December 2022 Erdmann Housing Tracker Update

Trends remain in place. Zillow’s aggregate US ZHVI price estimate hasn’t yet declined. There are 2 types of other price estimates you typically see: prices of sold homes, and the Case-Shiller index.

The prices of sold homes measures have shown some decline in some cases because they aren’t controlled for composition. The homes that are selling have lower values, but the prices of all homes, on average, aren’t declining. It’s the changing subset of homes that are selling that is driving that decline.

Case-Shiller is declining because it’s a value-weighted average, while Zillow is basically a median. For those of you who receive my monthly data, you might notice that the measured average home price in the data that I use to estimate national average price variances has declined by a couple of percentage points over the last few months. That price estimate is a value-weighted average of ZIP codes.

Supply constraints affect low-priced homes more and cyclical changes affect high priced homes more. Since cyclical factors have been declining, this affects value-weighted averages more than it affects median estimates. So, the Zillow estimate is still stable while Case-Shiller has lost a few percentage points.

A similar thing happened from 2002 to 2005, where my model attributes some rising prices to cyclical appreciation. The Case-Shiller index gained close to 10% more than ZVHI, and then they started converging again in 2006 and 2007 as the cyclical factor reverted to neutral.

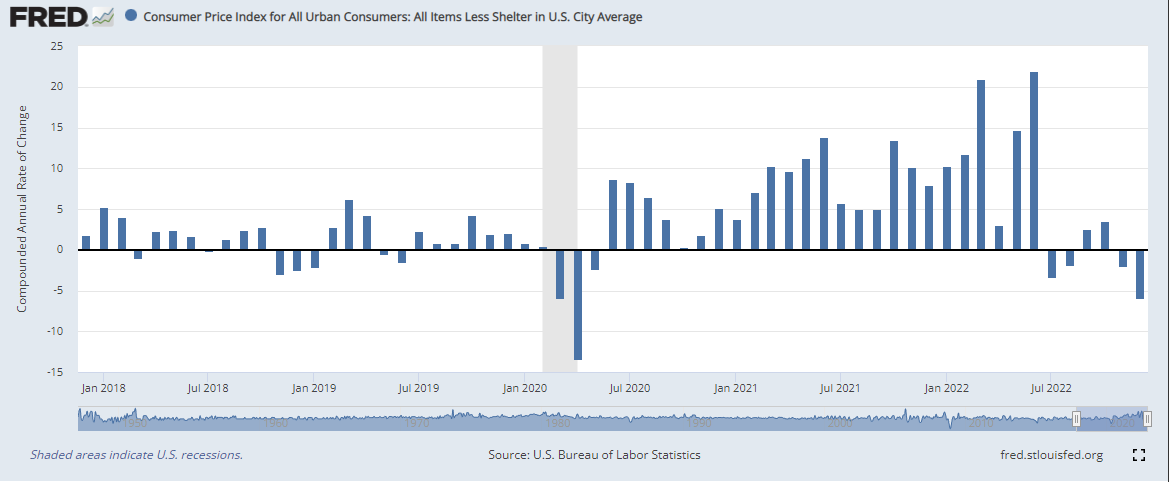

There are now 6 months of deflation in non-shelter CPI, with an especially deep cut in December. This is great news because it suggests that the economy can stabilize and that high inflation was temporary, either naturally or because of Fed reactions.

As readers know, I don’t think it is helpful to think of this process or of Fed policy with an interest rate focused framework. Figure 2 compares the national ZHVI price index with 30 year mortgage rates. There are 3 distinct phases in price trends. Using the Erdmann Housing Tracker components, Phases 1 & 3 are associated with cyclical headwinds and Phase 2 with cyclical tailwinds. Phases 1 & 2 are associated with price appreciation from supply constraints and Phase 3 with stabilizing supply.

So, the especially flattened price trend is more due to a pause in supply constraint appreciation than it is to unusual cyclical reversal (though the cyclical reversal is a little bit steeper than pre-2020). My supply component can pick up changes in credit conditions, so it is possible that a flattening in my Supply component would be due to less credit access. But, where the Supply component has flattened the most, and even reversed, it has been in expensive cities with higher incomes that had the worst supply problems. Possibly, there is an odd combination of factors that would cause rising rates to have this effect. But, I think the simplest explanation is that, at least at the completions end of housing production, the pace of supply has remained stable at the pace of the pre-Covid cycle highs, and so cyclical reductions in demand are being reflected somewhat in supply-related price trends. This is different than in 2006-2007 when new home construction was declining steeply as the national economy began to waiver.

More updates on the data below the fold.