A way to think about long-term homebuilder expectations

If you look at a typical stock that gained 20% over the past year, the answer to why it gained 20% instead of 10% or 30% will be complicated and full of guess work. If you look at a stock that gained 200% over the past year, the answer to why will probably be pretty obvious. One nice thing about big bets is that they can actually be easier to explain. Of course, that still leaves the problem of being on the right side of them.

Below the fold, I will walk through a simple way of thinking about the long term trends in residential investment. I will generally focus on homebuilders, but you could probably apply this way of thinking about it to various real estate subsectors.

First, one way I would simplify thinking about homebuilders in general is to stop worrying about demographics. I’m not saying demographics is completely unimportant on the margins, but real estate markets are in a strange enough spot that the large forces affecting future trends will dwarf things like demographics. If homebuilder valuations depended on demographics, I wouldn’t be interested in them. Big bets depend on large, simple disequilibria. In real estate right now, if you’re right or wrong about the big questions, your brilliant insights about demographics probably aren’t going to make or break it for you.

My basic reasoning here is this: Imagine two economies. In one, population growth will be 2% annually. In the other, population is flat. Both will have real annual GDP growth over the next decade of 2%. Which one will have higher growth rates in residential investment?

I would argue that to a first approximation it will be similar in both. If residential investment will differ, it will probably be for structural reasons that have little to do with population growth. Poking around 20th century American data suggests a pretty mixed bag on population growth and residential investment, though it’s hard to say because there hasn’t been much variation in population growth until recently.

I think this boils down to a basic rule of thumb in housing. Where there are not artificial supply constraints, modern human beings will spend a predictable amount of their total spending on housing - about 13% of total spending traditionally in the US. That could be 1,200 square feet in a small town in 1960, 2,000 square feet in the suburbs today, or 900 square feet downtown in a large central city. The baseline is determined nominally, mostly by our incomes, and our aggregate real consumption follows that.

So, in two counterfactuals of the US economy a decade from now, if GDP will be $40 trillion, to a first approximation, that tells you most of what you need to know about potential residential investment, regardless of whether that is a country of 340 million or 360 million residents.

On the big picture, I think worrying too much about aging boomers, young first-time buyers, etc., might add more smoke than fire, in much the same way that worrying too much about trade-up buyers, trade-down buyers, and owners tied to low rate mortgages might affect near-term cyclical trends. A lot of that is trading activity that affects gross trading activity a lot more than it affects net changes in consumption.

Now, if your job is deciding a location or picking out styles in the design center for a condo building in development, then those details could be very important. But, I’m not sure they are for deciding how homebuilders will be doing, in general, in 10 years.

Simplifying can help to see some fundamental issues. I think it helps to see how artificial constraints to supply have affected housing expenditures. Figure 1 shows the relative changes in housing expenditures (basically rental value) relative to total personal consumption since 1959 (black), which is a combination of relative rent inflation (red) and relative real housing expenditures (green).

Relative housing expenditures have increased over that time, by as much as 20%. (The current dip is partially a cyclical and a measurement issue. As we move past the recent Covid-related hiccups in income, inflation, etc., cumulative rent inflation will move back to all-time highs and total housing expenditures will move back up above 10%.) That total is a combination of 50% rent inflation and a nearly 30% decline in real housing expenditures, compared to other consumption, since 1959.

This is really the only way to get a positive long-term change in relative housing expenditures. In an amply supplied economy, if anything, as households get richer over time, we might expect a slight downward drift in relative real housing expenditures, with moderate inflation. The only way to get persistent increases in housing expenditures in a normal, growing economy, is to arbitrarily constrain local supply so that some families are stuck in a context where endowment effects and local idiosyncratic amenities mean that they choose to stay in a location in spite of high costs that make them poorer. We know this is the case in places that are conventionally poor - the poorest residents tend to remain when others leave. Where housing is constrained, the same process happens - the people most tied to a location are the ones most willing to accept poverty to remain there - but in this case, the poverty happens with high nominal incomes which are mostly claimed by housing costs. I have touched on this in some of my Mercatus writing, and hope to have another paper out soon that builds on this idea. The relentless rise in housing expenditures over time hasn’t been from irrational speculation and over-stimulus. It’s from inertia, deprivation, and poverty - people willing to spend more on housing because they resist being geographically displaced. If we were overconsuming housing because of demand, we would be spending less!

Since Nobel Prizes are being passed out for being wrong on this, we might be able to profit from it.

There are two big take-aways from Figure 1, then. First, the supposed housing boom in the 2000s was really just barely getting back to a rate of residential investment that was leveling out real housing expenditures enough to begin to bring total spending on housing down. (Note, the bump up in relative spending on housing in in late 2000s in Figure 1 is during the recession when other more volatile spending declined.) And when we broke that, we created a real wing-ding of a situation. Relative rent inflation has been higher than ever for the last 15 years and real expenditures on housing have been falling faster than ever. This should be increasing total relative expenditures on housing. The fact that total housing expenditures have been flat is a sign that we are past the point of families making somewhat difficult decisions in a context of limited choices. We always have limited choices, so, for instance, many families that I meet, who have moved to Phoenix from San Francisco see it as a personal choice, not a moral wrong that was imposed on them. The high costs of San Francisco are just one more constraint they accept as part of the world they have been presented with.

The fact that Americans have been cutting back on relative real housing expenditures so sharply that total expenditures have remained flat, in spite of unprecedented relative rent inflation is a sign that Americans have entered a new context. The housing shortage is making them poorer, and people are frustrated about it.

