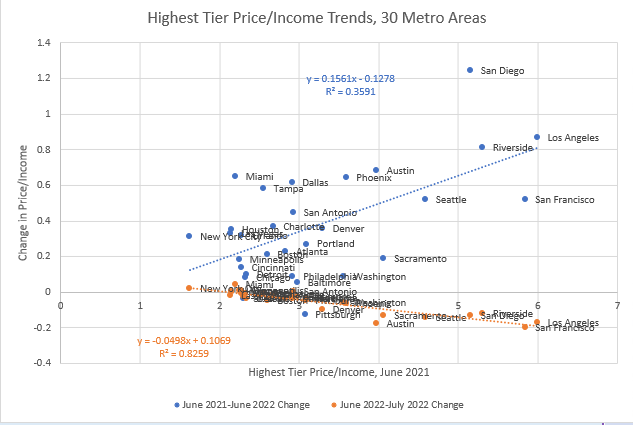

Here is a chart that gets at this. Places where homes are expensive in the richest neighborhoods had been getting more expensive in the post-Covid period, but suddenly that is reversing. And, the reversal is highly correlated with price/income levels.

This is different from my measures of cyclical or supply-driven price deviations. The expensive cities aren’t necessarily cities that have had recent cyclical booms. These are the price/income levels of very high-end homes that aren’t driven by either credit constraints or supply constraints. Much of the difference here between metro areas is from things like local costs and taxes (property taxes lower these prices and developmental taxes raise them, generally, for example).

I push back a lot against focusing on interest rates, but interest rates could plausibly explain these patterns (rising prices in expensive places when rates were low that are now reversing after rates increased). But, that explanation has little to do with credit constrained buyers maxing out their approved mortgage payments. If interest rates explain this, it is purely a textbook financial present value calculation. Higher rates have lowered the present value of future rents, and that effect is stronger where things like low property taxes make prices more volatile.

So, there has been some reversal in cyclical price deviations in this month’s data. That reversal is correlated with pre-existing expense, as shown in Figure 1. In other words, in expensive cities, like San Francisco, prices in July reversed. But, the recent price boom hasn’t been in the expensive cities. It has been driven by migration out into the least expensive cities. So, this isn’t a reversal of recent cyclical trends.

In fact, you might say that low interest rates were mitigating against recent cyclical trends! There has been a lot of upward pressure on home prices in more affordable cities because of population flows, and maybe at the same time interest rates were pushing the see-saw in the other direction, boosting prices and demand in the expensive cities that have been losing population.

So, again, I think it may not be helpful to view the housing cycle through an interest rate lens. I just don’t think it gets at the fundamental drivers of the cycle, and to the extent that it does, it is complicated.

There is much more to say about trends this month, and that will be below the fold for paid subscribers. If you have any interest in understanding the current housing market, this is a good month to jump in. And, please, share this if you know anyone who makes asset allocation decisions or would be interested in a an analysis of the housing cycle. I am certain that this analysis will be useful and unique for them.