Scott Sumner had a post about politics in Wisconsin, and I’m going to focus on a minor implication he made in the post. He wrote:

Nonetheless, the post-1980 shift from manufacturing to industries like tech and finance has resulted in some loss of highly educated people to the coasts (or Chicago.) In the 1960s, that sort of migration would have pushed politics to the left, but in today’s world it shifts politics to the right. There is one island of progressivism left in Wisconsin, the city of Madison (and Dane County), which has the state capital and the flagship campus. Nolan Gray linked to a map that suggests that Madison has the highest land prices (relative to house prices) between NYC and Boulder, Colorado:

Figure 1

Madison is basically a “coastal city”…

It is interesting that the measure Scott uses as a signal of progressivism is urban land value. I don’t think he means this to be a signal of the pressures of population growth, because population growth has been highest in the south and southwest, where urban land value is shown to be low.

Scott could be drawing on the “superstar” city idea - that cities which draw a lot of highly educated residents become more productive and more expensive.

The alternative explanation is that “coastal cities” are expensive because they obstruct new housing, and they end up with a higher percentage of educated workers with high incomes because the poorer residents move away.

Gray’s tweet that accompanied this map is, “Land share of total property value for single-family homes—at the extreme ends, probably a not a bad indicator of where single-family zoning is acting as a binding constraint.”

Maybe Scott is associating progressivism and a highly educated local electorate with obstructive housing policy.

Land value does rise with agglomeration value, but I’m not sure it rises as a percentage of real estate value. Where housing isn’t obstructed, the additional land value is related to each parcel holding more units of housing. Where housing is obstructed, a monopoly profit on limited housing raises home values, which is attributed to land, and so land value does rise as a percentage of real estate value.

Of course, there could be an interaction between agglomeration value and obstructed supply. Given an obstructed supply context, more agglomeration value would be associated with more land value.

It would be interesting to see what the map would look like from 22 years ago or more. The large portion of land value is a recent phenomenon. Structural value only changes slowly with the deployment of residential investment. Short-term changes in valuations are generally changes in land value.

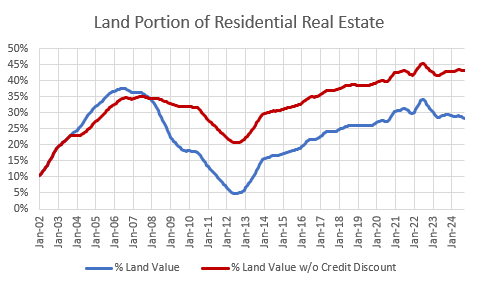

Land value is a much higher percentage of residential real estate than it was 25 years ago. Real estate valuations are way up and residential investment has been very low. Figure 2 is an estimate of land value using the Erdmann Housing Tracker.

Whether it is from urban amenities and networks or from supply constraints, the excess land value comes from higher rents. Then there also is some short-term cyclical movement.

Before 2008, there was some regional rent inflation due to supply constraints and some cyclical price appreciation. Then, from 2008 to 2012, public policy aimed at reversing the price appreciation by removing liquidity from capital markets, but it didn’t aim at reversing the supply-related rent inflation. Then, after the temporary decline in prices, rising rents took over again. Now, inflated rents have added trillions of dollars to urban home values (and land values) but those values are also discounted because of the lack of liquidity for homebuyers.

The blue line is the measured estimate of land value. The red line is the portion of real estate value that would come from land if homes reflected the inflated rental value without the liquidity discount.

The average portion of real estate going to land value, according to my broad estimate, is about 30%. Before 2002 it was below 10%.

Figure 2

To think through these changes, I decided to take a look at housing in Madison, and I am going to compare it to:

another Midwestern regional center - Grand Rapids, Michigan

another college town - Raleigh, North Carolina

a supply constrained poster child - San Diego, California

Since the 1980s, Grand Rapids incomes have been somewhat below the national average. Incomes in San Diego and the college towns have been near or above the national average (Figure 3).

Figure 3

Growth in Raleigh has been above average. Growth in San Diego was above average until the 1990s, then it abruptly slowed and it has continued to decline. Grand Rapids and Madison have grown at or slightly above the national average - about 1% to 2% annually.

Figure 4

Raleigh has permitted housing at well above the national average, befitting its high growth. San Diego has been below average since 1991. Madison has tended to be moderately above average at all times. Grand Rapids was above average before the 2000s and has been below average since then (Figure 5).

Figure 5

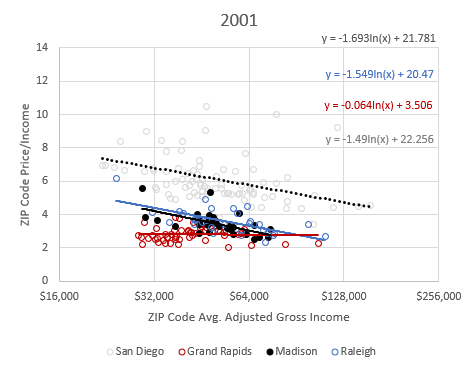

Figure 6 compares price/income ratios across zip codes for each metro area. This is for 2001. This is my proxy for supply constraints. Where housing supply is obstructed, demand elasticity becomes income-dependent. Housing is a bundle of necessities and luxuries. Where housing supply is blocked, richer families give up some luxuries in order to lower costs. In a supply constrained market where new homes are limited, and involves buying an existing home that would have otherwise filtered down to an owner with lower income. As we move down into zip codes with lower incomes, housing becomes more of a necessity and less of a luxury. Demand becomes more inelastic. Families are willing to pay more to keep what they have.

