December 2023 CPI and the Soft Landing

JPow! continues to win.

We are now 18 months into very boring and normal inflation trends. I don’t understand why so many observers who should know better - who are on the record as knowing better - are still acting like returning to 2% inflation is still a work in progress. It’s amazing that we ever get decent monetary policy with such deep-seated backward looking biases. It’s especially amazing how well JPow! has done, given the state of monetary discourse.

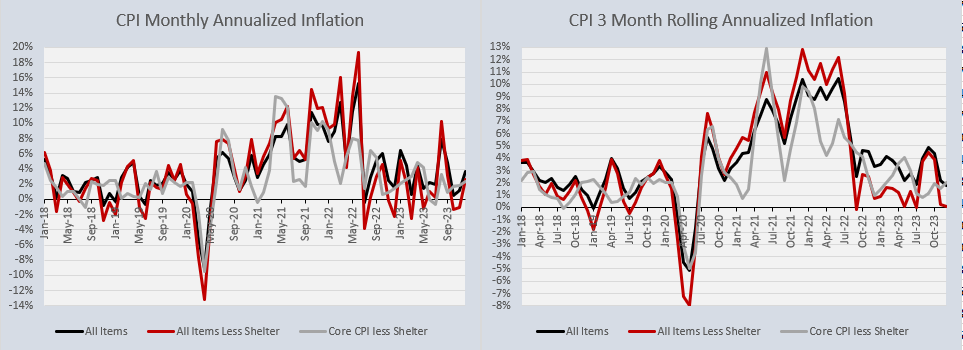

You really don’t even need to correct for the lag in CPI shelter to see the shift to normalcy 18 months ago in Figure 1. But, the elevated shelter component is, I guess, what makes it acceptable to still pretend inflation is marginally above 2%.

Figure 2 shows that Zillow rent estimates have basically followed the general trends in rent (with a bit of a dive in 2020 followed by a bump in 2021). Shelter (rent) inflation has basically run about 2% above general non-shelter inflation for years, and after accounting for those 2020-2021 pendulum swings in the Zillow data, it basically continued to do that.

In Figure 2, you can see that general non-shelter inflation has been running at about 2% for the past year while the Zillow rent estimate has risen by about 3% (implying about 2% rent inflation). This is actually true 2% inflation. It remains to be seen if it is permanent. The Erdmann Housing Tracker suggests that building has been strong enough to, maybe, finally, tame rent inflation. That remains to be seen. But true inflation, with or without shelter, is definitely not running hot at this point.

More below the paywall.

Keep reading with a 7-day free trial

Subscribe to Erdmann Housing Tracker to keep reading this post and get 7 days of free access to the full post archives.