Basically, one way to think about it is that previously, some Americans were forced into making consumption decisions where they had to trade on location. Now housing has become so universally undersupplied that, in the aggregate, we are just hitting a hard budget constraint.

At this point, we are two steps removed from a neutral residential investment rate. In 2005, we were finally to neutral on a trend basis, with a lot of ground to make up to get housing expenditures back down to normal. Now, we need to increase residential investment just to get back to making locational compromises in that second-best world.

It’s no accident that post-Great Recession population trends into formerly growing cities have been generally lower than pre-GR growth rates. Some of that is due to the fact that rising rents everywhere make them a less worthwhile compromise for families moving out of the traditionally constrained cities. But, I also wonder, given the recent housing expenditures data, how much aspirational migration out of economically stagnant rural areas and into growing cities is being cut off. Have we transitioned from a context dominated by reluctant moves away from expensive cities toward one dominated more by families who would like to move to cities with higher incomes, but who are stuck in cheaper places because metropolitan rents have risen practically everywhere?

What does this mean for homebuilders? Figure 2 compares real growth of personal consumption expenditures (PCE) over time (smoothed to reduce cyclical fluctuations), real growth of housing expenditures, and net residential investment as a percentage of housing expenditures since 1960. In a neutral context with sustainable housing production and moderate housing expenditures, real housing expenditures should increase about as much as real PCE. (It is possible that some future cohort will begin to voluntarily reduce real housing expenditures, but we know because of high housing inflation that this isn’t what’s been happening for the last 40 years.)

Real housing growth requires residential investment. Before the 1980s, total spending on housing remained moderate because residential investment was high and so real housing expenditures were also high. In the 1980s and 1990s, real housing growth and residential investment were lackluster (and, thus, high rent inflation increased total spending on housing). In the 2010s, residential investment and real growth of housing have been dismal. Probably unsustainably so.

It may be that trend real PCE growth has permanently slowed from 3.5% to 2.5% (in part related to slower population growth). Even with that, the level of residential investment that was considered a “boom” in 2021 and 2022 and triggered price spikes in cities across the country is basically the level of investment we need for sustainable housing at this new, low rate of growth, plus we have more than a decade to make up for to get back to an amount of housing that reduces total housing expenditures back to the aggregate level that our great grandparents enjoyed.

I don’t have any insight into the work-from-home phenomenon, but I can say that whatever effects it has had so far, the supply response was not remotely what we should consider a “boom”. If anything the moderate rise in demand that WFH triggered highlights this longer-term supply problem. It is not some unsustainable amount of construction activity that must collapse.

Going forward it will likely take a level of residential investment higher than the peak levels of the Covid period to get real housing expenditures to level out, let alone to recover.

What does this mean for home prices?

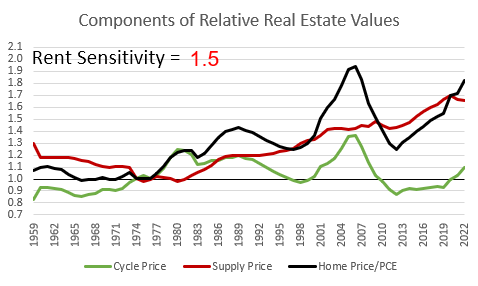

As I have written about extensively, price/rent ratios systematically rise with higher rents. In some other analysis, I have found that for each 1% increase in a metropolitan area’s median rent, its median price will increase by about 1.5%. The black line in Figure 3 is the value of owner-occupied real estate as a percentage of annual PCE since 1959. The red line is the deviation in price that would be associated with long-term rent inflation, given a 1.5x sensitivity. The green line is the residual price deviation after accounting for the sensitivity to rising rental values.

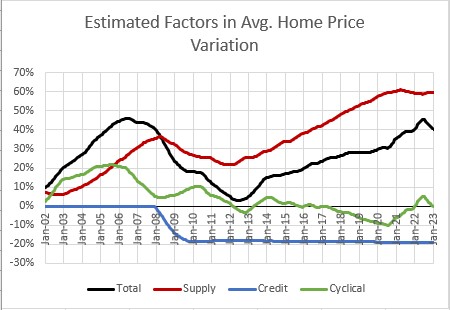

You might notice that this bears some resemblance to the estimates of supply-related price deviations and cyclical deviations which I derive in the Erdmann Housing Tracker from a completely different method, though I have not included a Credit component here.

This is where you can gain a trading advantage, because it is common to view the 80% inflation in relative prices since the 1970s to low interest rates, real estate subsidies, irrational exuberance, etc. and so a return to normalcy would be associated with demand-side deprivation. When this affects policy decisions, it’s not so great. But, I think the mistake may be universal enough to overcome the usual market efficiencies that would reduce speculative opportunities even when most market participants aren’t rational or informed. So, as a trading proposition, misunderstandings present an opportunity.

With regard to understanding the value of real estate sector investments, that advantage comes in 2 layers:

Prices of homes currently reflect rental value, and aren’t generally due for some massive reversal.

Price reversals would have to be paired with a large increase in residential investment compared to recent norms. So, business models for whom revenue is quantity of new homes x price of new homes, there really is little chance of a persistent downturn from current levels. Whatever your cyclical concerns may be, for cash flow modeling purposes, the terminal level of revenues for homebuilders, for instance, is very likely higher than recent levels.