Agglomeration Value vs. Scarcity

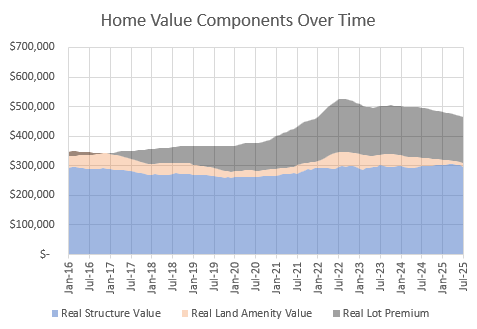

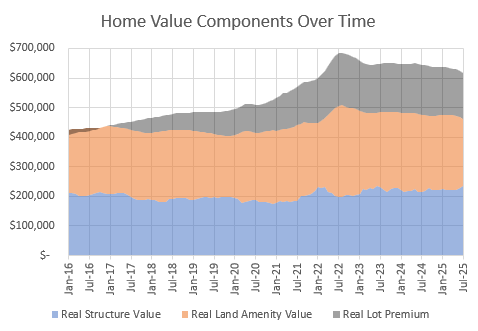

In the recent series of posts I published about my metro area housing trend analysis packages, I used a couple of figures that I think might highlight the issue of land values and urban amenities. I highlighted 2 ZIP codes with very different land values. Figure 1 shows home prices over time in a suburban neighborhood with large homes on spacious lots with little locational value. Figure 2 shows home prices in a central neighborhood with very high locational value.

Let’s approach these neighborhoods with some basic math.

My estimate for this market is that the stock of existing homes is about 12% too small to meet demand. And, by “meet demand” I mean to allow for naturally occurring household formation, aspirational in-migration, and to prevent pressure for uncomfortable down-moves or regional displacement that families are willing to pay excess rents in order to avoid. The $153,000 lot premium in both neighborhoods is a result of supply conditions so poor that they are creating those stresses.

Some economists and analysts argue that upzoning - allowing the construction of new housing in dense, high value parts of cities will make total land value rise because we will utilize the value of cities better.

Let’s say that this city radically reforms its infill construction policies and allows for the entire 12% of pent up housing demand to be constructed in high value neighborhoods.

Let’s assume that the rightward shift of supply in the high value neighborhood does not reduce the market price for that neighborhood’s amenities and the added density also doesn’t affect that price. Arguments go both ways on how those values might change. Let’s keep them constant for now.

In this case, we might imagine that households currently paying $470,000 to move into new houses in the suburban neighborhood will now move into new houses in the high value neighborhood, which will now sell for $470,000 instead of $620,000 because the new supply will eliminate the scarcity lot premium. And, now those suburban homes will only sell for $300,000.

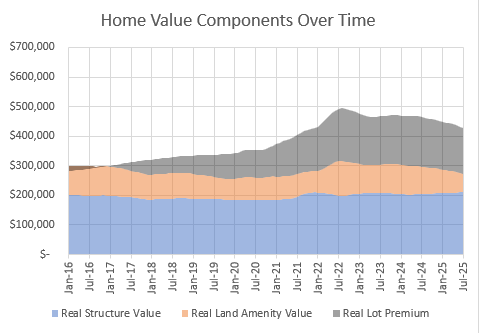

This will compositionally increase the amenity value of land in this city. Figure 3 shows the values of the average home in this city. The average amenity-locational value is currently about $60,000. Increasing the number of homes by 12% with new homes that average $230,000 of amenity-locational value will increase the average lot value in the city by $28,000, from $60,000 to $88,000.

But, the increase in the housing stock will lower the scarcity lot premium on every lot in the city by $153,000.

$153,000 is a lot more than $28,000.

Of course, these are hypothetical numbers, but they are reasonable numbers. And, there are no reasonable numbers that could raise the amenity-locational value more than the scarcity lot premiums will decline.

Also, my estimate of the housing shortage is much higher than almost any other estimate, so my estimate of the amount of new housing it would take to eliminate the lot premium is high.

Of course, my estimate of the lot premium is key. A premium of $153,000 because of scarcity is high. But, this premium has shown up all over the country now. Nobody would attribute an increase of $153,000 of value to homes in this city, or most cities, because of a sudden rise of agglomeration value. And it would be pretty weird if agglomeration value increased home prices uniformly within each market, so that prices in the worst neighborhoods with the least amenity value and the lowest quality homes increased proportionately the most. So, I frankly think economists who believe that total land value will rise if there is broad upzoning are just not looking very closely.

In any case, these are some basic numbers that explain why I don’t have any time for such claims.

Let’s take New York City, for example. Currently the Zillow ZHVI estimate for the typical home in the New York City metro area is $700,000. I estimate that New York City has a $350,000 scarcity premium. The model that provides this estimate today attributes no scarcity premium to New York City homes before 2002. But, since then, the scarcity premium has increased by $350,000. Let’s say that a very large portion of the remaining $350,000 home price in New York City is from location value. Let’s say the average New York City Home has $250,000 of location value, $100,000 of structure value, and $350,000 of scarcity value.

Even with that aggressive assumption of location value, there is no feasible amount of agglomeration value that would amount to enough to outweigh the elimination of the scarcity premium. The average home value would be lower than it is today with any reasonable growth of the housing stock. If New York City grew by 50% and the agglomeration value of the average home grew by 50%, to $375,000 (for a total average value of $475,000 after the correction in the scarcity premium), the total value of all homes in New York City, even after increasing the stock of homes by 50%, would be about the same as it is today. And, the correction of the scarcity premium in the rest of the country after 15 million households move to New York City would reduce residential real estate values in the rest of the country by $15 trillion or more.

There is no feasible arithmetic that raises either average or total American residential real estate or land values, locally or nationally, as a result of more building.

Under normal conditions, building more homes could increase the total value of real estate in some cases, but under shortage conditions that create inflated rents and elevated scarcity value, demand is inelastic and families will spend fewer total dollars when there are more homes. It’s not close.

Agglomeration value is real. It just isn’t all that.

I think the issue comes from attributing scarcity value to agglomeration value. If all of the high value of New York City homes is attributed axiomatically to agglomeration value, then new homes won’t seem to be able to reduce real estate values. But, that isn’t because of agglomeration value itself. It is because the overestimation of agglomeration value comes at the expense of underestimating scarcity value, so the potential for supply to lower prices is axiomatically denied as a result of being attributed to agglomeration value. The same outcome would result if there was no agglomeration value and all New York City real estate value was attributed to the size and quality of the homes.

So, I think the error comes from the tendency among urban economists to have mistaken scarcity value as agglomeration value before 2008. That position should have been put in doubt by the natural experiment we conducted after 2008, when every other city started building homes at the low rate that New York City had been, and every other city started becoming more expensive in exactly the same way that New York City had.

To be clear, New York City has a tremendous amount of locational and agglomeration value. It already had a lot of locational and agglomeration value in 2000. But, I think we should have doubts about how much of the increase in home values since then was an increase in that value versus an increase in scarcity value.