In Figure 6, Grand Rapids shows no sign of supply constraints. The other cities show a moderate signal of supply constraints. But these slopes - a price/income ratio that declines by about 1 point for each doubling of income - are pretty moderate. They are not strong signs of supply constraints.

Also, you can see that San Diego is more expensive across the board. I haven’t gone to the trouble of correcting this data, but much of that difference is from property tax differences. Average property taxes in San Diego are much lower than for these other cities. Maybe some of the difference that remains could be attributed to some inherent value to living in San Diego, which raises home prices across the board.

Figure 6

From 2001 to 2006, San Diego changed drastically. The gradient became much steeper. This was from moderate demand pushing against hard supply constraints. The other 3 cities didn’t change that much during that time.

In other words, that first bump in Figure 2 all came from low-tier San Diego and places like it, and it was mostly supply constraints.

Figure 7

Fast-forward to 2024. San Diego is still steep. Raleigh and Madison still really haven’t changed that much. And, Grand Rapids has steepened.

In both 2001 and 2024, high tier price/income ratios were about the same in all cities. In both 2001 and 2024, price/income in low-tier Madison and Raleigh ranged from about 4 or 5. From 2001 to 2024, the low tier of Grand Rapids increased from about 3 to 4. And in San Diego it increased from 7 to 12.

Figure 8

I would say that Madison and Raleigh are not like the coastal cities. To the extent that there is land value, it might be related to very local amenities. I’m not entirely sure why Madison shows up in Figure 1 with high land value. Prices don’t seem high enough to be associated with unusually high land values.

It may have been a standout in amenity value 25 years ago, but as supply constraints have come to dominate real estate valuations, home values in the rest of the country have passed up both Raleigh and Madison. Their potential moderate amount of amenity value is dwarfed by the supply-constrained valuations of San Diego, and they also are less inflated relative to the newly supply-constrained valuations of Grand Rapids, which was hit especially hard by the liquidity crackdown.

It could be that more than 25 or 30 years ago, in Figure 1, there were little moderately green Madisons swimming in a sea of yellow. And maybe, like Chicago, the coastal cities would have been moderately green too.

I would argue that economists have hoodwinked themselves into thinking that a handful of deeply supply constrained cities had suddenly attained some magical level of agglomeration value, even as their populations pointedly stagnated. They are asserting a cosmic coincidence between the rise of urban value and the end of growth that coincidentally happened in those very same locations.

In 2024, we now have nearly 20 years of depressed construction across the country. And, lo and behold, cities like Grand Rapids also seem to have suddenly attained some magical agglomeration value just at the same time we killed off their housing construction markets.

It could be that Madison and Raleigh are examples of agglomeration value in their stability and in the moderate scale of their excess valuations. Madison and Raleigh also approve multi-family housing at above-average rates.

Would that the coastal cities would have blessed us with such outcomes and such stability.

PS. Though I didn’t include it in these charts, Austin has similar patterns as Raleigh and Madison. It also approves higher than average rates of multi-unit housing.

Good post. I was going to make a snarky comment about how the collapse in higher education enrollment would force some places to re-assess their zoning regulations in the face of population losses. Turns out that the statistical impact in dropping enrollment probably won't move the needle that much in terms of housing availability---except in some very remote communities where a school closure wipes out the local economy.

I'm inclined to agree with the linkage between wealthy progressives blocking housing construction. Many colleges and universities, particularly highly ranked ones, have practiced a "steady-state" model of enrollment for decades. This stasis has been partly offset by hiring bloat in staff, attendants, and part-time faculty, but the zeitgeist of a college town is one of limited change to the overall population. This creates a political environment that would oppose any type housing construction, because locals---most of who depend on the college for their jobs in a direct or indirect fashion---will associate new inhabitants with undesirables. "You can't let Orcs settle in our Shire!" cry the Hobbits at the town meeting.

The consequence of this stasis is inflated housing costs which creates price pressure for lower paid staff and part-time faculty. Off campus housing for some students can be often be maintained in a state of squalor by landlords because they have a captive market. Occasionally, college leaders will build housing for non-student groups that are critical to the functioning of the institution, but this type of investment is usually regarded as less important than a new football stadium or science building.

Love a good College Town analysis.

Good post. I was going to make a snarky comment about how the collapse in higher education enrollment would force some places to re-assess their zoning regulations in the face of population losses. Turns out that the statistical impact in dropping enrollment probably won't move the needle that much in terms of housing availability---except in some very remote communities where a school closure wipes out the local economy.

I'm inclined to agree with the linkage between wealthy progressives blocking housing construction. Many colleges and universities, particularly highly ranked ones, have practiced a "steady-state" model of enrollment for decades. This stasis has been partly offset by hiring bloat in staff, attendants, and part-time faculty, but the zeitgeist of a college town is one of limited change to the overall population. This creates a political environment that would oppose any type housing construction, because locals---most of who depend on the college for their jobs in a direct or indirect fashion---will associate new inhabitants with undesirables. "You can't let Orcs settle in our Shire!" cry the Hobbits at the town meeting.

The consequence of this stasis is inflated housing costs which creates price pressure for lower paid staff and part-time faculty. Off campus housing for some students can be often be maintained in a state of squalor by landlords because they have a captive market. Occasionally, college leaders will build housing for non-student groups that are critical to the functioning of the institution, but this type of investment is usually regarded as less important than a new football stadium or science building.