2022 October New Home Sales & Construction

This month’s review of housing construction and new home sales reports are for subscribers only. The trends in construction activity continue to be novel and interesting.

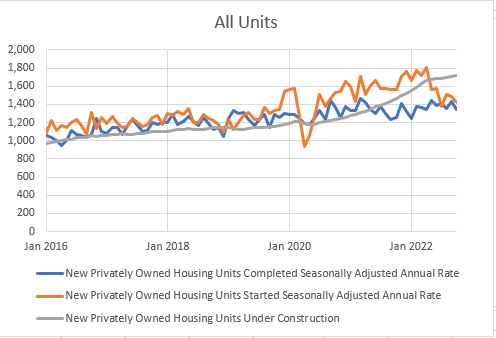

Housing starts continued to decline this month. However, supply chain capacity remains the primary constraint in housing production. Units under construction continues to rise, but not because throughput is increasing. Rather, the queue of units under construction continues to get longer. In other words, you could argue that rather than moving to Category 2 or 3, we are still in category 1. (A market with a growing backlog because of sales outpacing output.) I had expected us to move into Category 3 (work off the backlog), but, the declining sentiment of homebuilders notwithstanding, the housing market appears to me to be maintaining more strength than I had expected (and I hadn’t really expected much decline).

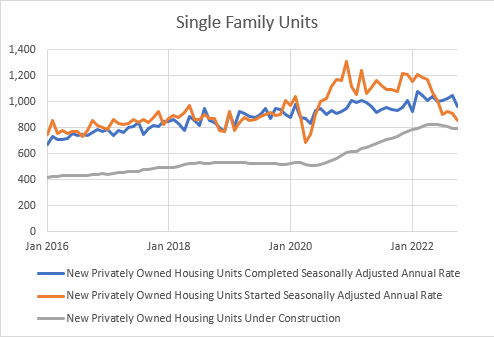

The decline in starts is entirely concentrated in single family homes. Single family builders have slowed their permit requests and continue to have a stable of permitted but not started units. Permits for multi-unit construction continue at a pace which appears to be faster than the supply chain can complete, so all of the recent increase in units under construction is in the multi-unit space.

But, while single family units under construction has plateaued, it hasn’t really declined. Single-family starts have been in the 900,000 units range for 4 months. (Keep in mind this is the seasonally adjusted annual rate, while the units under construction in Figures 3 & 4 are levels. So the difference between starts and completions is amplified by a factor of 12 in the charts.) In June there were 827,000 units under construction, and in October, there were still 794,000.

At the current rate of completions, starts would need to run at about 800,000 annually for a full year to revert to a normal scale of units under construction, even if there is no slowdown in the rate of completions. Even single-family units are in Category 2 (bloated backlog but shrinking), with quite a ways to go to get to Category 3 (normal backlog, no excess units). And it is almost the end of 2022, with nearly a year’s worth of rising interest rates behind us.

Keep reading with a 7-day free trial

Subscribe to Erdmann Housing Tracker to keep reading this post and get 7 days of free access to the full post archives.