2022 September Home Sales & Construction, and 3Q GDP

It looks to me like we are on a nice glidepath back to 5% GDP growth, and I continue to be a J-Pow stan.

Figure 1 shows recent quarter-to-quarter annualized growth rates.

Nominal GDP is gliding right down toward 5%, and it looks like real growth is rising while inflation is subsiding while we do. I don’t see much reason to want any more abrupt of a return to trend growth.

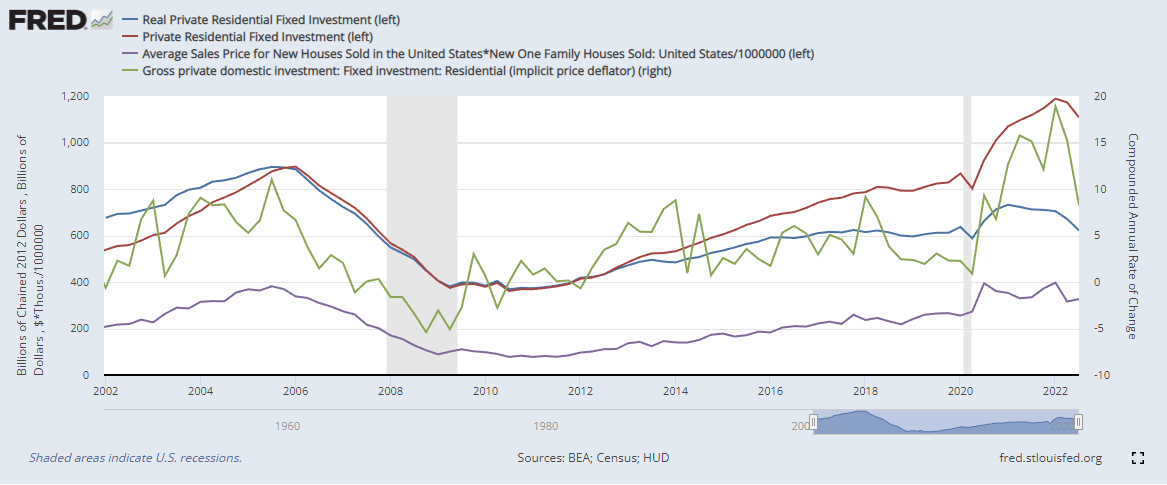

Residential investment took a hit this quarter, but it is generally still within the range of what I would expect in a “soft landing” scenario. Figure 2 shows nominal residential investment, real residential investment, residential investment price index, and the quarterly value of single family homes sold.

That is a pretty steep decline in real residential investment. I don’t think there is any reason, cyclically, for residential investment to move below the current capacity constraints at all.

That is the investment side of housing in GDP numbers. Figure 3 is the consumption side of it. (In quarterly numbers, the BEA only has a “housing and utilities” category.) These are 12 month changes. The green line is nominal spending (basically total rental value), the blue line is the inflationary change, and the red line is real change in the rental value of American homes.

Further analysis below for subscribers.

Keep reading with a 7-day free trial

Subscribe to Erdmann Housing Tracker to keep reading this post and get 7 days of free access to the full post archives.