Addendum to 2Q 2024 GDP Update

In the earlier post, I briefly made the case for considering a 5% NGDP growth rate to be neutral until proven otherwise. Nominal GDP had remained pretty close to 5%, cumulatively, during the meaty years of the Great Moderation, from the mid-1990s to the crisis in 2008.

The period after 2008 was an anomaly, mostly created by imposing a huge, one-time credit shock on mortgage markets that created an unrepeatable and unsustainable depression in new home construction.

That has a number of effects on nominal GDP growth. It created unprecedented inflation in land rents. It lowered real investment. It reduced aspirational migration, both internal and international. It lowered household formation. It even may have reduced fertility.

There are a number of channels through which the credit shock of 2008 lowered real GDP growth.

As I wrote that period was unsustainable. Residential investment was unsustainably low. It was in a temporary disequilibrium created by newly lowered home prices that was cured by rising rents, which have finally pushed home values back up to a level that can justify entry-level single-family production. This is the form of housing that has increasingly been a substitute for multi-unit housing since American cities made city building, as it traditionally occurred, illegal over the course of the 20th century.

Residential investment was held unsustainably low for 15 years because apartment construction could not be legally increased. The demand for housing from owner-occupiers that can qualify for mortgage financing is naturally limited to 1 home per household. And rents paid by families who now cannot qualify for mortgages had to rise significantly to get low-tier single-family home prices high enough to induce new building again. (About a half million of these units were constructed annually before the mortgage crackdown.)

Anyway, there are a number of reasons to treat the 2008-2015 period as an anomaly, with the unsustainably low rate of residential investment as the signal of its oddness. My position, as I wrote in the previous post, is that these are complicated interactions. If the 2008-2015 period is an anomaly, we should benchmark GDP growth to previous norms until we see definitive evidence that trend real growth with a normal residential investment rate is different than it was before 2008.

But, in an effort to poke at this idea, I thought it might be a good idea to look at NGDP growth since 2016 relative to other trends.

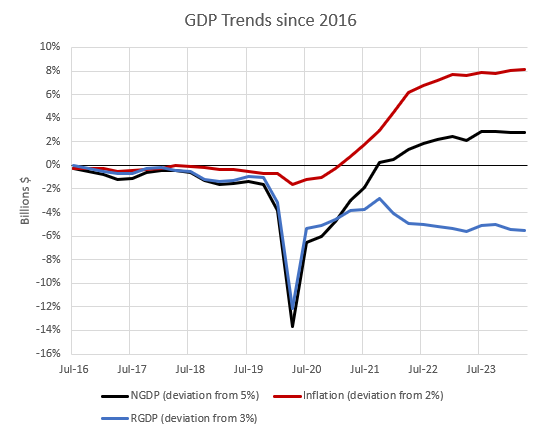

Figure 1 is from the earlier post. It shows nominal GDP growth, GDP inflation, and real GDP growth relative to a 5% nominal trend. (This means a 2% inflation trend and a 3% real growth trend, adding up to a 5% nominal GDP growth trend.)

Using this trend, I conclude that most of the deviation in nominal GDP growth from the neutral trend has been due to the real shock created by Covid. Inflation has been high, mostly, because real growth was temporarily low. Nominal GDP (the black line) has risen cumulatively to about 2.8% above trend, which is pretty mild.

What if we assume a 4% nominal growth trend (2% inflation plus 2% real growth). Figure 2 shows deviations from that trend.

In either case, inflation is cumulatively about 8% above the trend of a 2% inflation target rate. If we assume lower real trend growth, then real growth is currently more than 2% above trend and nominal growth is more than 10% above trend.

This is clearly a trend that is too low. There are still major areas where there are unusual supply constraints related to recent production interruptions. There is still catch-up real growth due to come. Real GDP is not likely to be above some sustainable potential trend line now.

Also, that trend benchmark would suggest that real production was 2% above a sustainable trend when Covid arrived while inflation was below trend. That combination suggests that a 4% target NGDP growth rate was too low in the period leading up to the Covid shock.

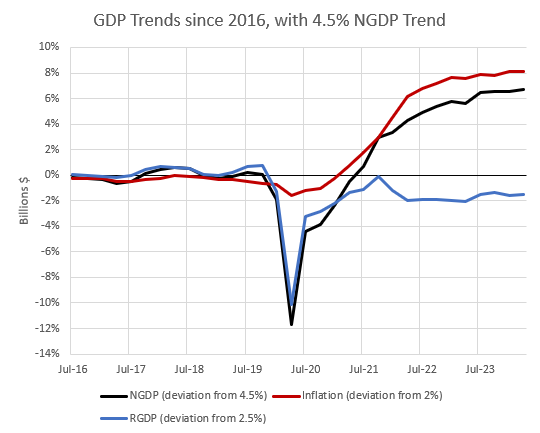

Figure 3 shows the relative cumulative trends with a 4.5% target (2% inflation plus 2.5% real growth). This looks plausible. If this is the neutral trend, then most of the deviation from the nominal GDP trend is due to overshooting the trend. Nominal GDP growth would be cumulative about 6.7% above trend. And, there would still be some room left for some remaining real catch-up growth.

With this benchmark trend, real growth has been running quite linearly along the trend path (2.5% annual real growth) from 2016 to 2019 and again from 2021 to the present, with a one-time Covid shock of about 2%.

So, maybe a 4.5% nominal GDP growth trend is the new normal. I might even agree that this currently appears to make more sense than my 5% benchmark target rate.

But, sustainable residential investment is still higher than the current level. The unsustainably low amount of construction is still causing rent inflation to be elevated (which is more of a transfer than a true inflation. I will have more on that in an upcoming post). I am not sure how deeply the continued cyclical and secular increase in residential investment will reach into aggregate trends to create more real growth in the years ahead. And, there are other categories of growth that likely continue to have catch-up potential.

So, for now, I’m a 5%-er. And if there has been a permanent downshift in that trend, it is likely at a scale of 0.5% annual growth or less.